European markets are pointing to a weaker start in a flight to safety as covid cases surge, lockdowns tighten and as investors brace themselves for what is expected to be a volatile week ahead with the US elections, BoE, FOMC and non-farm payrolls.

UK going into lockdown

Coronavirus cases continue to spiral out of control, so much so that the UK joins France and Germany by announcing national lockdown 2.0.

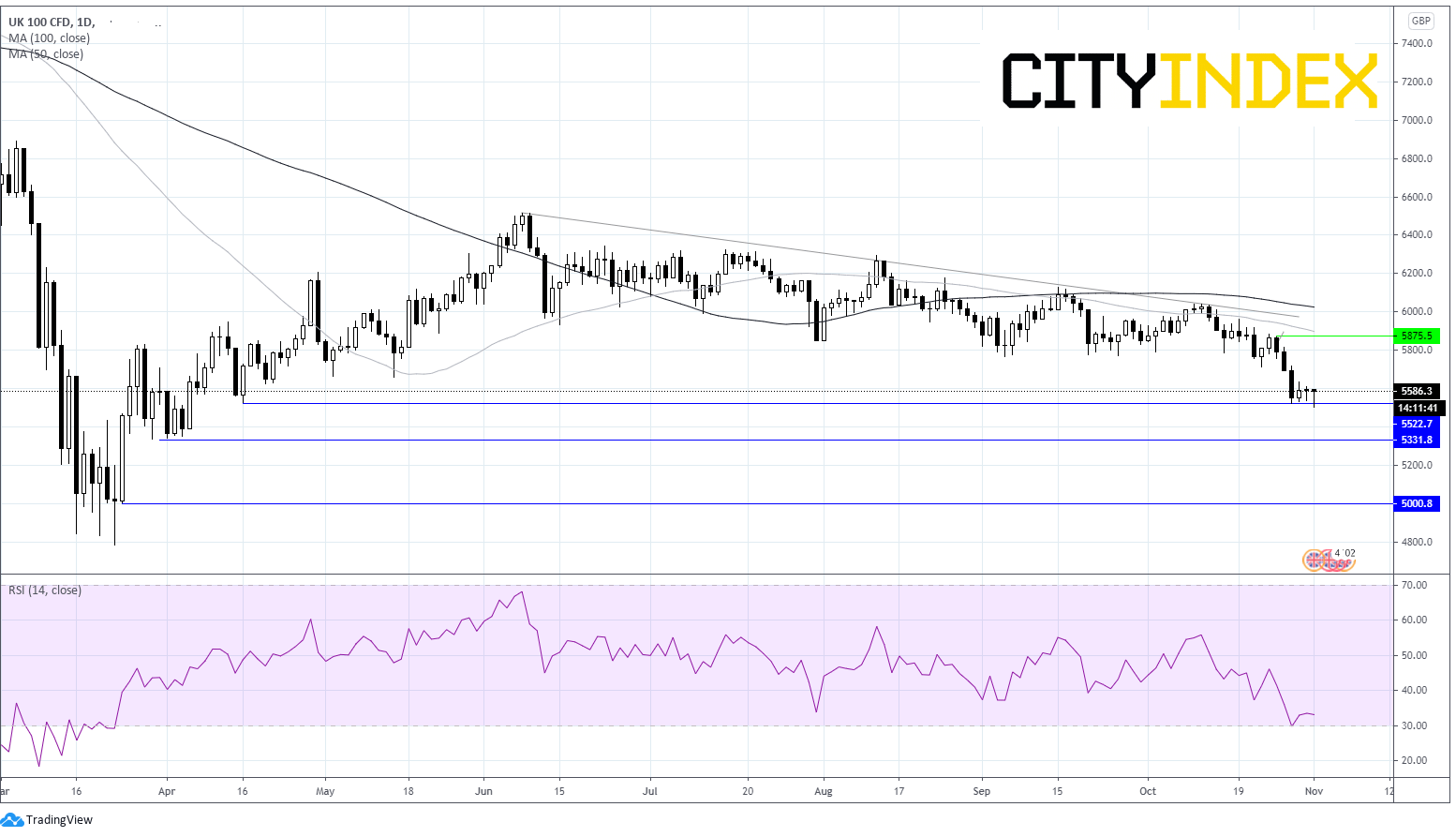

The FTSE is a notable laggard versus its European peers after Boris Johnson’s spectacular U-turn ordering another national lockdown from Thursday. Retailers will be in focus and as they are expected to face a Christmas disaster after the government ordered the lockdown of all non-essential shops. Tighter travel restrictions will also mean that travel firms will once again be under pressure as the covid trade returns.

Coronavirus cases continue to spiral out of control, so much so that the UK joins France and Germany by announcing national lockdown 2.0.

The FTSE is a notable laggard versus its European peers after Boris Johnson’s spectacular U-turn ordering another national lockdown from Thursday. Retailers will be in focus and as they are expected to face a Christmas disaster after the government ordered the lockdown of all non-essential shops. Tighter travel restrictions will also mean that travel firms will once again be under pressure as the covid trade returns.

Ryanair cuts capacity expectations again

Ryanair confirmed the disastrous outlook for the sector announcing that it now expects to fly at just 25% -40% of potential capacity over the winter months, depending on how covid develops. This winter as good as a complete write off for airlines. The dismal outlook comes as the budget airline revealed a €197 million loss in the first half compared to a profit of €1.1 billion in the same period last year. It also reported that passenger numbers tanked 80% to 17 million during the pandemic. Ryanair was unable to given guidance for the full year to the end of March, only to say that it expected losses to widen.

Ryanair confirmed the disastrous outlook for the sector announcing that it now expects to fly at just 25% -40% of potential capacity over the winter months, depending on how covid develops. This winter as good as a complete write off for airlines. The dismal outlook comes as the budget airline revealed a €197 million loss in the first half compared to a profit of €1.1 billion in the same period last year. It also reported that passenger numbers tanked 80% to 17 million during the pandemic. Ryanair was unable to given guidance for the full year to the end of March, only to say that it expected losses to widen.

China’s recovery continues

Upbeat data from China is at least offering some support to market sentiment ahead of manufacturing PMI data from Europe and the US.

China’s manufacturing sector expands for a sixth straight month as the pandemic fallout eases, whilst in Europe it worsens. The Caixin/Markit PMI printed at 53.6 in October, better than the 53 expected. This is the highest reading since January 2011 and confirms that the Chinese economy is well on the road to an economic recovery. The hope is that the strengthening Chinese economy will help spare Europe from some of the inevitable economic suffering as nations head back into lockdown 2.0.

Upbeat data from China is at least offering some support to market sentiment ahead of manufacturing PMI data from Europe and the US.

China’s manufacturing sector expands for a sixth straight month as the pandemic fallout eases, whilst in Europe it worsens. The Caixin/Markit PMI printed at 53.6 in October, better than the 53 expected. This is the highest reading since January 2011 and confirms that the Chinese economy is well on the road to an economic recovery. The hope is that the strengthening Chinese economy will help spare Europe from some of the inevitable economic suffering as nations head back into lockdown 2.0.

Manufacturing PMI in focus

Manufacturing PMI data will be in focus for Europe and the UK. The manufacturing sector has proved to be much more resilient to the impact of the pandemic than the service sector. The most recent flash manufacturing PMI readings from the Eurozone and from the UK showed robust expansion n the sector despite surging covid cases. This is of course now likely to change as lockdown restrictions are imposed once again.

FTSE Chart

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM