Asian Indices:

- Australia's ASX 200 index rose by 47.9 points (0.66%) and currently trades at 7,321.20

- Japan's Nikkei 225 index has risen by 616.93 points (2.21%) and currently trades at 28,557.35

- Hong Kong's Hang Seng index has risen by 173.53 points (0.63%) and currently trades at 27,518.07

UK and Europe:

- UK's FTSE 100 futures are currently down -16.5 points (-0.23%), the cash market is currently estimated to open at 7,105.38

- Euro STOXX 50 futures are currently up 0.5 points (0.01%), the cash market is currently estimated to open at 4,068.59

- Germany's DAX futures are currently down -22 points (-0.14%), the cash market is currently estimated to open at 15,665.93

US Futures:

- DJI futures are currently up 448.26 points (1.3%)

- S&P 500 futures are currently down -11 points (-0.07%)

- Nasdaq 100 futures are currently down -7.75 points (-0.18%)

Learn how to trade indices

Asian indices track Wall Street higher

China’s equity markets rallied on Monday following the PBOC’s (People’s Bank of China) decision to cut in the RRR (Reserve Requirement Ratio) late on Friday. Core machinery orders in Japan rose much higher than expected, helping the Nikkei 25 rise 2.3%. South Korean stocks also enjoyed their most bullish session in eight weeks despite the rise in COVID-19 cases in the region.

The FTSE 100 rebounded back above its 50-day eMA on Friday and recovered around three quarters of Thursday’s sell-off. However prices remain very much rangebound between 7000 – 7164 with lots of overlapping candles on the daily chart, so range-trading strategies remain the preference until a breakout develops.

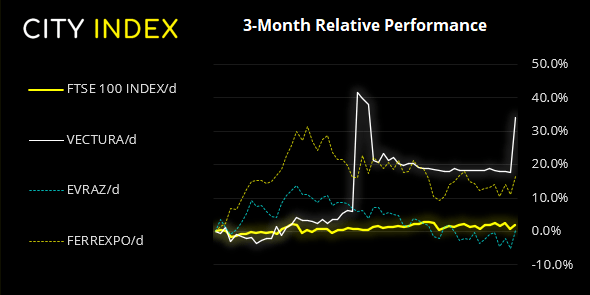

FTSE 350: Market Internals

FTSE 350: 4086.83 (1.30%) 09 July 2021

- 291 (82.91%) stocks advanced and 47 (13.39%) declined

- 20 stocks rose to a new 52-week high, 1 fell to new lows

- 83.48% of stocks closed above their 200-day average

- 56.41% of stocks closed above their 50-day average

- 18.52% of stocks closed above their 20-day average

Outperformers:

- + 14.0% - Vectura Group PLC (VEC.L)

- + 5.45% - EVRAZ plc (EVRE.L)

- + 4.77% - Ferrexpo PLC (FXPO.L)

Underperformers:

- -4.29% - Just Eat Takeaway.com NV (TKWY.AS)

- -2.52% - Centamin PLC (CEY.L)

- -1.78% - CLS Holdings PLC (CLSH.L)

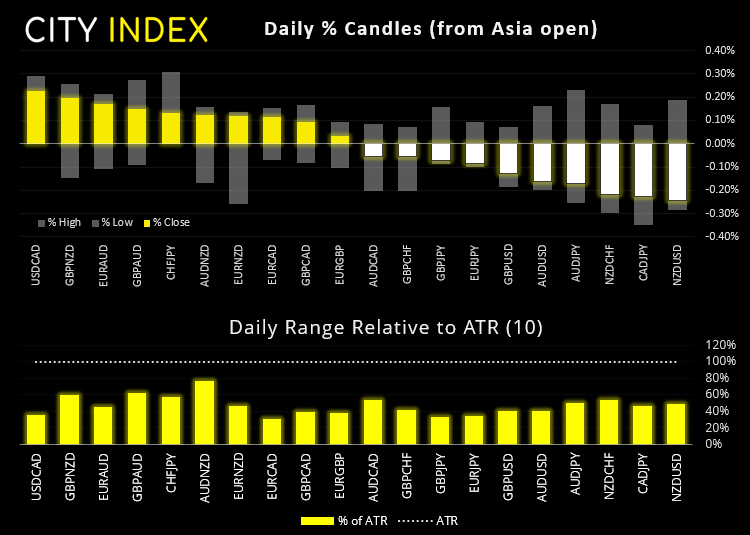

Forex:

USD was the strongest currency overnight whilst NZD and AUD were the weakest. Asian currencies were also mostly higher thanks to the easing from PBOC late on Friday.

