Perhaps the best that can be said about Europe’s take on the global rebound is that it may not turn out to be any more deluded than elsewhere

Europe’s bounce is proving resilient so far on Wednesday. Markets were off highs a bit earlier, though DAX was up 0.4%, with France’s CAC-40 up 0.6% and the broad STOXX counter holding around 0.5% better on the day. ‘Risk assets’ are thereby doing little more than follow counterparts in other world regions with a positive reaction—possibly an over-reaction—to Fed chair Jerome Powell’s mild hint that the bank could cut rates if “appropriate”.

- Resilience shows in Europe’s broad response to Italy news. The FTSE MIB index underperforms after the European Union confirmed disciplinary procedures. After frequent signals from Brussels though, this is not a surprise. BTP futures dropped and hypersensitive Italian bank shares slumped, but tell-tale yield spreads barely flashed alerts. Prime Minister Giuseppe Conte, an essentially neutral figure, had couched a request this week for confirmed backing from his two coalition leaders as a demand for squabbling to end. Both endorsed the coalition. Tacitly that includes Conte too. He has repeatedly signalled adherence to the EU’s mandate. A punishing EU fine (at worst) may still be forthcoming, but some of the sting has been removed

- A lacklustre raft of closely-watched PMI gauges was also absorbed in glass-half-full-manner. The ‘stand-out’ German performance was just 0.4 of a point above consensus but at least firmly on the ‘growth’ side at 55.4, hence reassuring in context

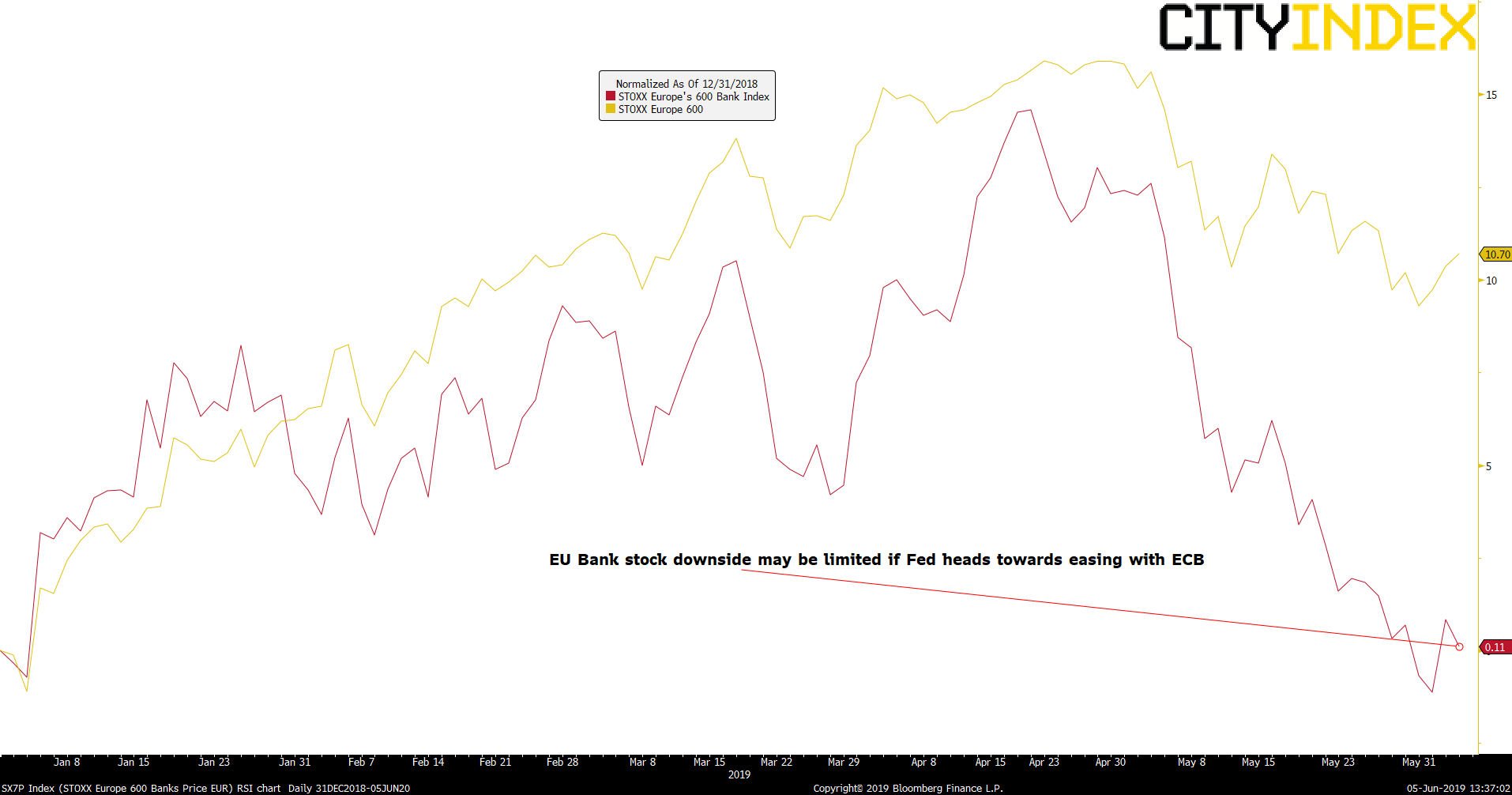

- With one of Europe’s least loved sectors, banks, sitting on a gain of almost zero in 2019 (according to the STOXX sub-index) few flies in the ointment can truly hurt the uplift at this point. Chiefly, the euro’s sneak higher has been met in relaxed fashion. Expectations of generous ECB loan terms at the margin could yet disappoint relative to EUR/USD’s 1.6% advance from late-May lows when Draghi unveils them on Thursday. But the let-down doesn’t have far to fall. And it may be arrested at any time with ECB policy now looking like a work-in-progress

Normalised stock index chart: STOXX Europe 600 Banks; STOXX Europe 600 – year to date

Source: Bloomberg/City Index

- More generically, European shares are, like Wall Street and Asia Pacific counterparts, taking the opportunity to smooth imbalances from over a month of selling. Technology and hardware shares are out in front as investors seek out likeliest bargains. Other ‘heavy’ industries like mining, metals, transportation, capital goods and of course, automobiles also enjoy a bias

In essence, should the stock market come-back be confirmed—another way of saying if global monetary policy really has turned accommodative—there are decent signs European stocks can continue to participate.

Whilst Powell’s comments remain arguable as a definitive bringer of relief, his adroit switch of focus from “patient” to “as appropriate” has proven to be enough, for now. Should markets’ reaction turn out to a misinterpretation, European shares won’t be spared. But at least the relapse will be no more punishing than elsewhere.

Latest market news

Latest Indices articles

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM