A day before the European Central Bank decides on monetary policy, investors dumped the euro again this morning on fresh concerns over growth in the single currency block. Purchasing managers in the manufacturing sector reported deteriorating conditions in July, especially in Germany, where the sector contracted at its weakest pace in over 7 years. In France, too, activity stagnated while across the Eurozone purchasing managers in the sector reported the weakest levels of activity since December 2012. As a result, calls grew louder for the ECB to introduce more stimulus, with the probability of a 10 basis point cut in the deposit rate tomorrow rising to just under 50% from around 40% before. The euro extended its falls following yesterday’s sell-off, while the German DAX bounced off its lows after it had started on the back-foot following the big rally from the day before. The single currency may stage a short-covering bounce from oversold levels later, but heading into the ECB meeting the bias is clearly bearish. If the central bank turns out to be as dovish as we expect them to be then the euro could extend its declines across the board tomorrow. However, the dollar looks a bit overbought especially with the Fed likely to cut interest rates next week. So instead of the EUR/USD, euro bears may prefer looking at the euro crosses such as the EUR/GBP for trade ideas.

In case you missed it, here is a recap of the IHS Markit Flash Eurozone PMI data from earlier:

- German July flash manufacturing PMI 43.1 vs. 45.2 expected, down from 45.0 in June. Services PMI 55.4 va 55.3 and 55.8 last.

- France July flash manufacturing PMI 50.0 vs. 51.6 and 51.9 last. Services PMI 52.2 vs. 52.7 and 52.9 last.

- Eurozone July flash manufacturing PMI 46.4 vs. 47.6 expected and last. Services PMI 53.3 as expected but lower than 53.6 in June. Composite PMI 51.5 vs. 52.2 expected and last.

- “The pace of GDP growth looks set to weaken from the 0.2% rate indicated for the second quarter closer to 0.1% in the third quarter"

Meanwhile the pound, which refused to fall on the announcement of Boris Johnson becoming the new UK Prime Minister, was higher across the board at the time of writing. Clearly, short-side profit taking was supporting the beleaguered currency after sharp falls in the previous months.

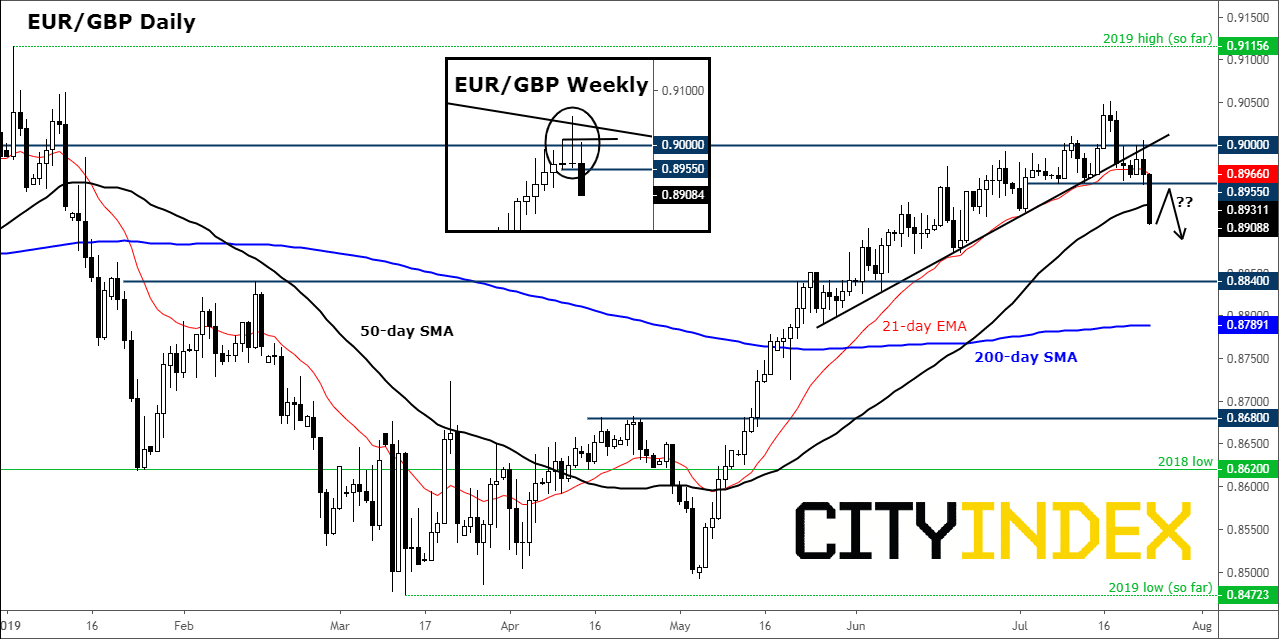

From a technical point of view, we continue to favour looking for bearish setups on the EUR/GBP after it posted a potential bearish reversal candle last week. We have now seen the breakdown of support around 0.8850/55, an area which could turn into resistance upon a retest later today or week.

Source: Trading View and City Index.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

Latest Forex articles

Yesterday 06:01 AM

April 17, 2024 02:40 PM

April 17, 2024 04:47 AM