Asian Indices:

- Australia's ASX 200 index rose by 31.6 points (0.47%) to close at 6,771.20

- Japan's Nikkei 225 index has risen by 253.7 points (0.88%) and currently trades at 28,998.58

- Hong Kong's Hang Seng index has risen by 282.35 points (0.99%) and currently trades at 28,823.18

UK and Europe:

- UK's FTSE 100 futures are currently down -11 points (-0.16%), the cash market is currently estimated to open at 6,708.13

- Euro STOXX 50 futures are currently down -3 points (-0.08%), the cash market is currently estimated to open at 3,760.24

- Germany's DAX futures are currently down -5 points (-0.03%), the cash market is currently estimated to open at 14,375.91

Monday US Close:

- The Dow Jones Industrial fell -121.43 points (-0.39%) to close at 31,270.09

- The S&P 500 index fell -20.59 points (-0.54%) to close at 3,821.35

- The Nasdaq 100 index fell -376.62 points (-2.88%) to close at 12,299.08

Index futures are higher again overnight with Singapore STI rising over 1% and Nikkei 225 futures up around 0.9%. At the time of writing, Nasdaq E-mini futures have recouped +1.25% of Monday’s losses and the S&P E-minis are around 0.8% higher.

Stronger yields during yesterday’s NY session saw the Nasdaq 100 tumble nearly -3% and retest last week’s low, as investors continued to rotate out of high valuation equities. The S&P 500 got off relatively lightly with a -0.54% fall and closed on its 20-day eMA.

S&P 500: 08 March 2021

- The index closed -3.27% below its 52-week high

- Utilities (1.38%) was the strongest sector and Information Technology (-2.46%) was the weakest

- 9 out of the 11 sectors outperformed the index

- 80.2% of stocks closed above their 200-day average

- 94.46% of stocks closed above their 50-day average

- 64.75% of stocks closed above their 20-day average

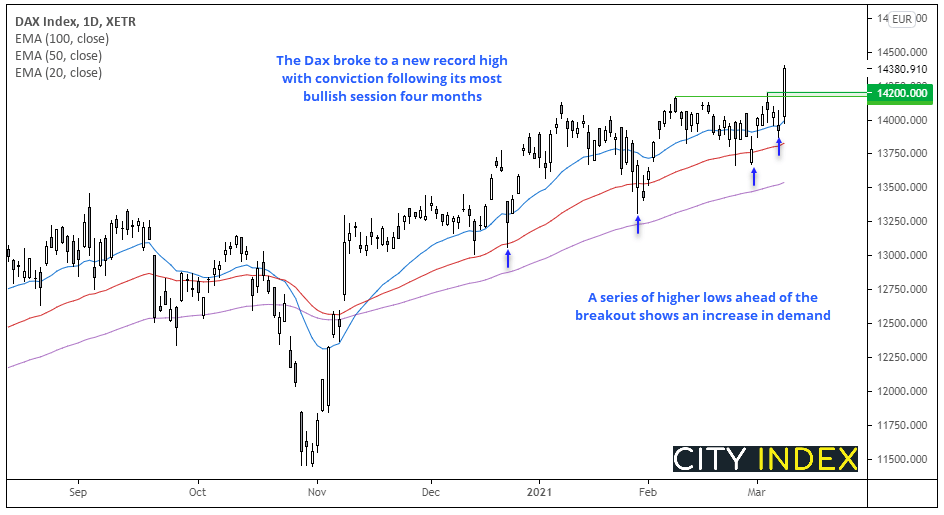

Dax hits record high

Weaker German industrial production weakened the euro and helped strengthen stocks as investors bet on more fiscal stimulus and easy policies from the ECB. Rising around 3.5%, it was the most bullish session for the Dax since November and it closed above its prior highs with staunch conviction.

- Our bias remains bullish above 14,200

- Bulls could look to enter longs upon a low volatility retracement or period of consolidation above its prior highs

- Given its at a record high an open upside target could be used, or technical indicators such as pivot points can project potential targets

Gold bugs look to 1670 as their last line of defence

Gold prices retraced overnight after printing a firm bearish close below 1700 and forming a bearish engulfing candle. Given the ease at which longs were flushed out around 1700 then we could see key support around 1670 challenged today. And, as we’d expect to see some large stops beneath this level, we could see a battle from bulls to defend it (bullish volatility) unless large stops are triggered and prices get sent sharply lower.

Forex: Another g’day for Aussie data

NAB’s business confidence index rose to a 10-year high as higher employment, sales and profits pointed towards a stronger then expected recovery. Business conditions rose to 15 from 7 prior, and now sits back at its highest level since August 2018.

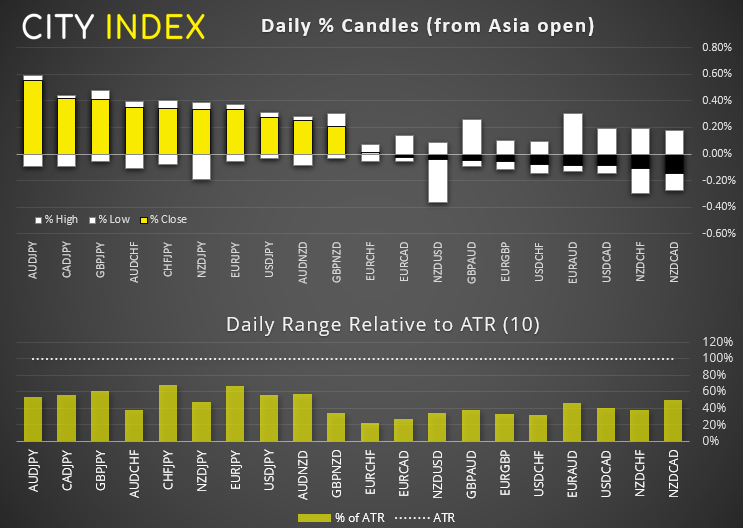

- AUD/JPY is currently the strongest FX pair although volatility remains calm overall, with daily ranges sitting around 40-50% of their 10-day ATR (average true range).

- AUD/USD has stabilised above the 0.7620 low, yet within the prior two-day range and well below the 50-day eMA. Until we see weakness for the dollar then our bias remains bearish below 0.7700.

- GBP/USD has remained confined within the 1.3773 – 1.3866 outlined in yesterday’s European open report. A break above 1.3866 invalidates the bearish bias, whereas a break below 1.3773 reaffirms it.

- EUR/USD’s decline has stalled at its 200-day eMA which leaves the potential for a technical bounce, assuming the dollar’s rally can calm down a little first. Yet with momentum predominantly bearish leading into this key level we suspect it may be a minor bounce at best. Ultimately, our bias remains bearish below the 1.1952 swing low and we’d favour fading into (shorting) into retracements.

Japan’s GDP deflates in final reads

Japan’s growth was downgraded in Q4 as capital expenditure and private inventories were lower than originally expected. Q4 annualised growth now sits at 11.7% YoY (12.7% prior) and the consensus was for it to be upgraded slightly to 12.8%. The quarterly read suffered the same fate and was reduced to 2.8% from 3% previously.

USD/JPY hit fresh highs above 109 and sits at its highest level since June 2020. Given every technical indicator screams overbought (yet price action has yet to confirm any of them), the intraday bias remains up. The next major resistance level is the 109.85 high and, if current momentum persists, it could be there within two sessions. A break of today’s daily low could be the first suggestion that momentum has turned.

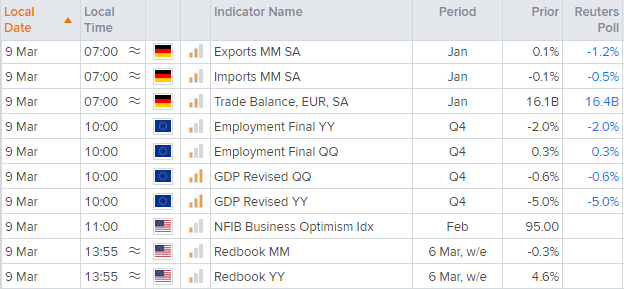

Up Next (Times in GMT)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

- There’s no top tier economic data scheduled for today. Euro pairs could remain vulnerable to weak German trade data (particularly if exports slump more than expected) in a strong US dollar environment.

- The same can be said for Eurozone employment and GDP numbers but, as these are final reads, we doubt they will become too market moving.

- RBA Governor, Dr Philip Lowe speaks at the AFR (Australian Financial Review) business Summit at 22:00.

- Fed member Robert Kaplan speaks at 23:00 speaks on national and global economic issues.

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM