European stocks are pointing to a mixed start amid a cautious mood in the market. Whilst economies across the region are gradually starting to reopen boosting optimism of an eventual return to normality, oil continues to tank unnerving investors.

Nervous Openings

Europe is gradually releasing virus curbs. Spain and Italy the two hardest hit countries in Europe are due to lay out plans to loosen virus restriction as leaders are keen to get the economies back up and running. Italy could soon join countries such as Germany, Netherlands and Austria and allow Italians out onto the streets for the first time in weeks. However, the easing of restrictions comes with a heavy dose of weariness. The markets have managed an impressive run from mid March's low and the S&P is now only 20% away from its all time high. However, this run higher has been based on optimism that economies can quickly reopen and return to some form of normality. A second wave of infection would smash that optimism and send riskier assets sharply lower again.

Europe is gradually releasing virus curbs. Spain and Italy the two hardest hit countries in Europe are due to lay out plans to loosen virus restriction as leaders are keen to get the economies back up and running. Italy could soon join countries such as Germany, Netherlands and Austria and allow Italians out onto the streets for the first time in weeks. However, the easing of restrictions comes with a heavy dose of weariness. The markets have managed an impressive run from mid March's low and the S&P is now only 20% away from its all time high. However, this run higher has been based on optimism that economies can quickly reopen and return to some form of normality. A second wave of infection would smash that optimism and send riskier assets sharply lower again.

WTI Dives Amid Heightened Storage Concerns

Oil prices have been closely tied to sentiment across the past few weeks. Whilst stocks rallied in the previous session despite the price of oil tanking, that is not proving so easily achieved today. Oil has dumped another 12% in early trade, adding to the 23% decline from Monday, on dwindling crude storage capacity.

With OPEC+ cuts not due to start until 1st May, combined with the fact that economies are reopening gradually, a realisation is hitting that any increase in oil demand will be gradual rather than a sudden jump to pre-coronavirus levels. Furthermore the 10 million bpd cut doesn’t even scratch the surface of the 30 million bpd hit to demand that lock down is estimated to have caused.

Part of the decline in WTI is owning to retail investment vehicles, such as ETF’s selling out front month June contracts and buying into later months to avoid the massive losses seen last week when the May contract dived below 0.

Oil prices are a reflection of supply and demand. Simply there is too much oil for the reduced and only very gradually increasing demand. Inventory numbers will be very much in focus this week, particularly at Oklahoma Cushing storage, which is set to reach full capacity as soon as mid-May.

HSBC Profits Dive 48%

HSBC was the first of the big UK banks to report and the numbers made for grim reading. Given the state of the economy and lack of visibility ahead bank’s earnings are all about loan loss provisions. Profits halved as the bank to $3.2 billion, below expectations, as bad loan provisions were beefed up to $3 billions owing to covid-19 impact and the collapse in oil price. Without naming names, HSBC alluded to the inclusion of a charge for Hin Leong Trading, the oil trading company which is restructuring billions of dollars of debt.

These results will encourage HSBC to press ahead with its restructuring plan. Cutting costs, stripping out management levels and shifting capital from under performing parts of the business has never been so crucial.

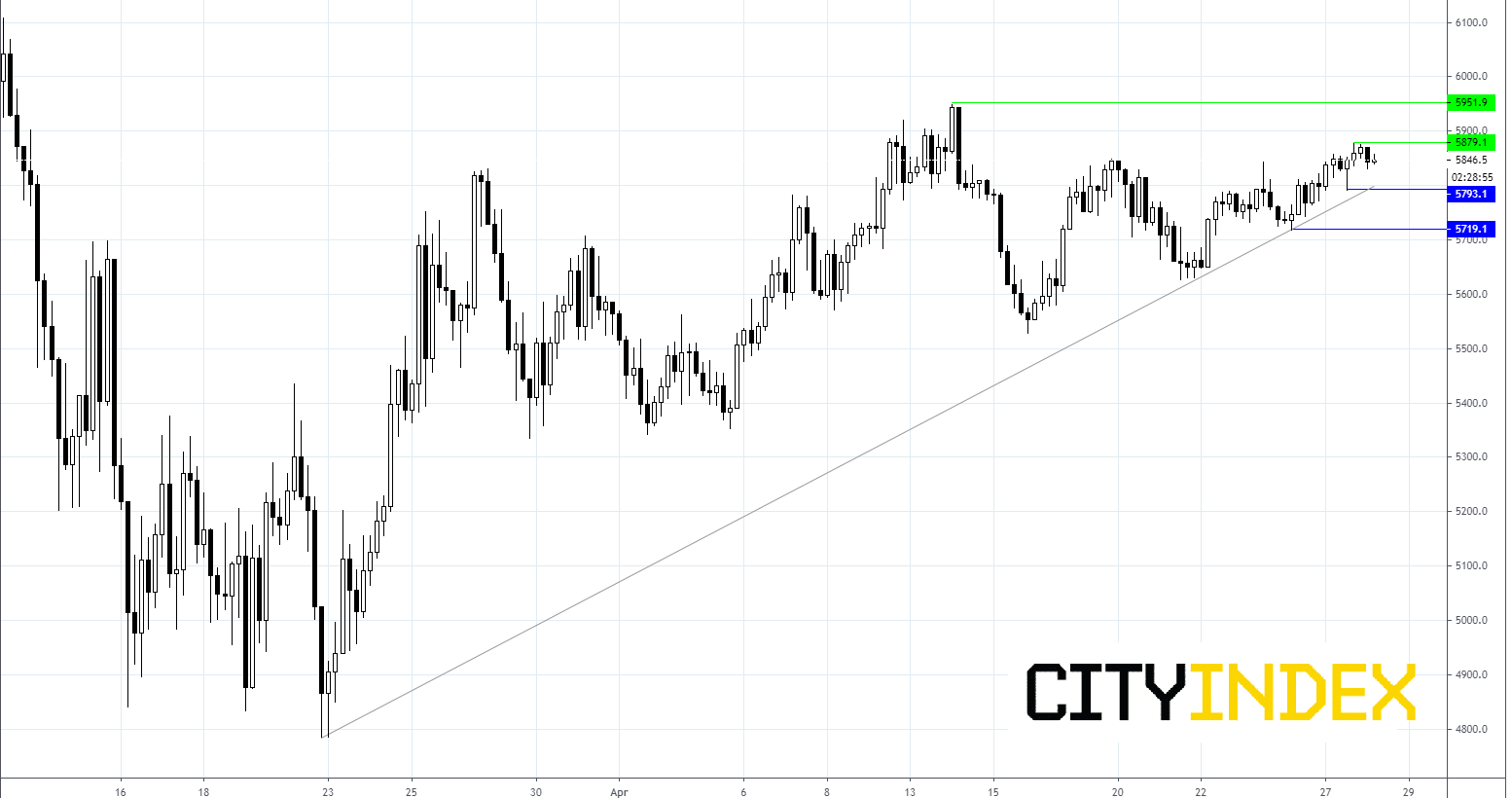

FTSE Chart

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM