Asian Indices:

- Australia's ASX 200 index fell by -36 points (-0.49%) and currently trades at 7,242.50

- Japan's Nikkei 225 index has fallen by -530.42 points (-1.89%) and currently trades at 27,901.30

- Hong Kong's Hang Seng index has risen by 67.78 points (0.28%) and currently trades at 24,104.15

UK and Europe:

- UK's FTSE 100 futures are currently up 35 points (0.5%), the cash market is currently estimated to open at 7,046.01

- Euro STOXX 50 futures are currently up 15.5 points (0.39%), the cash market is currently estimated to open at 4,011.91

- Germany's DAX futures are currently up 69 points (0.46%), the cash market is currently estimated to open at 15,105.55

US Futures:

- DJI futures are currently down -323.54 points (-0.94%)

- S&P 500 futures are currently up 52.25 points (0.36%)

- Nasdaq 100 futures are currently up 6.25 points (0.15%)

Indices

Higher oil prices continued to fan inflationary concerns and weigh on equity prices across Asia. The MSCI APAC index (excluding Japan) fell over 1% and is now approaching the August low. It currently trades lower for a 6th consecutive week. The ASX 200 is currently -0.7% lower and on track to change direction for its 5th consecutive session as the directionless shakeout continues. And the Nikkei 225 accelerated to the downside and hit a 25-day low. The index is down around -10% since its failure to hold above the February high.

Still, there may be chance of a technical bounce looking at the Nasdaq 100. It found support at a bullish trendline from the March low and monthly S1 pivot. It also closed back above the July 19th low, so there is a technical case for a minor bounce (even if it is only short lived). And if the Nasdaq can manage a bounce then it may help the FTSE 100 remain above 7000, a level it tried to crack yesterday.

FTSE 350: Market Internals

FTSE 350: 4026.29 (-0.23%) 04 October 2021

- 57 (16.24%) stocks advanced and 288 (82.05%) declined

- 4 stocks rose to a new 52-week high, 22 fell to new lows

- 55.56% of stocks closed above their 200-day average

- 55.27% of stocks closed above their 50-day average

- 9.4% of stocks closed above their 20-day average

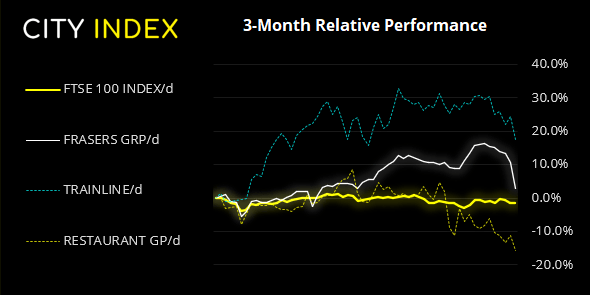

Outperformers:

- + 5.41%-Harbour Energy PLC(HBR.L)

- + 3.71%-BH Macro Ltd(BHMG.L)

- + 3.37%-J Sainsbury PLC(SBRY.L)

Underperformers:

- -6.91%-Frasers Group PLC(FRAS.L)

- -5.53%-Trainline PLC(TRNT.L)

- -5.30%-Restaurant Group PLC(RTN.L)

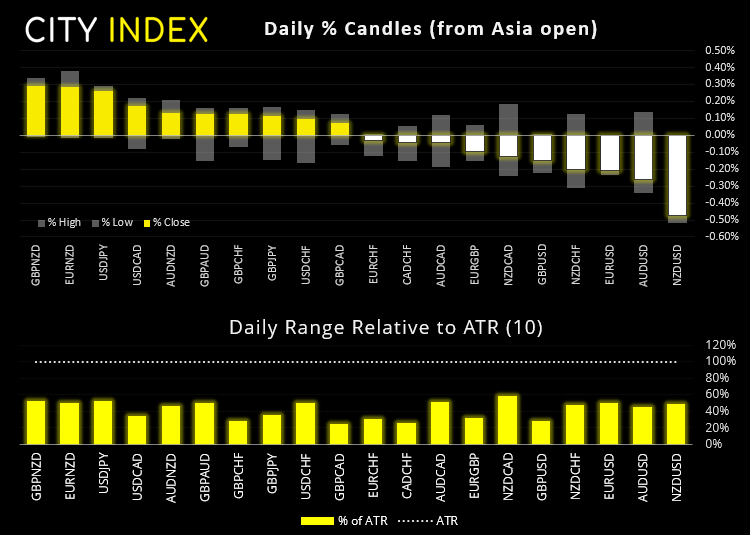

Forex:

The RBA held interest rates at 0.1% as widely expected, and decided to continue purchasing government securities at AU $4 billion per week until at least February 2022. So it look like we get to celebrate the first anniversary of their record low rates at next month’s meeting. Volatility was low overnight and ultimately a minor correction against yesterday’s moves, so USD is currently the strongest major.

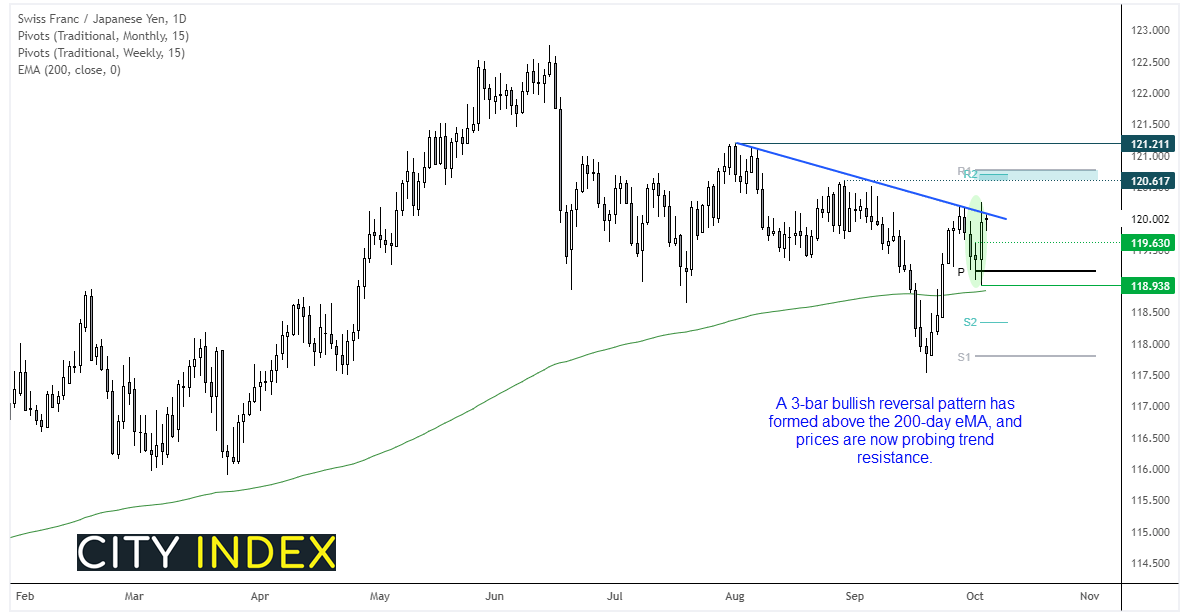

Technically, CHF/JPY may be one to watch after it printed a prominent swing low yesterday. Its bullish outsider / engulfing candle confirmed support just above the 200-day eMA, and followed on from a small Doji as part of a Morning Star reversal (3-bar bullish reversal pattern). Having confirmed support at the monthly S1 pivot point it is now probing trend resistance. If prices can break above yesterday’s high we think it could aim for the 120.62 highs, just below the monthly R1 and weekly R2 pivots.

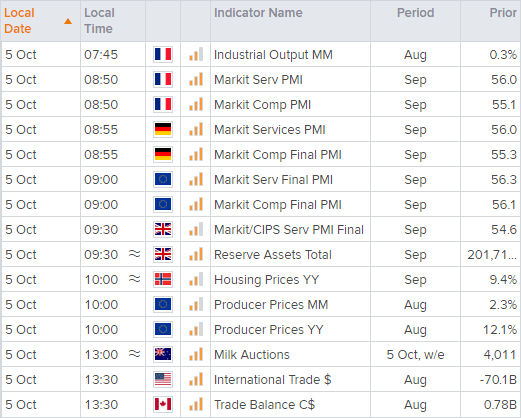

Final PMI reads across Europe place EUR and GBP pairs into focus in today’s session. Yet as it’s the flash report that tends to provide greater levels of volatility traders would need to see some strong revisions before expecting any larger moves.

We also have a few central bankers speaking today. ECB board member Fernandez Bollo speaks at the international summit “GLOBAL NPL” at 08:00. The Fed’s Thomas Barkin speaks at 15:30 BST, and Vice Chair Randal Quarles speaks at 18:15.

Commodities:

Gold was -0.5% lower overnight having found resistance at the monthly pivot point and yesterday’s high. Yet due to its bullish outside day yesterday, a break above resistance assumes bullish continuation in line with Thursday’s elongated bullish candle.

Oil prices were a touch higher overnight after breaking to 3-year high. And should they continue to rise then it could spell further trouble for equities, whilst a pause in trend for oil could potentially see bears shaken out at the lows.

Up Next (Times in BST)

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Latest Forex articles

Yesterday 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM