European markets fell back on Tuesday as investors locked in some gains after Draghi announced last week plans to launch ‘Outright Monetary Transactions’ and weaker than expected US non-farm payrolls raised expectations of additional stimulus from the US Federal Reserve.

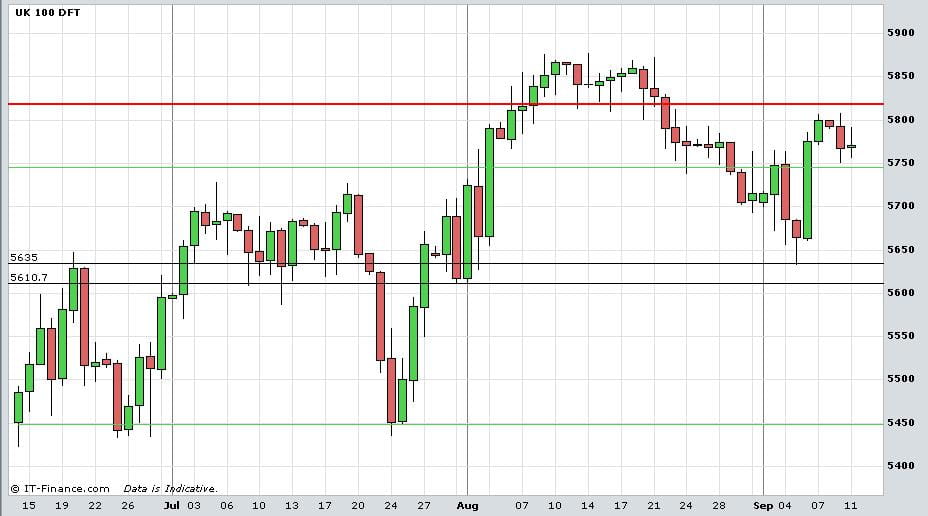

The FTSE 100 has struggled to push on above resistance levels of 5800, whilst imminent decisions over the next few trading days has also convinced traders to lock in their gains over the past 24 hours, with the UK Index falling back by 0.4%. Resistance levels of between 5634 and 5610 need to be watched carefully for a break below, which could indicate that UK equities may encounter further pressures.

Chart: FTSE 100 (Daily)

There are a number of things investors need to be mindful of when trading the markets this week.

First and foremost, the return of trading volumes in the market place. As expected, with the summer lull now over and investors returning to their desks (I personally witnessed the lack of yacht owners in St Tropez last weekend), volumes are starting to pick up with vigour and this helps to paint a much more transparent picture of true market sentiment. Friday’s trading session saw the heaviest amount of volumes since the end of May.

Secondly, we have two key decisions to come this week. Tomorrow, the German constitutional court is expected to approve the European Stability Mechanism, the new and permanent euro zone bailout fund, and the greater budgetary discipline required for a ‘fiscal compact’ and by doing so, reject injunctions made by thousands of people complaining Germany’s participation undermines the constitution.

A rejection of the fund itself would be a huge surprise to the markets and likely trigger large bouts of market volatility as it would essentially restrict Germany’s participation in the fund, which is essentially the engine room for any euro zone bailout.

A rejection is not expected, but then again, we have seen surprises beforehand. Alongside the likely approval however may come with certain conditions that give the country greater security and allies some of the fears made clear by the injunctions. Make no mistake, the ESM cannot happen without Germany’s involvement. The market required clarity at all times and hates uncertainty. To that end, if there is certainty from tomorrow’s decision in a positive way, that is likely to remove an air of trepidation from the markets.

On Thursday we also see the culmination of a two day FOMC meeting, which comes hot on the heels of disappointing non-farm payrolls data last week for August, which saw a mere 96,000 jobs created against expectations of 163,000, though the unemployment rate did surprisingly fall back to 8.1%.

A key element will be whether the Fed decide to do anything on the stimulus front. A recent Reuters poll showed that there is a 60% of QE3 being announced this week, yet I personally would put myself in the 40% bracket for no announcement. Recent improvements in economic data out of the US – barring the non-farm disappointment – may threaten any imminent announcement of QE3.

The Fed have proved in the past to be aggressive when they need to be however and with the US presidential election to come in November, the timing of any additional stimulus could be just as important economically as politically. We could hear the Fed detail guidance beyond 2013 too. Bernanke’s press conference that follows the decision will certainly be one not to miss though.

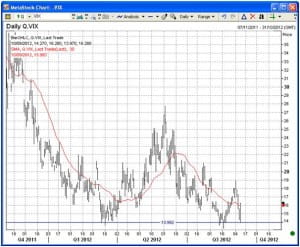

And finally, the Volatility Index, a key gauge of market fear or pessimism, enjoyed its biggest daily gains in Monday’s trading session since 23rd July, bouncing from long term support levels and closing above its 30 day moving average. A rallying VIX is typically a bearish indicator for equity markets and though whilst yesterdays jump does not indicate an impending market correction yet, it is certainly something worth watching given the previous correlations with equity market corrections.

Chart: S+P Volatility Index