After Thursday’s seismic risk off selloff, which saw stocks and oil crash, and safe havens rally, markets are trying to stabilise. European markets are looking to extend losses by around 0.5%, however US futures are pointing to a more upbeat start.

Stocks finally experienced that hefty correction that had been expected the whole run higher. A cautious Fed, gloomy projections and growing fears of a second wave of coronavirus saw European stocks drop the most in two months.

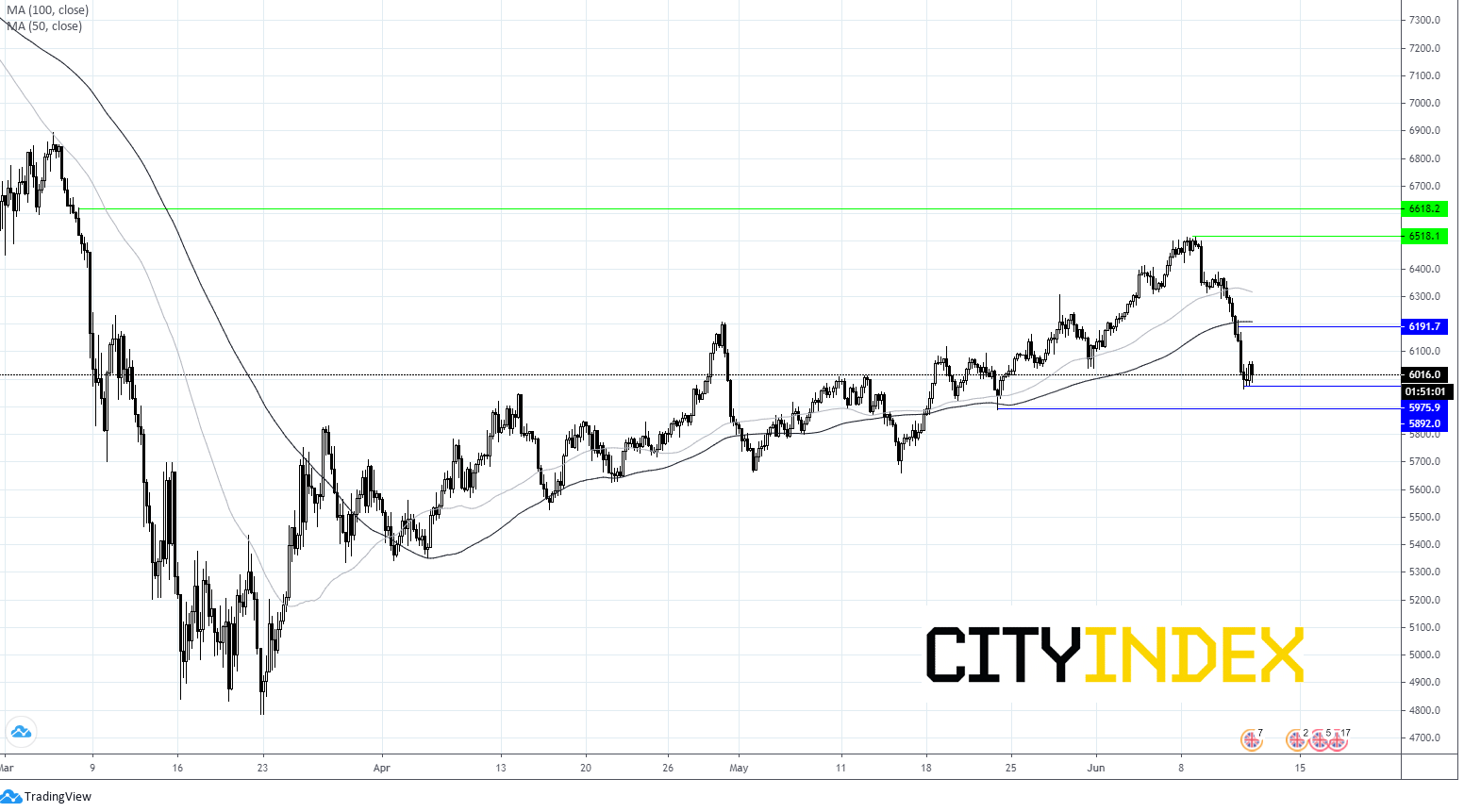

The “only way is up” philosophy that the markets had been following for the past 2 months, which saw the Nasdaq rally to a fresh all time high, the S&P wipe out losses for the year and the Dax come within a few percentage points of the same achievement was contradicted with a massive sell off. The big question now is whether this was just a natural correction is an impressive bull run or whether this is the start of something more sinister – a new bear trend.

Grim milestone & 2nd wave?

Coronavirus numbers are still elevated, with the grim milestone of 7.5 million cases globally being breached. Concerns are growing of a second wave in the US where over 20 states have started to see an increase in covid-19 cases following 5 weeks of falling numbers. Local officials have mention restarting lockdown measures. However, US Treasury Secretary Steve Mnuchin has warned that there won’t be a repeat of the stay at home order, given the impact that it would have on the US economy. The very prospect of another round in the ring with covid-19 sent investors rushing for cover in safe haven assets. The threat of a second wave could dampen the prospect of any push higher in riskier assets and promote a period of consolidation whilst trades wait to see how it plays out.

Coronavirus numbers are still elevated, with the grim milestone of 7.5 million cases globally being breached. Concerns are growing of a second wave in the US where over 20 states have started to see an increase in covid-19 cases following 5 weeks of falling numbers. Local officials have mention restarting lockdown measures. However, US Treasury Secretary Steve Mnuchin has warned that there won’t be a repeat of the stay at home order, given the impact that it would have on the US economy. The very prospect of another round in the ring with covid-19 sent investors rushing for cover in safe haven assets. The threat of a second wave could dampen the prospect of any push higher in riskier assets and promote a period of consolidation whilst trades wait to see how it plays out.

UK GDP

The UK economy contracted by a worst than -20.4% mom in April versus -18.4% expected and down from -5.8% in March. Unsurprisingly retail, travel and hospitality were worst hit, although manufacturing and construction also see significant hits, as the data reflects a full month of lockdown and highlights the uphill struggle that the economy now faces to get back on track. The Pound has shrugged of the record break collapse in economic activity to a degree this is old news and finally marks the nadir.

The UK economy contracted by a worst than -20.4% mom in April versus -18.4% expected and down from -5.8% in March. Unsurprisingly retail, travel and hospitality were worst hit, although manufacturing and construction also see significant hits, as the data reflects a full month of lockdown and highlights the uphill struggle that the economy now faces to get back on track. The Pound has shrugged of the record break collapse in economic activity to a degree this is old news and finally marks the nadir.

US Consumer confidence

Looking ahead US consumer confidence data will be in focus as investors attempt to gauge whether US consumer are ready to get shopping to reigniting the US economy. Expectations are only for a slight lift in morale in June to 75, up from 72.3 in May. A much stronger reading could do some heavy lifting in the market. However, a weaker number could fuel fears over the economic outlook, dragging stocks lower and boosting the safe haven USD.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM