Asian Indices:

- Australia's ASX 200 index fell by -32.8 points (-0.43%) and currently trades at 7,596.10

- Japan's Nikkei 225 index has fallen by -504.08 points (-1.8%) and currently trades at 27,472.56

- Hong Kong's Hang Seng index has fallen by -211 points (-0.8%) and currently trades at 26,180.62

UK and Europe:

- UK's FTSE 100 futures are currently down -45.5 points (-0.63%), the cash market is currently estimated to open at 7,173.21

- Euro STOXX 50 futures are currently down -19.5 points (-0.46%), the cash market is currently estimated to open at 4,210.20

- Germany's DAX futures are currently down -66 points (-0.41%), the cash market is currently estimated to open at 15,911.44

US Futures:

- DJI futures are currently up 15.48 points (0.04%)

- S&P 500 futures are currently down -19.25 points (-0.13%)

- Nasdaq 100 futures are currently down -11.25 points (-0.25%)

Learn how to trade indices

Indices mostly lower, led by Japan

Share markets were mostly lower overnight, with China being the exception with the CSI300 rising 0.23%. Japanese equity markets were broadly lower as the Delta variant continued to weigh on Japan’s economic outlook. The TOPIX fell 1.7% and the Nikkei 225 fell -2.04%. The Nikkei 225 futures contract fell to a 2-week low and probed the top of our bearish target range at 27,370.

Soft earnings, a rise in coronavirus cases and Victoria’s lockdown extension weighed on the ASX 200 which is down -0.4% at the time of writing.

The FTSE 100 touched its highest level since February 2020 on Friday, although closed the week just beneath Thursday’s high. Yet bullish momentum remains in favour of the bull-camp overall so we’re looking for a break above last week’s high whilst prices hold above 7171.60.

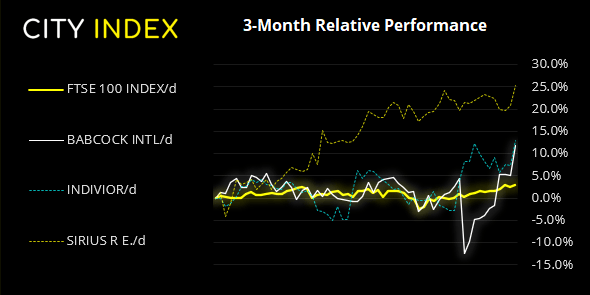

FTSE 350: Market Internals

FTSE 350: 4160.37 (0.35%) 13 August 2021

- 197 (56.13%) stocks advanced and 134 (38.18%) declined

- 51 stocks rose to a new 52-week high, 3 fell to new lows

- 78.63% of stocks closed above their 200-day average

- 78.63% of stocks closed above their 50-day average

- 25.93% of stocks closed above their 20-day average

Outperformers:

- + 6.39% - Babcock International Group PLC (BAB.L)

- + 5.26% - Indivior PLC (INDV.L)

- + 3.71% - Sirius Real Estate Ltd (SRET.L)

Underperformers:

- -27.7% - Avon Protection PLC (AVON.L)

- -4.94% - Tyman PLC (TYMN.L)

- -4.33% - Just Group PLC (JUSTJ.L)

AUD broadly lower:

Commodity currencies were lower overnight on the back of weak data form China. However, the Australian dollar also faced fresh selling pressure after it was confirmed the state of Victoria had extended its lockdown until September 2nd. China’s industrial production rose 6.4% YoY in July, down from 8.3% and missing the 7.8% forecast. Retail sales also missed, rising 8.5% YoY, down from 12.1% in June and missing 11.5% expected. And fixed asset management also came in below expectations at 10.3% compared with 11.3% forecast. Australian bond yields tracked the ASX 200 and AUD pairs lower. The Japanese yen was the strongest major thanks to safe-haven inflows.

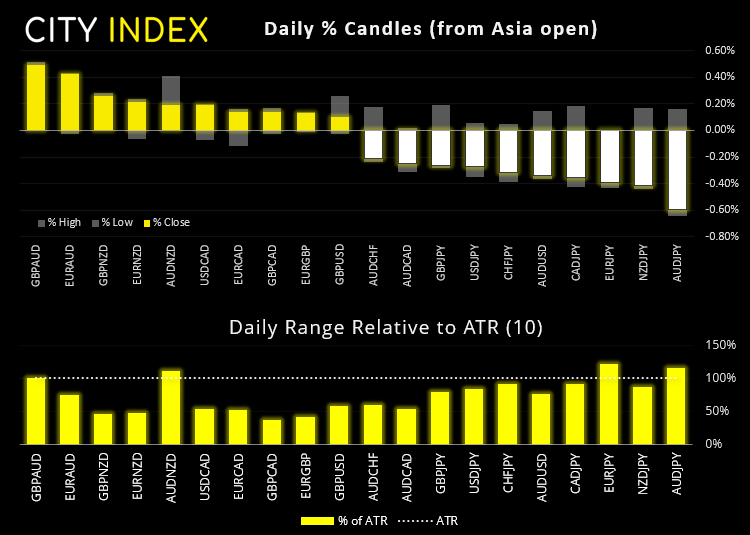

GBP/JPY fell to an 8-day low and is currently beneath the monthly pivot point. GBP/USD edged lower from Friday’s high, although has found support at its 20-da eMA. Should prices hold above 1.3791 then we’d look for da break above its bearish channel to assume trend continuation.

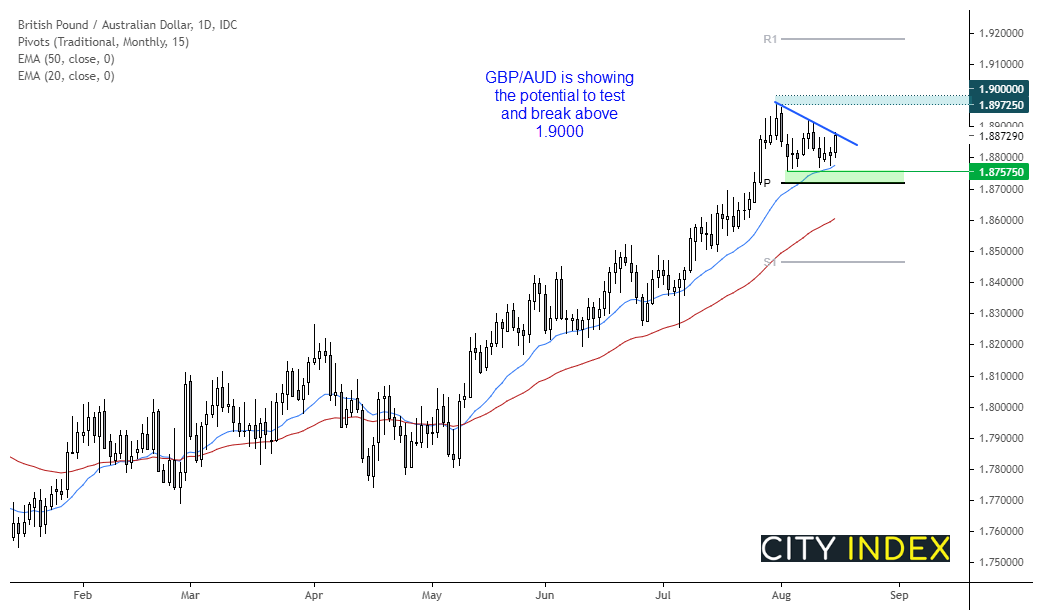

We can see on the daily chart that GBP/AUD remains in a strong uptrend. Prices have been held above the 1.8757 low whilst it traded in a sideways correction and remained above the 20-day eMA. It has risen to a 4-day high ahead of the UK open and shows the potential to extend its rally and potentially resume its uptrend. A break above the retracement line would be a good start for bulls.

Learn how to trade forex

China’s data miss weighs on commodities:

Weak data from China weighed commodities overnight. As for metals, copper is trading -1.3% lower, platinum was down -1% and palladium fell -0.52%. Gold and silver were a touch lower, falling -0.18% and -0.1% respectively. WTI has gapped lower at the open and trades at 67.70, or -1.1% lower.

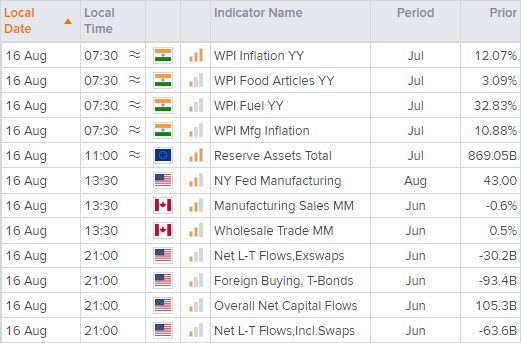

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM