An upbeat session in Asia is set to spill over into Europe, with European stocks pointing to a positive start, extending gains from the previous session. Optimism surrounding the reopening of economies, upbeat Alphabet revenue and a surge in the price of oil are doing the heavy lifting this morning.

Risk assets remain in favour as the broad mood in the market is in a significantly better place than a month ago. At the end of March, many countries were at the beginning of lockdown and there were too many unknowns. Fast forward a month and economies are gradually reopening, news surrounding potential treatments and progress towards a vaccine has also helped improve the mood, as has a heavy dose of fiscal and monetary stimulus to help cushion the economic blow from the coronavirus crisis.

Rally to stall?

That said there are still many unknowns, perhaps too many to justify the return to a bull markets for many bourses across the globe. The true scale of the economic impact of the coronavirus is still unknown. Whilst people returning to work and economies reopening is a good thing, there is a good chance that the rally will start to stall over the coming weeks, as investors are faced with the stark reality of the hard data whilst also waiting to see if the gradual reopening are working.. Investors face the same conundrum as governments; will the reopening prove successful or lead back to a second wave of infections?

That said there are still many unknowns, perhaps too many to justify the return to a bull markets for many bourses across the globe. The true scale of the economic impact of the coronavirus is still unknown. Whilst people returning to work and economies reopening is a good thing, there is a good chance that the rally will start to stall over the coming weeks, as investors are faced with the stark reality of the hard data whilst also waiting to see if the gradual reopening are working.. Investors face the same conundrum as governments; will the reopening prove successful or lead back to a second wave of infections?

US GDP & Fed

Attention will now shift towards UD GDP and Federal Reserve FOMC announcement. Of the two events, the GDP has more market moving potential. The Fed are not expected to move on rates. Recently, if the Fed wants to move, it doesn’t wait for the monthly meeting.

Q1 US GDP, will shed some light on how badly the coronavirus crisis hit the US economy. There were only two full weeks of lock down included in Q1. A worse than forecast GDP reading will stoke fear in the markets that the Q2 numbers will be even worse.

Investors will look to the Fed for guidance as to what to expect for the economy this year. How deep does the Fed envisage the Covid-19 contraction being and how long do they intend to keep rates at 0? Whether Fed Chair Jerome Powell emphasizes a long slow slug higher for the economy or an optimistic quick rebound will set the tone for the market.

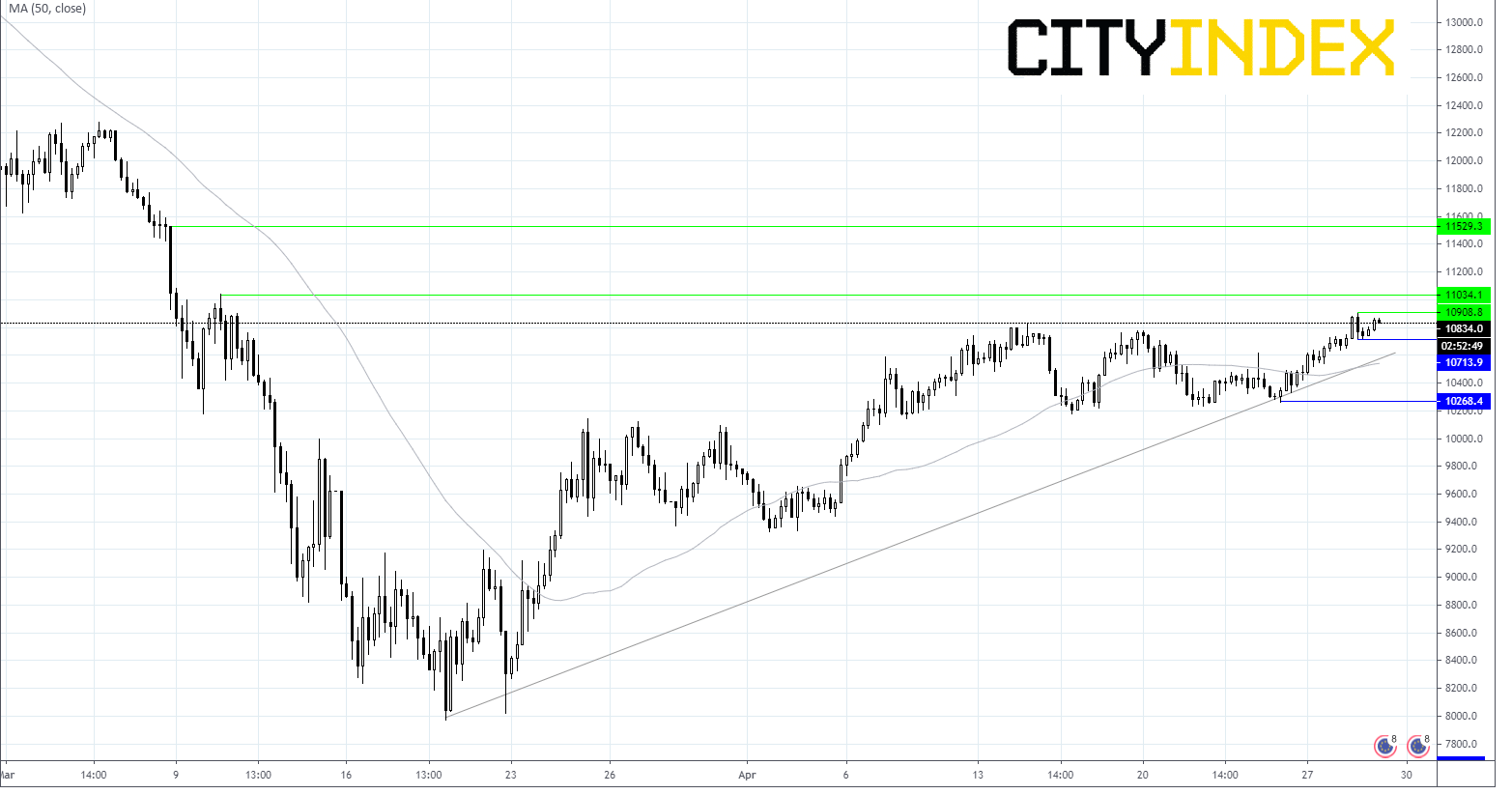

Dax levels

Dax remains in an uptrend, supported by a trend line from March low. Immediate resistance can be seen at 10901 (yesterday’s high) prior to 11034 (high 10th March)

Immediate resistance is seen at 10719 (low yesterday) prior to 10595 (trend line support).

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Indices articles

Yesterday 03:30 PM

April 18, 2024 04:46 PM