We have a quiet economic calendar today so trader so volatility may end up remaining beneath average levels unless headlines can provide a new catalyst. The Fed’s John Williams speaks at 14:30 BST titled “Inflation Dynamics, Expectations and Targeting”.

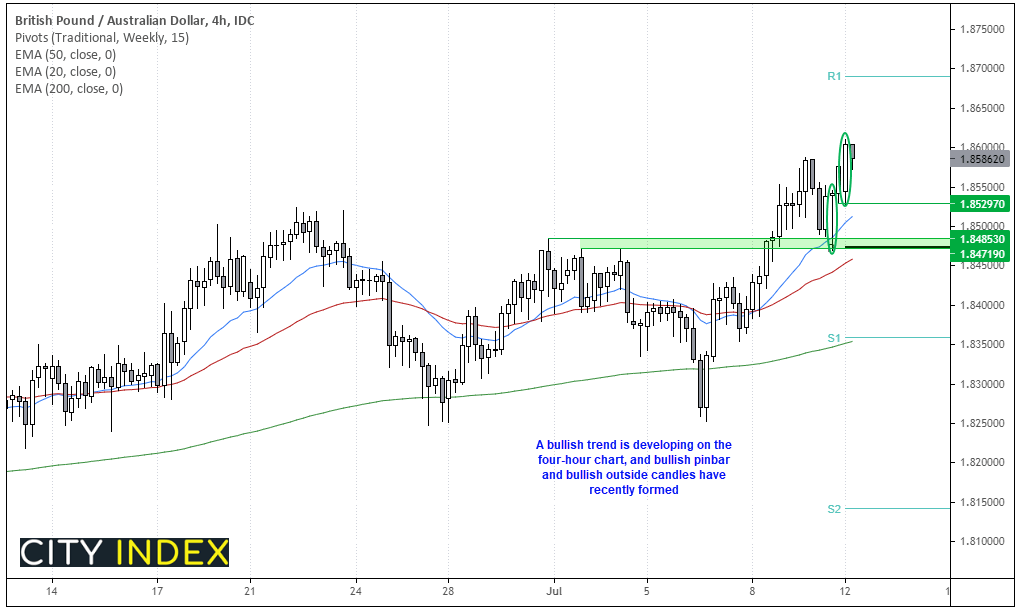

GBP/AUD closed at its highest level in a year on Friday and produced a bullish outside week. A stubbornly dovish RBA combined with Boris Johnson’s desire to go ahead with ‘freedom day’ and lift lockdown restrictions has been a positive driver for the cross, allowing a bullish trend to develop on the four-hour chart.

Prices are holding above the 20-bar eMA and a higher low formed around the June 30th high, which is also near the weekly pivot. Furthermore, a bullish pinbar marks the swing low and a bullish outside candle has since appeared. Our bias remains bullish above 1.8475 and the initial target is 1.8700, near the weekly R1.

Learn how to trade forex

Commodities:

Gold produced a bullish engulfing week and closed above 1800. We had been on guard for a minor bounce given the bullish pinbar at trend support on the weekly chart, although bullish momentum generally lacks conviction. Perhaps Wednesday’s PPI data (inflationary input) or Jerome Powell’s testimony can breath some life into the yellow metal later in the week.

Platinum futures failed to break lower as we’d hoped and is now retesting its 200-day eMA from below. A break above 1115 invalidates the bearish bias but if the 200-day eMA caps as resistance then bears may want to monitor for a break beneath the 1062 low.

Oil prices are a touch lower overnight yet remain just off of their 3-day highs. The daily trend remains bullish on brent and a corrective low at 70.76 suggests it may try to retest last week’s high, with support levels residing around 73.39 and 72.72.

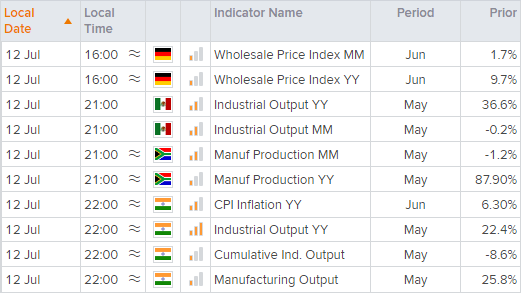

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM