Asian Indices:

- Australia's ASX 200 index rose by 44 points (0.63%) and currently trades at 7,067.10

- Japan's Nikkei 225 index has risen by 23.43 points (0.08%) and currently trades at 29,645.42

- Hong Kong's Hang Seng index has fallen by -276.93 points (-0.96%) and currently trades at 28,623.90

UK and Europe:

- UK's FTSE 100 futures are currently up 8.5 points (0.12%), the cash market is currently estimated to open at 6,948.08

- Euro STOXX 50 futures are currently down -5 points (-0.13%), the cash market is currently estimated to open at 3,971.28

- Germany's DAX futures are currently down -11 points (-0.07%), the cash market is currently estimated to open at 15,198.15

Wednesday US Close:

- The Dow Jones Industrial rose 53.62 points (0.16%) to close at 33,677.27

- The S&P 500 index fell -16.93 points (-0.41%) to close at 4,124.66

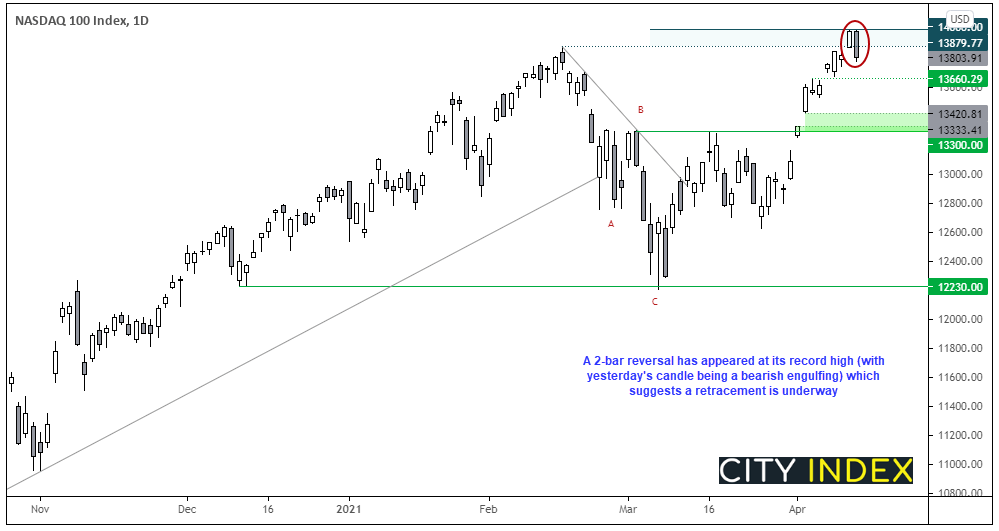

- The Nasdaq 100 index fell -182.58 points (-1.31%) to close at 13,803.91

US indices print ominous candles at their highs.

Well, the Nasdaq did hit our 14,000 this week. For all of 2 minutes. After briefly touching the key milestone on Tuesday and closing at 13,879, it set the stage for yesterday’s bearish engulfing candle from the record high. Therefore, the odds favour a retracement from current levels whilst prices remain below its record high, with 13,660 making a viable first target. But given we are in the middle of a wave ‘3’ uptrend, we make no promises this will be a large correction.

- Today’s bias is bearish whilst prices remain beneath 13,879 (prior record high).

- The initial target is 13,660 support.

- A break to new highs assumes the continuation of wave ‘3’.

The S&P 500 also left a bearish engulfing candle in its wake yet, overall, price action appeared less ominous compared with the Nasdaq. The CAC 40 hit a new record to lead the way higher in Europe, whilst the DAX remains within its tight range, looing for a directional cue to confirm a counter-trend move (with a break below 15,110) or the resumption of its uptrend (with a break to new highs).

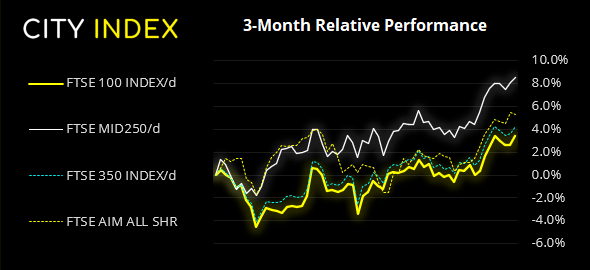

FTSE 100: Market Internals

Large-cap oil and mining stocks lifted the FTSE 100 yesterday, led by Glencore (GLEN.L), Antofagasta (ATO.L) and BP (BP.L). AstraZeneca PLC (AZN.L) recouped 1.5% after its lung cancer treatment Tagrisso was approved by China’s health regulator. At the other end of the Spectrum was Tesco, which found itself in the dented tin aisle with a -4.1% decline following a 20% drop in its pre-tax profits.

The FTSE 100 broke above Tuesday’s bullish pinbar to close at a four-day high. Further gain appear the more likely route with prices accelerating away from their 10 and 20-day eMA (which are also fanning out as they point higher).

FTSE 100: 6939.58 (0.71%) 14 April 2021

- 49 FTSE 100 stocks advanced and 51 declined

- 84.48% of stocks closed above their 200-day average

- 87.93% of stocks closed above their 50-day average

- 72.41% of stocks closed above their 20-day average

- 3 hit a new 52-week high, 0 hit a new 52-week low

Outperformers

- + 5.44% - Glencore PLC (GLEN.L)

- + 4.46% - Antofagasta PLC (ANTO.L)

- + 3.39% - BP PLC (BP.L)

Underperformers:

- -2.03% - Tesco PLC (TSCO.L)

- -2% - Auto Trader Group PLC (AUTOA.L)

- -1.86% - B&M European Value Retail SA (BMEB.L)

Learn how to trade indices

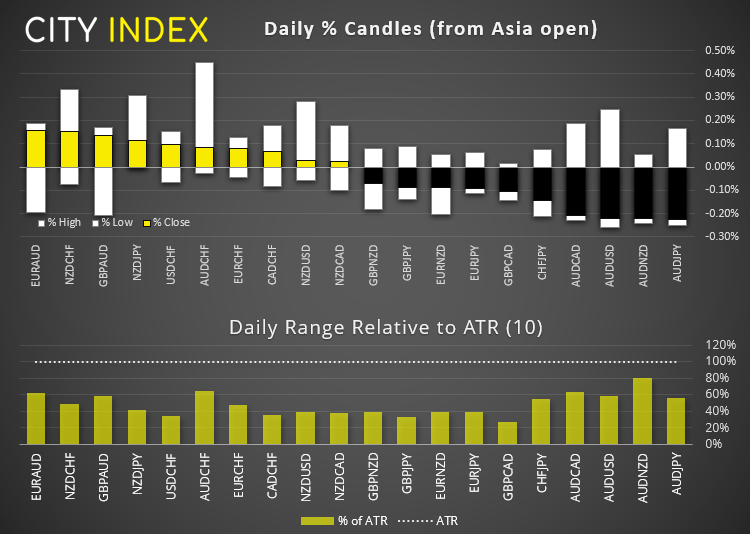

Forex: AUD looks past strong employment report

It was another strong employment report for Australia with unemployment at a one-year low and creation is at a pre-pandemic peak. This is on the back of consumer sentiment which hit an 11-year high yesterday. All jobs lost during the pandemic have been recouped, plus some more as total employment is at a record of 13 million. Yet with a central bank hell-bent on doing absolutely nothing (towards raising rates) then the market looked elsewhere.

- It was minor ranges overnight, despite a glowing employment report from Australia. In fact, AUD and CHF were the weakest majors at around -0.2% lower.

- The US dollar index (DXY) trades just above yesterday’s lows and about midway to the initial 91.30 target with a break beneath 92.00. Whilst we see the potential for a minor pop higher from current levels, the bias remains bearish below 92.00.

- And if that is the case then EUR/USD may have issue testing, let along breaking above 1.2000. Whilst the euro appears structurally bullish, bulls may prefer to buy dips at lower prices or wait for a clean break above 1.2000 before pursuing bullish setups.

- Despite dollar weakness yesterday, GBP/USD failed to hold onto a breakout above 1.3783 resistance and now trades just beneath its 50-day eMA. A break above yesterday’s high suggests it to be a minor blip / setback, but if prices driver lower after the open then we may have a fakeout on our hands.

- GBP/AUD closed to three-week low yesterday following a convincing break lower of its bullish channel. Given it is about half way to our 1.7700 target, we would prefer to see a retracement from current levels before seeking bearish reversal patterns on lower timeframes, to increase the potential reward to risk ratio. The bias remains bearish below 1.8000, although we really don’t want to see any retracement bounce above 1.7933.

- EUR/CAD I struggling to hold above 1.5000. Given the series of upper wicks (selling tails), perhaps this is preparing for a minor leg lower.

Learn how to trade forex

Commodities: Oil high on its own fumes

Oil prices held onto gains overnight, after breaking above key resistance levels yesterday. With fundamentals aligning with its longer-term bullish trend, we won’t be seeking any counter-trend moves at present.

Copper prices also remained just off yesterday’s highs, and price action continues to point towards strong demand around $4.00 as prices have repeatedly failed to hold beneath it since its correction began late February.

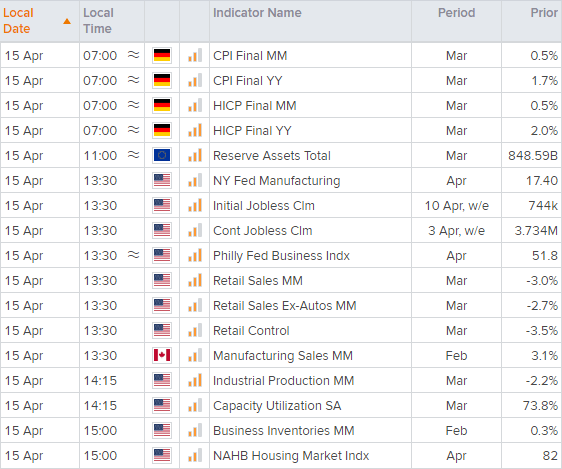

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Today 01:15 PM

Today 07:49 AM

Today 04:24 AM

Latest Nasdaq articles

Yesterday 06:08 AM

April 12, 2024 02:28 AM

April 8, 2024 12:58 PM