European bourses are looking to extend gains for a third straight session on Thursday as optimism over the reopening of economies once again overshadows rising tensions between the US and China over Hong Kong.

Last night, Washington took steps towards potentially removing the city’s special trade status. US Secretary of State Mike Pompeo said that the US no longer views Hong Kong as autonomous from mainland China. This has been the most serious response from the Trump administration over China’s crackdown on civil liberties in the financial hub.

The backdrop of cooling relations between US and China could limit gains, but we are not seeing that here is Europe at the moment. Instead stocks are bounding higher on the expectations that consumers will be coming out of lock down with an increased desire to spend, making up for those months stuck at home. This rally does of course assume that consumers will feel financially confident to continue spending.

EC’s rescue fund

The European Commission’s announced rescue fund is also going some way to boost sentiment on the continent. The fund will include €500 billion raised on the bond market. Given the size of the crisis that is hitting the region, the sums involved are small. However. it is the move towards financial integration that is being cheered by investors. This marks a clear turning point in policy.

The European Commission’s announced rescue fund is also going some way to boost sentiment on the continent. The fund will include €500 billion raised on the bond market. Given the size of the crisis that is hitting the region, the sums involved are small. However. it is the move towards financial integration that is being cheered by investors. This marks a clear turning point in policy.

Day ahead

Looking ahead, US data releases will be in focus, with Q1 GDP, US Durable goods and jobless claims taking centre stage. The numbers are expected to be dire, with Q1 GDP to confirm -4.8% contraction on annualised basis, and Durable goods to decline by a record -19%. Worryingly initial jobless claims are expected to remain over 2 million. There will also be a growing focus on continuing claims for signs of rehiring as states ease lockdown measures to reopen the economies.

Looking ahead, US data releases will be in focus, with Q1 GDP, US Durable goods and jobless claims taking centre stage. The numbers are expected to be dire, with Q1 GDP to confirm -4.8% contraction on annualised basis, and Durable goods to decline by a record -19%. Worryingly initial jobless claims are expected to remain over 2 million. There will also be a growing focus on continuing claims for signs of rehiring as states ease lockdown measures to reopen the economies.

Oil drops on larger than expected stockpiles

Whilst European futures are charging higher and US futures to a lesser extent, oil markets are extending yesterday’s steep losses. Hopes of a smooth recovery for oil from the coronavirus lockdown were dashed after oil inventories rose by more than expected.

Whilst European futures are charging higher and US futures to a lesser extent, oil markets are extending yesterday’s steep losses. Hopes of a smooth recovery for oil from the coronavirus lockdown were dashed after oil inventories rose by more than expected.

Data from API revealed that inventories rose by 8.7 million barrels compared to expectations of a 1.9-million-barrel draw. Gasoline stocks also rose by 10 times what analysts had been expecting. These are big misses and show that whilst demand is on the road to recovery, it will be a very rocky road and is still some way off from sustaining prices.

The worse than feared US oil stockpiles added to growing nerves over Russia’s commitment to deep oil production cuts ahead of June 9th OPEC+ meeting. The last thing the oil market needs right now is another standoff between Russia and Saudi Arabia. It was the straw that broke the camel’s back in March and with demand still so fragile any further signs of Russia not being onboard with supply cuts could see oil quickly break through support at $30 per barrel.

WTI shed 4% in the previous session and is down 3% at the time of writing.

WTI shed 4% in the previous session and is down 3% at the time of writing.

Oil levels to watch

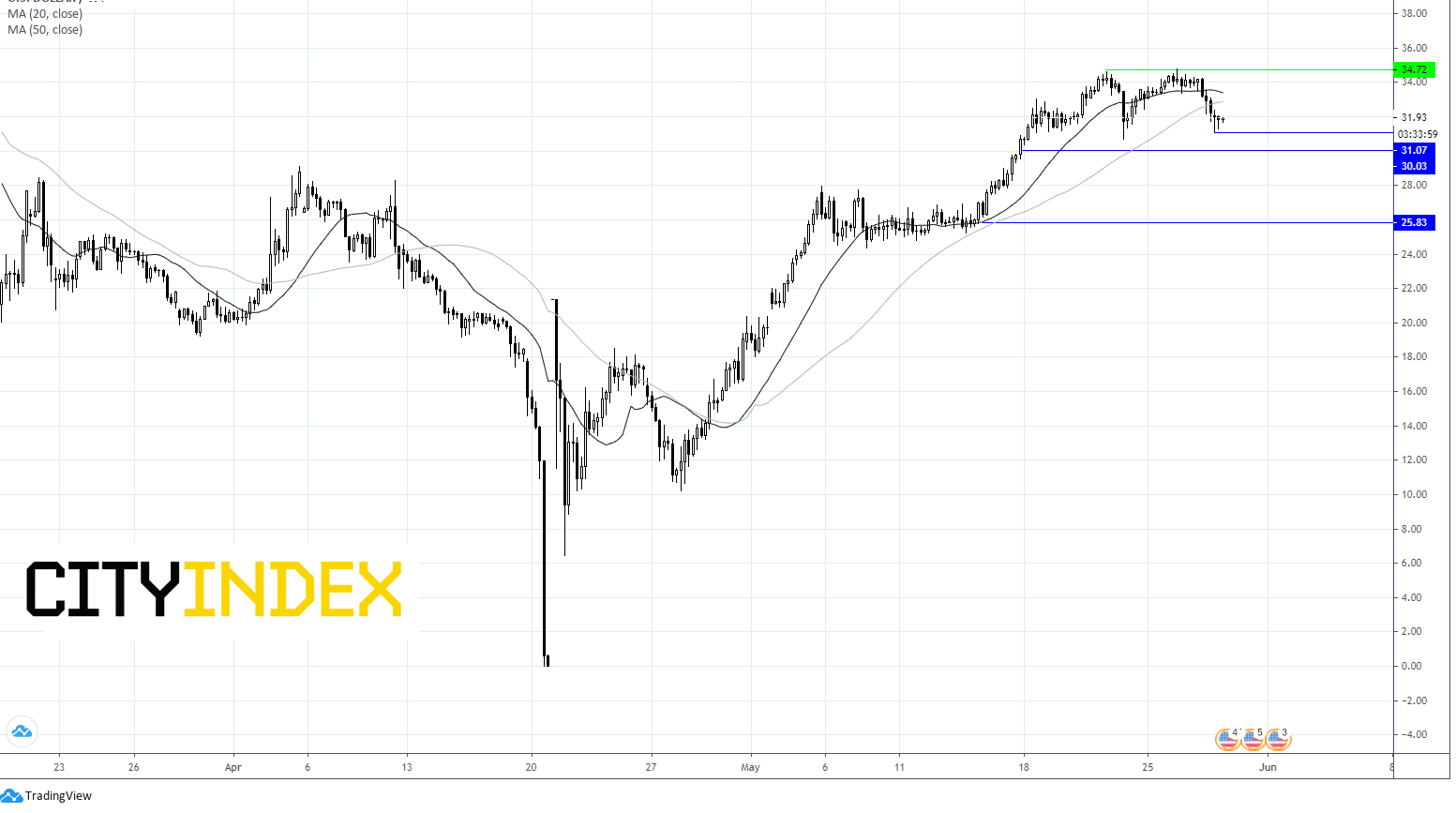

WTI’s rally look s like it is stalling. The stock trades below its 20& 50 sma on 4 hrs chart.

Immediate support can be seen at $31.16 (today’s low) prior to $30 psychological level and $25.80 (low 14th May).

Resistance can be seen as $32.70 (50 sma) and $33.50 (20 sma) prior to $34.70 (high 26th May)

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Indices articles

Yesterday 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM