Euro Vulnerable to a Near Term Dip if Q2 GDP Disappoints

Early in tomorrow’s European session, the statistics agency Eurostat will release its flash estimate of Q2 Eurozone GDP. After the first quarter’s solid, if unspectacular, […]

Early in tomorrow’s European session, the statistics agency Eurostat will release its flash estimate of Q2 Eurozone GDP. After the first quarter’s solid, if unspectacular, […]

Early in tomorrow’s European session, the statistics agency Eurostat will release its flash estimate of Q2 Eurozone GDP. After the first quarter’s solid, if unspectacular, 0.4% increase in the flash reading, traders are once again anticipating that the currency union’s economy grew by 0.4% q/q in the second quarter, which represents about a 1.5% annualized growth rate. You would be excused for expressing skepticism that the Eurozone grew at the same pace in Q2 as it did in Q1; after all, Greece was a basket case at risk of getting kicked out of the euro for most of the quarter and China, the Eurozone’s second largest trading partner, saw its economy downshift substantially over the same period.

Indeed as we look at some of the leading indicators for GDP, the balance point toward a potentially disappointing reading. All three monthly Industrial Production reports missed expectations, coming in at -0.3%, +0.1%, and 0.4% in April, May, and June respectively. Retail Sales figures were similarly subdued at -0.8%, +0.7% and +0.2% m/m in the three months. That said, the Eurozone’s PMI figures still point to modest growth, with the Final Manufacturing PMI figures holding around 52 and the Services surveys steady in the 54 area.

Of course, the best leading indicators for Eurozone GDP are the GDP readings of the major Eurozone economies. On that note, both Germany and France, accounting for approximately 50% of the Eurozone’s total production, will release their GDP reports a few hours before the headline figure. Germany, the engine that powers the entire Eurozone, is anticipated to grow at a 0.5% rate, while France is expected to show slower, 0.2% growth. If these figures come out below consensus, it would increase the likelihood of a miss in the overall figure at 9:00 GMT.

In terms of trading implications, traders will view tomorrow’s GDP report through the lens of the ECB’s monetary policy. In the immediate term, the Q2 GDP reading is unlikely to impact monetary policy in the Eurozone; after all, the central bank already committed to maintaining its €60B monthly Quantitative Easing program through September 2016. However, some analysts speculate that timeframe could be extended further, and a below-consensus GDP reading would certainly strengthen their case, likely at the expense of the euro.

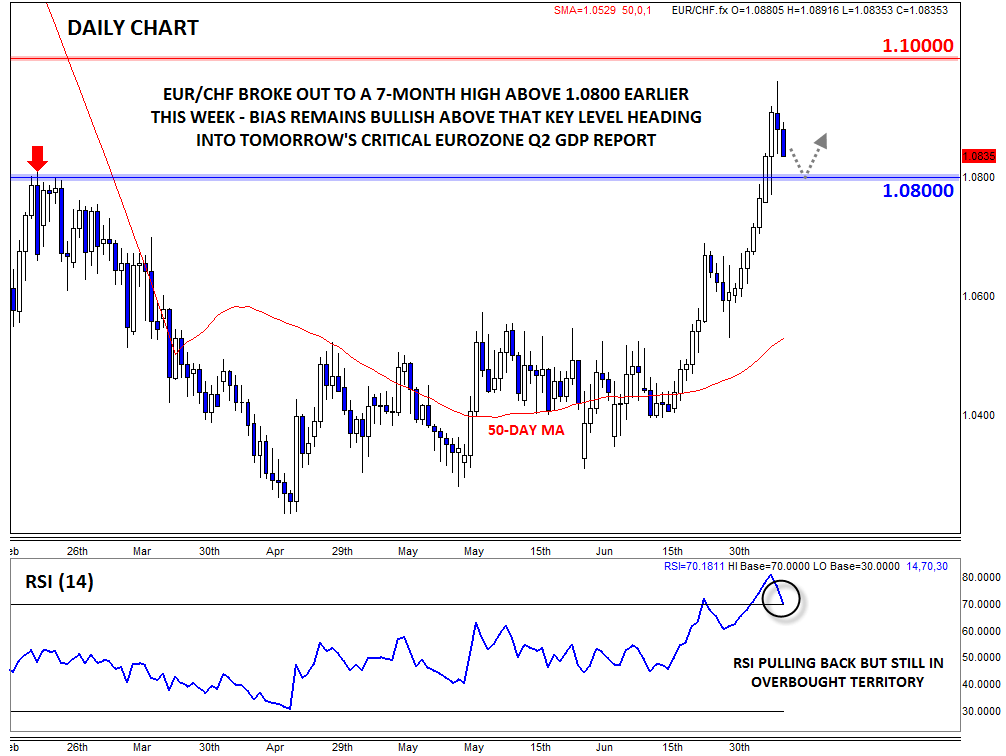

Pair in Play: EURCHF

Perhaps the most interesting pair to watch in the wake of the report will be EURCHF, which exploded out to a seven-month high above 1.0800 earlier this week. The move was driven by the big short squeeze in the euro, as well as a sharp depreciation in the value of the franc as traders abandoned their Grexit safe-haven positions in the currency. In addition, Swiss National Bank member Fritz Zurbruegg emphasized the central bank’s willingness to intervene in order to weaken the currency last weekend, reminding traders that the SNB still wants to see a lower franc.

On a technical basis, the pair is clearly overbought after surging over 400 pips trough-to-peak in less than two weeks, so the pullback over the last 24 hours is hardly surprising. That said, the medium-term trend, backed by the SNB’s dovishness, remains higher above previous-resistance-turned-support at 1.0800. Therefore, traders may look to fade any short-term GDP-driven weakness, whereas a stronger-than-expected report could drive EURCHF back up toward 1.10.

Source: City Index

Source: City Index