Asian Futures:

- Australia's ASX 200 index fell by -49.9 points (-0.74%) to close at 6,710.80

- Japan's Nikkei 225 index has fallen by -65.79 points (-0.23%) and currently trades at 28,864.32

- Hong Kong's Hang Seng index has risen by 38.05 points (0.13%) and currently trades at 29,274.84

UK and Europe:

- UK's FTSE 100 futures are currently down -46.5 points (-0.7%), the cash market is currently estimated to open at 6,604.38

- Euro STOXX 50 futures are currently down -24 points (-0.65%), the cash market is currently estimated to open at 3,680.85

- Germany's DAX futures are currently down -60 points (-0.43%), the cash market is currently estimated to open at 13,996.34

Thursday US Close:

- The Dow Jones Industrial fell 345.95 points (-0.0111%) to close at 30,924.14

- The S&P 500 index fell -51.25 points (-1.35%) to close at 3,768.47

- The Nasdaq 100 index fell -219.325 points (-1.73%) to close at 12,464.00

It was the strong dollar, weak Wall Street theme that initially weighed on sentiment for equity traders in Asia as shares across all regions were in the red. Yet towards the end of the session US futures turned flat then slightly higher ahead of the European open. Due to lack of bearish follow through and volatility overnight, we cannot write off the potential for a minor rebound for indices.

The Nasdaq 100 closed to a 3-month low, making its second session below the 12,755 neckline of a head and shoulders top pattern. Yet with 12,241 support nearby we see potential for a technical correction but the bearish reversal pattern remains in play whilst 12,755 caps as resistance.

S&P E-mini futures closed beneath its 50-day eMA and its November bullish trendline yesterday. So bears may be tempted to reload upon retracements towards 3,785 – 3,800 resistance and shoot for the 3,656.5 lows. But, if yields are to stop rising then indices are a prime candidate for a rebound, and we could just as easily see the S&P breaking higher and gunning for 4,000. So really it is down to how yields behave going forward as to why way equities wat to trade today leading up to NFP.

S&P 500 cash: 04 March 2021

- The index closed -4.61% below its 52-week high

- Energy (2.47%) was the strongest sector and Information Technology (-2.25%) was the weakest

- 7 out of the 11 sectors outperformed the index

- 77.03% of stocks closed above their 200-day average

- 69.5% of stocks closed above their 50-day average

- 40.99% of stocks closed above their 20-day average

Forex: Dollar edges to a new high in Asia

Dollar bulls retained control throughout the overnight session with USD remaining the strongest major currency. The USD dollar index notched higher a further 0.08% which took it to its highest level since the 1st of December 2020. Even if volatility was on the cute side.

Whilst volatility was low among the majors, the dollar rose around 0.2% against the Turkish Lira and South African rand, and around 0.15% against the Swedish Krona and Norwegian Krone.

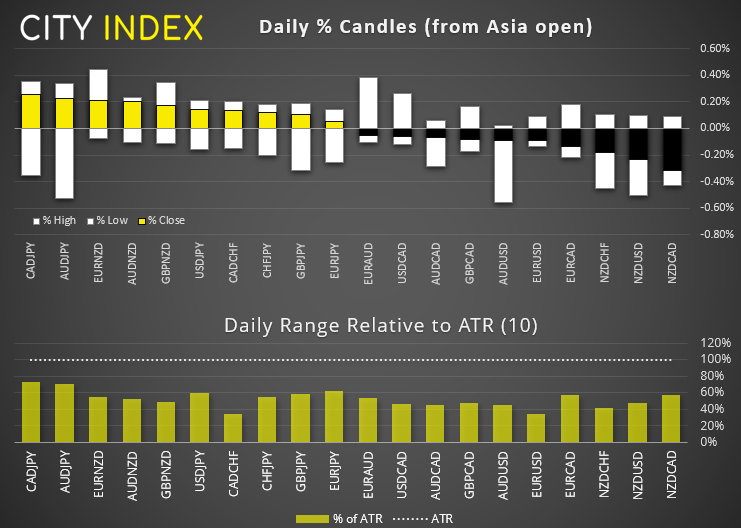

AUD/USD teased bears with a break beneath 0.7700 support (outlined in today’s Asian Open report) and NZD/USD extended losses to a 12-day low. EUR/GBP closed beneath 0.8616 flagged in yesterday’s European Open report although, as of yet, lacks bearish follow-through. From here we’d be looking for short opportunities beneath this key level but, if momentum takes it above resistance early on, be on guard for a ‘fakeout’ and subsequent move higher.

Commodities: WTI flies high (just watch your head at resistance)

WTI rallied around 7% yesterday and now trades at its highest level since January. Yet this technical milestone may become its (temporary) downfall as prices sit just below the January 2020 high (65.65) and the April 2019 high (66.50). Given their significance it looks like an obvious place to book a profit. But as the daily trend remains bullish above 59.24, if prices can clear those historical highs then the skies become clearer for a run to $70.

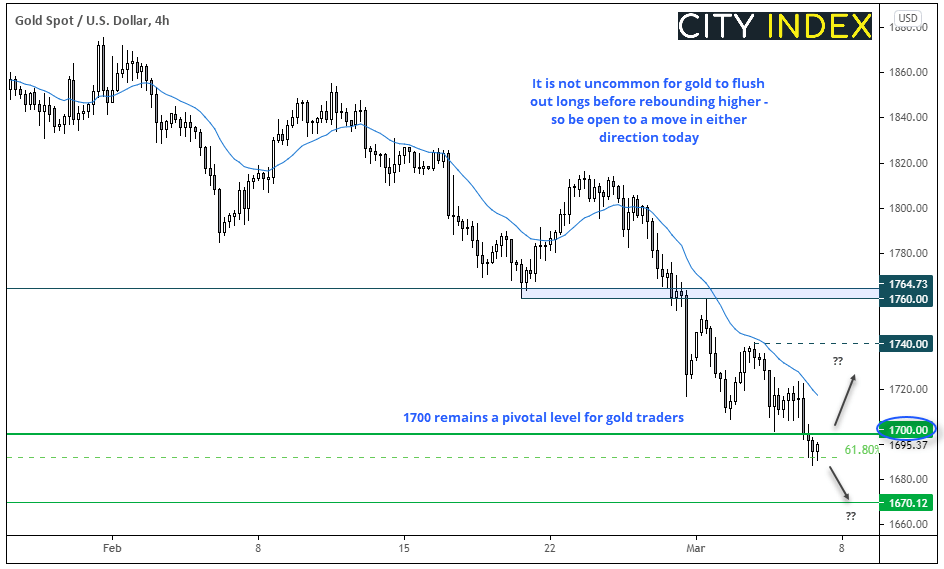

Gold prices closed below 1,700 for the first time yesterday since June 2020. And we expect 1,700 to remain a pivotal level and key focal point for traders over the coming session/s. Simply put, bears may be tempted to fade into minor rallies below 1,700 and target the lows around 1,670. Whereas a quick recovery and rise above key resistance would point towards a bear-trap and flush out of ‘weak longs’. Which seems to be a particular feature with gold price action at such key levels.

- Bears could seek bearish setups on intraday timeframes below 1,700 or wait for a break beneath yesterday’s low, to confirm bearish resumption

- Next major support is 1,670.12, making it a viable bearish target if 1,700 is confirmed as resistance

- However… with prices finding support at a long-term 61.8% Fibonacci ratio we are on guard for a break above 1,700 to signal a bear-trap and run towards 1,740

Elsewhere in commodities, copper is back above $4.00 and its 20-day eMA after rebounding from a key support level (September 2012 high at 3.840). After a sharp rally this year a correction was not overdue, making its -11% correction from last week’s multi-year high not-so-surprising. And whilst it’s too early to tell whether this bounce is part of a deeper correction, most would agree that 3.840 support remains a pivotal level going forward.

China on the rise? (even if below expectations)

China’s Premier Li surprised analysts by announcing a growth target ‘above 6%’ for 2021, when expectations were for a 8-9% rebound. CPI is also to be pegged to around 3%. Overall, the premier sounded optimistic about China’s economy and spoke of “mutually beneficial China-US business relations” when speaking on international trade.

Up Next (Times in GMT)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

- All eyes will remain on the bond market to see if rising yields continue to supress equity prices and boost the stronger dollar further.

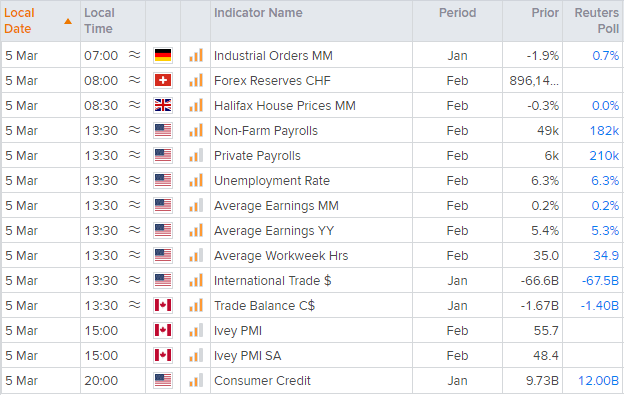

- Event wise, traders will keep a close eye on this month’s Nonfarm payroll report. View Matt Weller’s preview for a complete rundown: NFP preview: When will jobs growth get back into gear?.

- And Canada’s PMI data also warrants a look which put USD/CAD into view, particularly if oil prices continue to support CAD and yields fall with the dollar if a weak employment report materialises.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM