March 5, 2020 4:13 PM

EUR/GBP Could Reach Near .9000

Earlier today, we asked the question: ‘When will Japan Act?” on providing additional stimulus in the face of the coronavirus plaguing the economy, with the Reserve Bank of Australia (RBA), the Bank of Canada (BOC) and US Federal Reserve (FED) already doing so. Currently, members of the Bank of Japan (BOJ) see no need to act, however if USD/JPY fell sharply through 105.00, members would take a look. The next BOJ meeting isn’t until March 18th.

If we look at the Bank if England (BOE), they are in the mist of handing over the reins, as new Bank of England Governor Andrew Bailey takes over for current Governor Mark Carney on March 16th. However, a week before then, on March 11th, the UK will present its 2020 Spring Budget. The BOE’s Monetary Policy Committee (MPC) doesn’t meet until March 26th. Yesterday, Bailey sad the BOE and the Treasury will work together to provide financial support to companies affected by the coronavirus. On January 20th, the BOE held rates at 0.75%. Expectations are for the MPC to cut rates by 25bps on March 26th. Could it come earlier? Of course, it can!

Let’s take a look at the other side of the recently divorced couple, the European Union (EU). The European Central Bank (ECB) currently has rates at -0.50%!! Their next meeting is March 12th, a day after the UK’s spring budget report. On Monday, ECB President Christine Lagarde said the ECB will act if needed to support the Euro Area as the coronavirus creates economic risks. The market is expecting -10bps at the March 12th meeting. But how much more can the ECB cut and what affect would it have? Italy plans to set aside over $8 Billion to help business who are dealing with the fallout of the coronavirus. More fiscal stimulus needs to be done.

With a potential cut on its way from the BOE of 25bps, and perhaps more as the BOC and the FED have done, one would expect the GBP to be moving lower. And with a cut of 10bps from the ECB next week, one would expect the Euro to be moving lower as well, all else being equal. However, due to the inequality of the cuts, one would expect GBP to be moving lower at a faster pace than the Euro. And that is precisely what is happening to EUR/GBP.

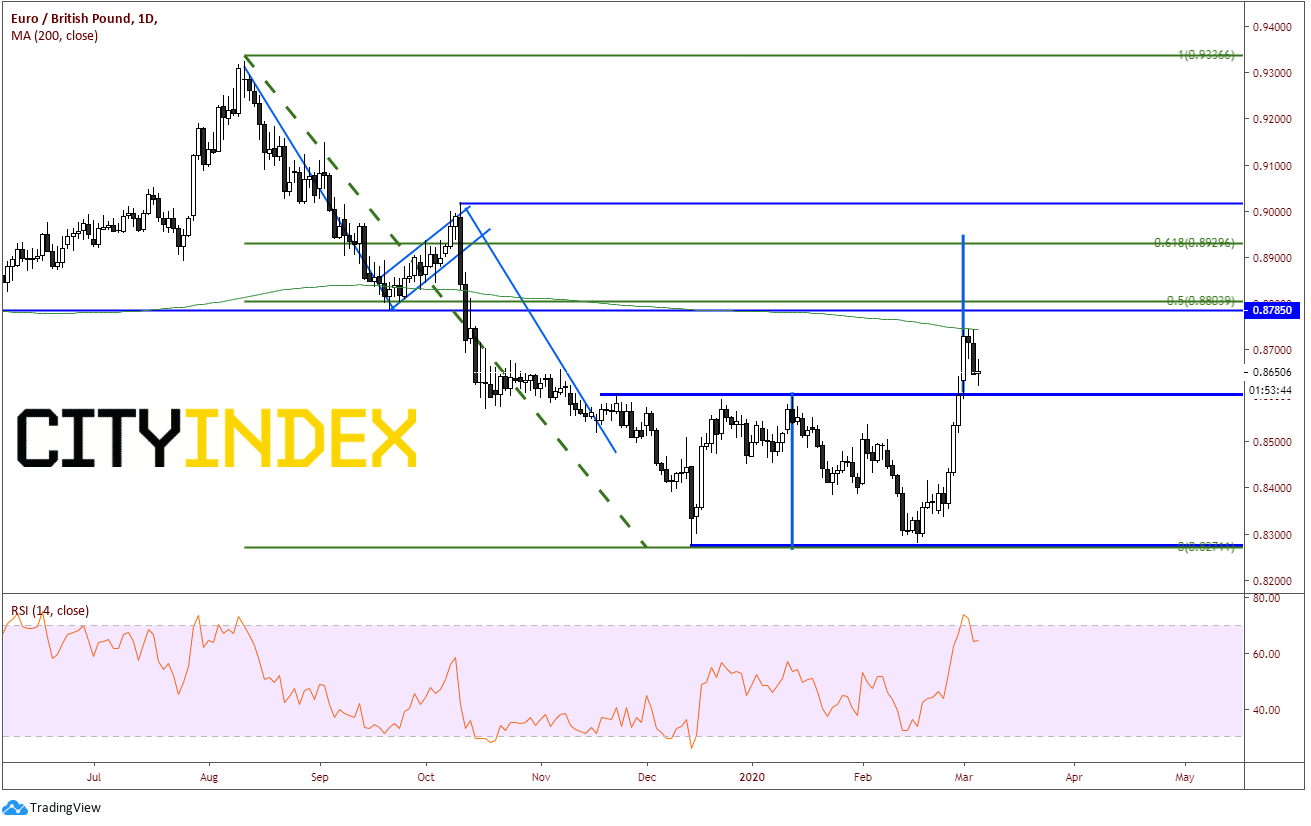

As we have discussed, when stock markets around the world began to sell off, the carry trade began to unwind. As a result, the Euro began moving higher. EUR/GBP put in a double bottom on a daily timeframe at .8270 and on February 28th, price broke higher through the neckline of the double bottom setting up a target of near .8950. The pair continued to trade higher and halted at the 200 Day Moving Average before pulling back to today’s lows near .8620. This gave a chance for the overbought RSI to unwind. Resistance is at the 200 Day Moving Average near .8680, horizontal resistance and the 50% retracement from the August 18th, 2019 highs to the February 18th lows, near .8900, and the 61.8% Fibonacci retracement level near the double bottom target at .8930/50.

Source: Tradingview, City Index

If the markets continue to believe that the BOE rate cut will have more of an effect than the ECB rate cut, EUR/GBP should remain bid. In addition, if the carry trade unwind continues, then EUR/GBP should remain bid. If the price action in EUR/GBP is going to change, one of these 2 situations will most likely have to change as well.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest EUR articles

April 13, 2024 08:00 PM

March 25, 2024 02:55 AM

January 22, 2024 04:19 AM

January 18, 2024 04:46 AM