Europe will like a Clinton victory more by November

If Democratic nominee Hillary Clinton is widely viewed as the ‘winner’ of the first election debate, why are stocks selling off again?

If Democratic nominee Hillary Clinton is widely viewed as the ‘winner’ of the first election debate, why are stocks selling off again?

Demand for risky assets like equities and commodity linked-currencies was only momentarily swayed by last night’s key battle in the fight for the White House.

European equity sentiment continues to hinge more on long-standing themes like dollar strength, oil weakness and global growth worries.

After all, this side of the Atlantic, a hyper-waspish debate in the early hours between the outsize TV personality and US political royalty, was more akin to entertainment than a ‘must watch’.

At its open, Europe did react to the knee-jerk comeback of Asian shares overnight. That set Germany’s DAX, the FTSE 100, and the broad STOXX 600 on the front foot as trading got under way.

But the good cheer was fleeting.

Beyond Clinton’s studiously rehearsed (and exquisite) put down on ‘stamina’ and Trump’s legally watertight ‘smart tax retort’, we learned little about their personalities or potential policies we didn’t know already.

Trump’s blustered jobs-creation elevator pitch was well and good—tax cuts for the rich would redirect “billions and billions into companies”; slashed corporation tax would entice $2 trillion back into IRS coffers. But he didn’t sketch how he’d make these goals happen.

Conversely, Clinton’s shopping list of spending on infrastructure, clean energy, minimum wage, and education by taxing the rich more, would indeed aid the many. Too bad her plans on how to steer this comprehensive fiscal commitment through a still GOP-dominated Congress after 8th November, remained a mystery.

In the end, the weak ‘risk’ rally and rebound in Clinton’s poll lead that Europeans awoke to were not enough to buffer sentiment.

They were no match for continuing signs of corporate (if not financial) stress at the heart of Europe and no let-up in volatile oil trading.

Come a cold corporate winter in Europe, the least-disruptive option for President will be welcomed more wholeheartedly than Tuesday’s trading suggests.

Clinton’s debate performance was clearly more of a big deal for some markets than others. Mexico’s peso, for instance, the so-called ‘Trumpometer’, continues to hold on to its earlier bid at the time of writing, grabbing back two-day’s worth of losses against the dollar in one session.

Another probable proxy, the Canadian dollar, has been more of a ditherer, given strong ties to oil. The latest upsurge in oil price volatility has stymied the loonie’s attempts to break the greenback’s five-day ascent.

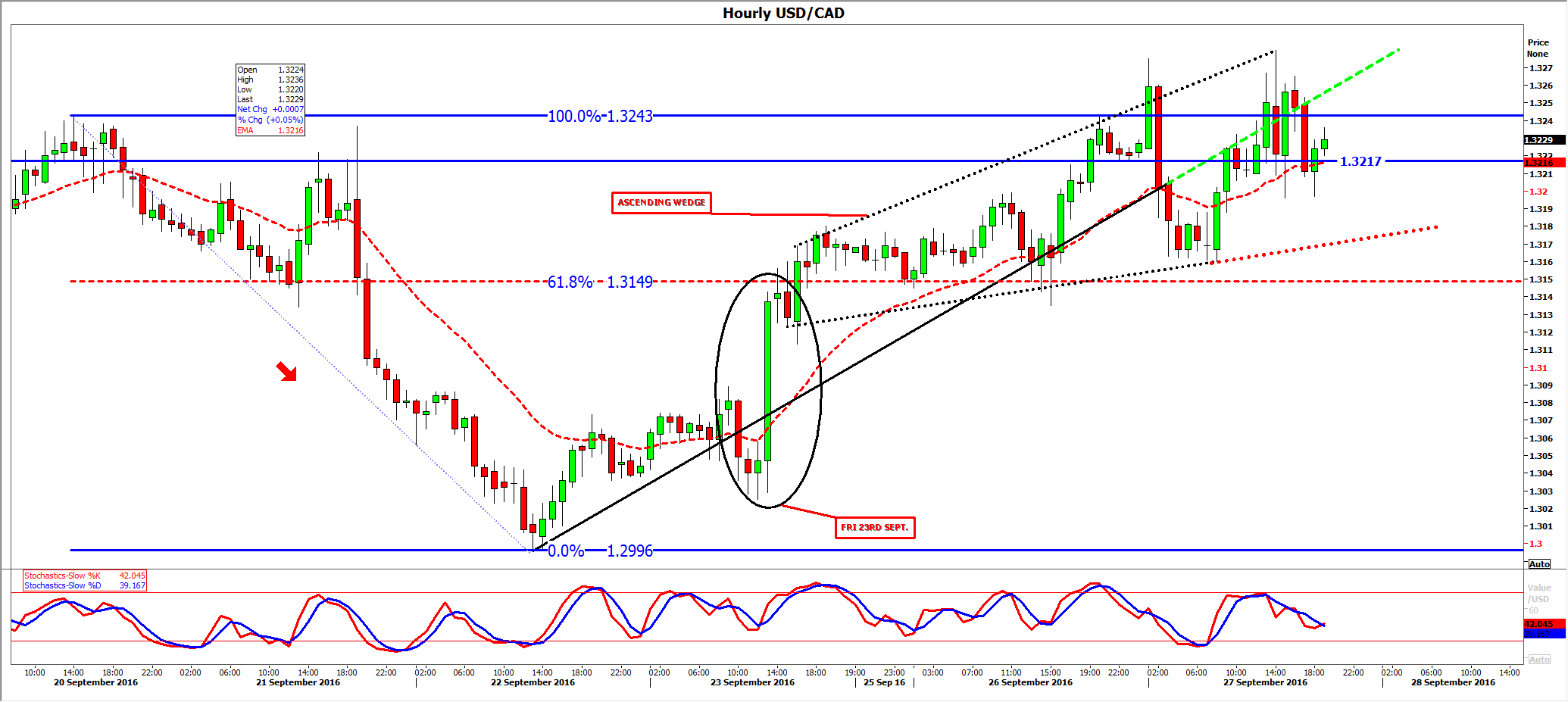

From a technical perspective, however, the Canadian dollar’s chances of limiting that trend to the short term look more even.

USD/CAD managed a sharp spike lower around the start of the debate but it has been hugging the rising trend in our hourly chart below since then.

In fact, the C$1.32 resistance line will be familiar to long-standing traders of this pair.

Since a break down in late-March, and an immediate dollar fight-back in early April, two strong challenges followed by eventual failure of the greenback and a loonie bounce were seen between 25th-27th July and 15th-21st September.

Prices tagged the underside of the pair’s 21-day exponential trend (red dotted line) around the time of writing, whilst an expanding wedge pattern—typically bearish when pointing upwards—was formed between last Friday and online time.

Obviously, the ability of C$1.3217 to keep a lid on the US dollar will set up a drive back to the lower bound of the wedge.

Soon after that, USD/CAD will face a strong challenge from 61.8% of slide last week.

Should that level (C$1.3149) give, this time, bears will exploit the relative vacuum back down to C$1.3029, the base of the dollar’s Friday surge, with an eye on C$1.2996, where the dollar rallied.

A sustained upside breach of C$1.3217, and of the loonie’s 20th September failure high (C$1.3243) could bring the late-July peak at C$1.3251 back into play.

Please click image to enlarge