Asian Indices:

- Australia's ASX 200 index rose by 66.3 points (0.9%) and currently trades at 7,448.20

- Japan's Nikkei 225 index has risen by 314.05 points (1.07%) and currently trades at 29,591.91

- Hong Kong's Hang Seng index has risen by 54.95 points (0.22%) and currently trades at 25,302.94

- China's A50 Index has fallen by -128.09 points (-0.82%) and currently trades at 15,550.95

UK and Europe:

- UK's FTSE 100 futures are currently up 6 points (0.08%), the cash market is currently estimated to open at 7,390.18

- Euro STOXX 50 futures are currently up 7 points (0.16%), the cash market is currently estimated to open at 4,365.00

- Germany's DAX futures are currently up 25 points (0.16%), the cash market is currently estimated to open at 16,108.11

US Futures:

- DJI futures are currently down -158.71 points (-0.44%)

- S&P 500 futures are currently up 38.75 points (0.24%)

- Nasdaq 100 futures are currently up 7.25 points (0.16%)

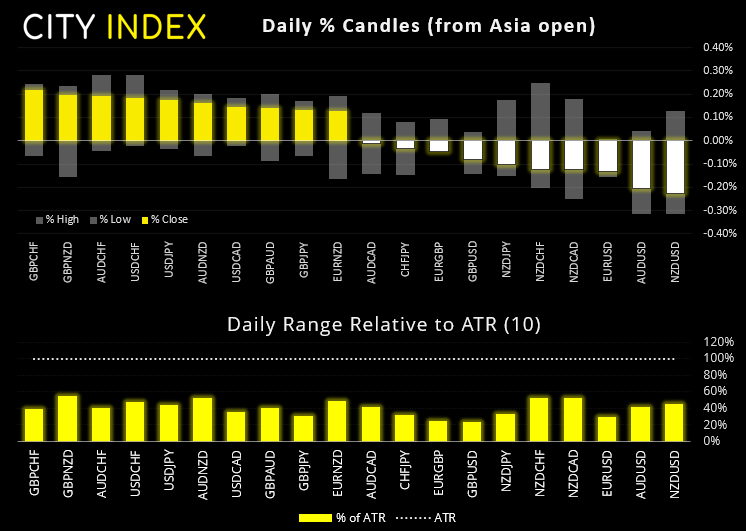

Currency movement have essentially been a one-way bet since Wednesday’s inflation report; buy the dollar, sell its peers. Commodity currencies have been the worst hit, with the Canadian dollar leading the declines ahead of AUD and NZD. Yet volatility behind those moves has been lacking overnight, which leaves the potential for some mean reversion today should US data disappoint.

The US dollar remains the strongest major and is up around 0.2% against NZD and CHF. USD/CAD tapped the 1.2600 handle and USD/JPY pulled back from yesterday’s high, yet a new catalyst is clearly required.

Today, US consumers will tell us how they feel, and then predict inflation

University of Michigan Consumer sentiment survey is up later today. It's still near decade lows but expectations are for a small bounce in today’s report. And that seems plausible, given the index has spent 3-months below -1 standard deviation of its long-term average. However, traders will want to see the inflation expectations component – even if consumers are not deemed to be excellent forecasters - as their inflationary concerns can impact their spending plans.

The 1-year inflation expectations are at 4.8% (highest since 2008) and it could go higher from here. However, Wednesday’s CPI report is not likely to be wrapped up in today’s print, so it may only tick up a little today. Yet next month should fully capture the ‘terrifying’ levels of inflation being widely reported to the average person on the street, which should then feed back into their own expectations for higher inflation.

With that said, there will come a point where consumers start to hold off from their purchases due to rising prices and persistent bottlenecks, presuming they have already bought forward many of their purchases during lockdown with easy month. Time will tell.

As for today, should we see a strong rebound in confidence and rise in inflation expectations, it is another reason for traders to bid the dollar despite its strong gains over the past 48 hours. Whereas a surprise downside consumer report would likely prompt traders to book their dollar profits ahead of the weekend and trigger some mean reversion (bounces) for some oversold dollar pairs.

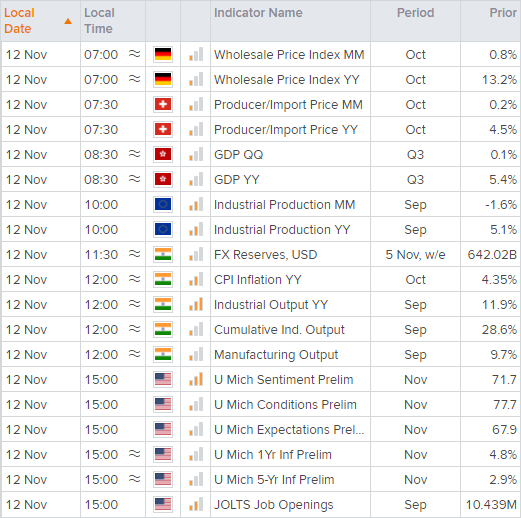

But first, German wholesale data is released at 07:00 GMT, Swiss producer prices at 07:30, HK GDP at 08:30 and then Eurozone industrial production at 10:00. Yet given the dominance of the dollar and US inflation narrative, we do not expect any volatile reactions today from these data sets.

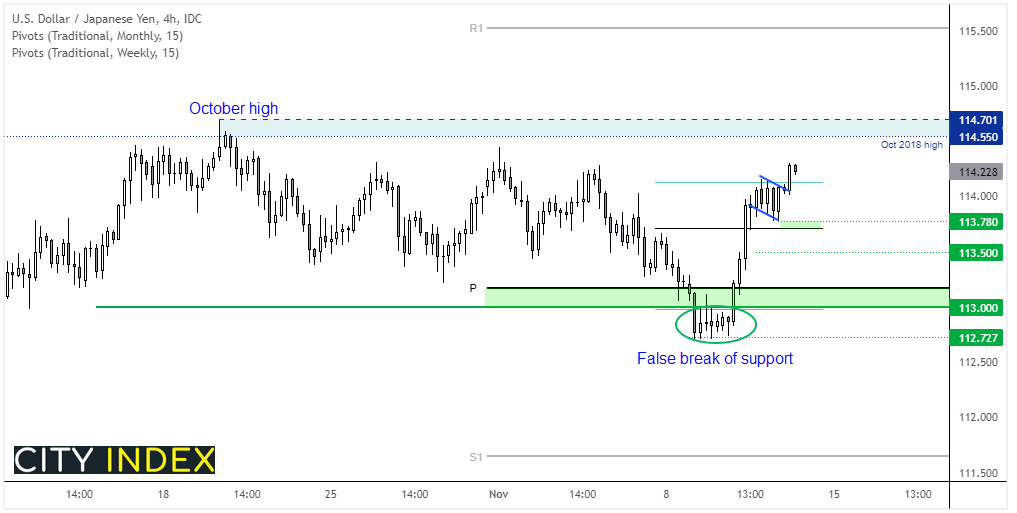

USD/JPY has the 2018 highs within its sights

The strong bounce back above 113 was a pivotal momentum for USD/JPY as it likely marked the end of its correction from the October high. Bullish momentum remains strong overall, and prices have broken above a consolidation pattern overnight to suggest its set to continue higher today. A break back below 114 serves as a warning for bulls, whilst a break beneath likely triggers a countertrend move. Yet whilst US yields remain firm, we expect it to act as a tailwind for USD/JPY.

FTSE 350: Market Internals

FTSE 350: 4231.53 (0.60%) 11 November 2021

- 236 (67.24%) stocks advanced and 106 (30.20%) declined

- 24 stocks rose to a new 52-week high, 3 fell to new lows

- 62.96% of stocks closed above their 200-day average

Outperformers:

- + 14.16% - Auto Trader Group PLC (AUTOA.L)

- + 5.87% - Anglo American PLC (AAL.L)

- + 5.63% - Hochschild Mining PLC (HOCM.L)

Underperformers:

- -19.07% - Johnson Matthey PLC (JMAT.L)

- -10.42% - TI Fluid Systems PLC (TIFS.L)

- -5.59% - B&M European Value Retail SA (BMEB.L)

Up Next (Times in BST)

How to trade with City Index

You can trade easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

April 25, 2024 03:09 PM

April 25, 2024 03:00 PM

April 25, 2024 01:12 PM

April 25, 2024 11:14 AM

Latest Forex articles

April 24, 2024 03:14 PM

April 24, 2024 11:00 AM

April 23, 2024 11:09 PM