Asian Indices:

- Australia's ASX 200 index rose by 120.5 points (1.67%) and currently trades at 7,355.80

- Japan's Nikkei 225 index has risen by 837 points (2.97%) and currently trades at 28,842.39

- Hong Kong's Hang Seng index has fallen by -5.51 points (-0.02%) and currently trades at 28,483.49

UK and Europe:

- UK's FTSE 100 futures are currently up 16 points (0.23%), the cash market is currently estimated to open at 7,078.29

- Euro STOXX 50 futures are currently up 15 points (0.37%), the cash market is currently estimated to open at 4,127.33

- Germany's DAX futures are currently up 41 points (0.26%), the cash market is currently estimated to open at 15,644.24

US Futures:

- DJI futures are currently up 586.98 points (1.76%)

- S&P 500 futures are currently up 9.75 points (0.07%)

- Nasdaq 100 futures are currently up 6.75 points (0.16%)

Learn how to trade indices

Global healthcare and energy stocks led the rebound according to Reuters indices, and equities from Japan took the lead with the TOPIX rising 3% at the time of writing. It wasn’t celebrations everywhere though, as China’s bitcoin-themed shares were in the red as Beijing continued to tighten their grip on Bitcoin regulation.

Index futures for the US are marginally higher, with the Dow Jones E-minis currently up 0.2% and the S&P rising 0.17%. European shares are set to open higher with STOXX 600 futures up 0.5% and the FTE 100 is set to open around 7078.

FTSE 100 S/R Levels

- R3: 7071 - 7081

- R2: 7140

- R1: 7100

- S1: 7046

- S2: 7018

- S3: 7000

FTSE 350: Market Internals

FTSE 350: 4044.31 (0.64%) 21 June 2021

- 225 (64.10%) stocks advanced and 114 (32.48%) declined

- 7 stocks rose to a new 52-week high, 11 fell to new lows

- 83.48% of stocks closed above their 200-day average

- 12.54% of stocks closed above their 20-day average

Outperformers:

- + 34.6% - WM Morrison Supermarkets PLC (MRW.L)

- + 9.14% - Capita PLC (CPI.L)

- + 4.80% - Energean PLC (ENOG.L)

Underperformers:

- -4.95% - Auction Technology Group PLC (ATG.L)

- -4.59% - PureTech Health PLC (PRTC.L)

- -3.75% - Moonpig Group PLC (MOONM.L)

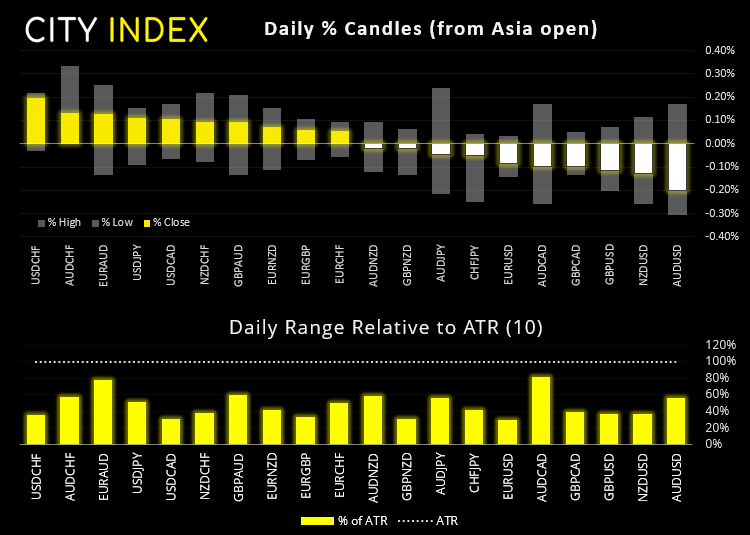

Forex: Yen pairs in focus around risk-appetite

The US dollar index (DXY) was a touch higher overnight by around 0.08%, so relatively miniscule moves compared with the previous two days of trade. Still, it is keeping above its 200-day average and Friday’s low for now, an area we expect to remain pivotal over the coming session/s.

With US bond yields forming an intraday V-bottom recovery yesterday, with bullish a bullish close with long lower wicks then we should consider the potential for risk assets (such as equities and commodities) to rebound. But this ultimately hinges around how hawkish Fed members are this week among their 16 scheduled speeches.

The British pound remained firm overnight with several pairs trading just off-of their week’s highs. GBP/CHF continues to tease traders with a break above the 1.2800 – 1.2817 resistance zone, but until it does then range-trading strategies are preferred.

With a rebound in risk sentiment the Japanese yen has come under selling pressure. Given the magnitude of moves between Wednesday and Friday, we think there is the potential for risk to recover (should Fed speakers allow….) which leaves several yen pairs vulnerable to movement.

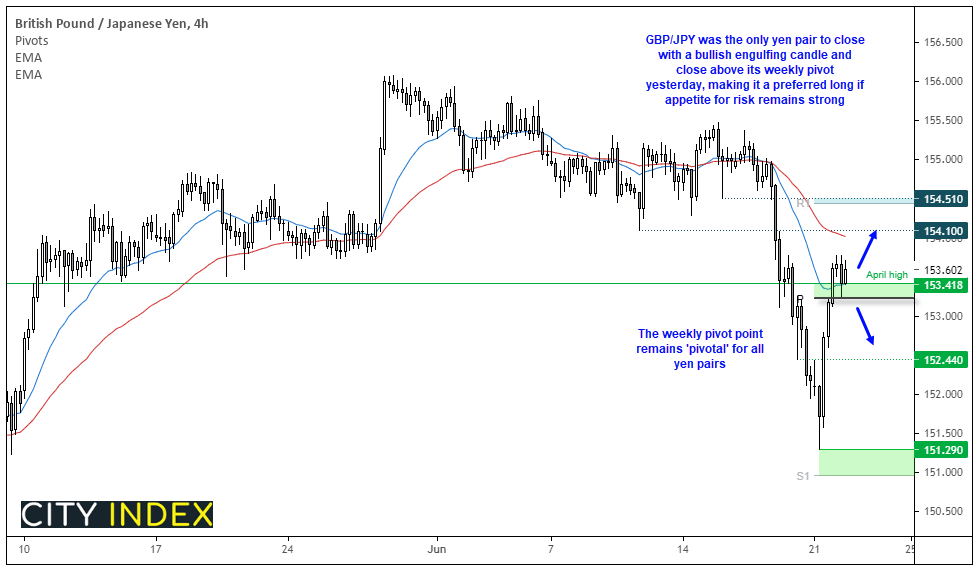

AUD/JPY would be one of our favoured shorts if sentiment soured, as yesterday’s rebound has met resistance at its weekly pivot point (83.26) and the four-hour 20-bar eMA. NZD/JPY is a similar setup, so much the muchness. However, if risk appetite continues to improve then our preferred long would be GBP/JPY as it is the only major to form a bullish engulfing candle yesterday and close above its weekly pivot point.

We can see on the four-hour chart that a V-bottom formed and traded above the weekly pivot. Given a retracement has since confirmed that level as support and remains above the 20-bar eMA, our bias today remains bullish above the 153.22 pivot point. If prices can break above yesterday’s high then bulls could target 150.00/10 (near the 50-day eMA) or the resistance zone around 154.51.

Learn how to trade forex

Commodities slowly on the rise

Copper prices are probing the 100-day eMA (from below) after printing a small but potentially important bullish engulfing candle. That it follows after a small Doji shows bearish momentum was already waning on Friday despite the strong dollar on that day. Today’s bias is bullish and a target could be the broken trendline from the October low on the daily chart.

Gold futures rose a further 0.4% to a two-day high after printing its own bullish engulfing candle yesterday. Its next major resistance level is 1800, whilst its 200-day eMA is 1811 and its 100-day sits at 1823.

Brent futures are probing the YTD high at 47.95 amid its third bullish session. Given the supporting fundamentals, established bullish trend and potential for a weaker US dollar then a breakout could be on the cards. Its next resistance level is the 2019 high at 75.58.

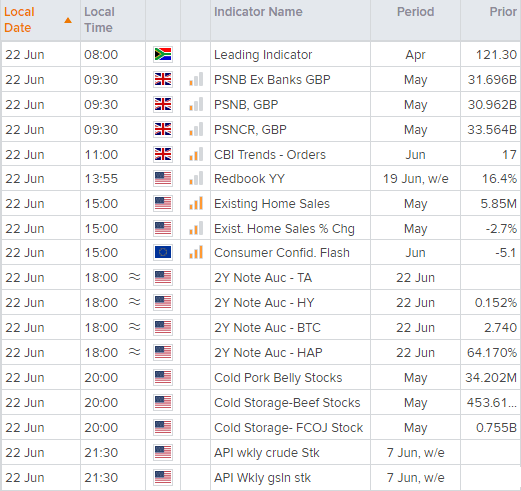

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM