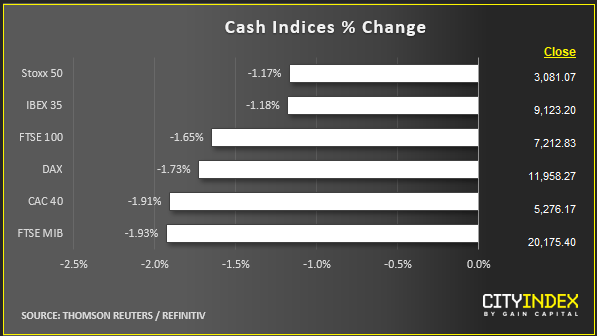

Stock market snapshot as of [23/5/2019 3:22 PM]

- Things are not looking up yet, and U.S. stocks have joined global shares in a fourth declining session out of five.

- It is almost classic ‘risk off’, with gold and the yen dutifully rising on demand for their perceived ‘safety’

- Further confirmation comes from currencies, where dollar appreciation ensues by default as traders hollow out prospects for most minor and many major currencies, save for Japan’s yen, and the HKD

- The news vacuum that may or may not be broken much before Presidents Trump and Xi are meant to meet in June, isn’t helping. In the place of fresh developments, two opinion pieces in the Communist Party’s flagship paper took aim at Washington’s recent curbs on Chinese technology companies. Does anyone still believe Huawei, ZTE, Chinese video surveillance firm Hikvision and others, have nothing to do with how markets perceive the trade dispute?

Corporate News

- Tesla is among the standouts to the upside—and to the downside. It looked set to break a six-session session losing streak for a spell, paring a 40% loss in the year so far, that makes it one of the worst trade-war casualties among bedraggled autos

- An email to employees by its colourful CEO, Elon Musk, said the electric car maker has a “good chance” of exceeding the record 90,700 deliveries the group achieved in the fourth quarter. Volatile action saw the stock down as much as 3.5%. It then rose more than 4% a little ago and subsequently relinquished almost all of that gain

- Victoria’s Secret parent L Brands, Best Buy and med-tech group Medtronic all shone after solid earnings. As such, blanket selling is off the cards, for now

- Still, the VIX volatility ‘fear gauge’ has confirmed good support around the 15 level with a 17% bounce

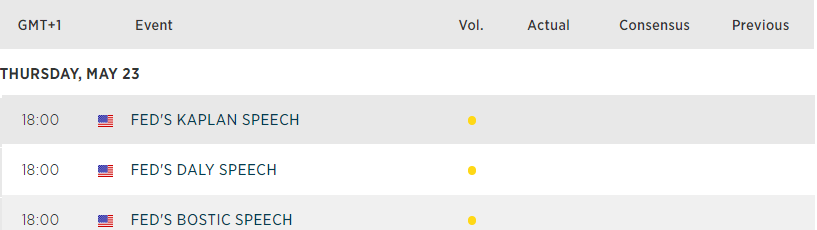

Upcoming economic highlights

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest China articles

March 26, 2024 04:11 AM

March 13, 2024 04:47 AM

March 6, 2024 05:47 AM

February 22, 2024 01:21 AM