EUR USD Will Draghi trigger short squeeze in euro

Growth in the Eurozone is picking up, unemployment is falling and inflation is accelerating towards the European Central Bank’s 2 per cent target. Within the […]

Growth in the Eurozone is picking up, unemployment is falling and inflation is accelerating towards the European Central Bank’s 2 per cent target. Within the […]

Growth in the Eurozone is picking up, unemployment is falling and inflation is accelerating towards the European Central Bank’s 2 per cent target. Within the Eurozone however, inflation is higher in some countries and lower in others. Spain’s 3% inflation rate stands out. But it is Germany where most of the noise is coming from. Here, inflation rose to 1.9% year-over-year in January from 1.7% the month before. With interest rates at zero and QE near full throttle, you can understand why the Germans feel that the ECB’s current monetary policy stance is no longer appropriate for the Eurozone’s economic powerhouse. Indeed, Germany’s finance minister Wolfgang Schäuble, has said the ECB’s monetary policy is too loose for Germany and the euro too low for his country.

But Mario Draghi and co are obviously responsible for the Eurozone as a whole, not individual countries, and would deflect criticism by pointing to the fact that by being in a currency union, a country effectively foregoes control over its monetary policy. This is the opportunity cost. The slower rate of growth and high levels of unemployment, particularly in the youth category, in some Eurozone countries – Italy, for example – is why the ECB has until now resisted calls from Germany to normalise its monetary policy. Meanwhile external pressure is growing on the ECB, too – for example, from the US government. Last week, President Trump’s trade adviser said that Germany is using a “grossly undervalued” euro to “exploit” the US and its EU partners.

As the pressure grows, Mario Drgahi will ultimately have to make a sacrifice. The ECB cannot let inflation accelerate uncontrollably, even if it means choking off economic growth for some. But are we at that stage yet for the ECB to make a sacrifice? If not exactly there, we are not that far off either.

Market participants will therefore be paying a lot of attention to what Mario Draghi will have to say with regards to the future path of monetary policy given the improvement in data recently. The ECB president’s testimony at the European Parliament’s Economic and Monetary Affairs committee will start at 14:00 GMT with a statement. After that he will be answering questions from legislators. Any suggestions of tapering QE early could send the euro surging higher.

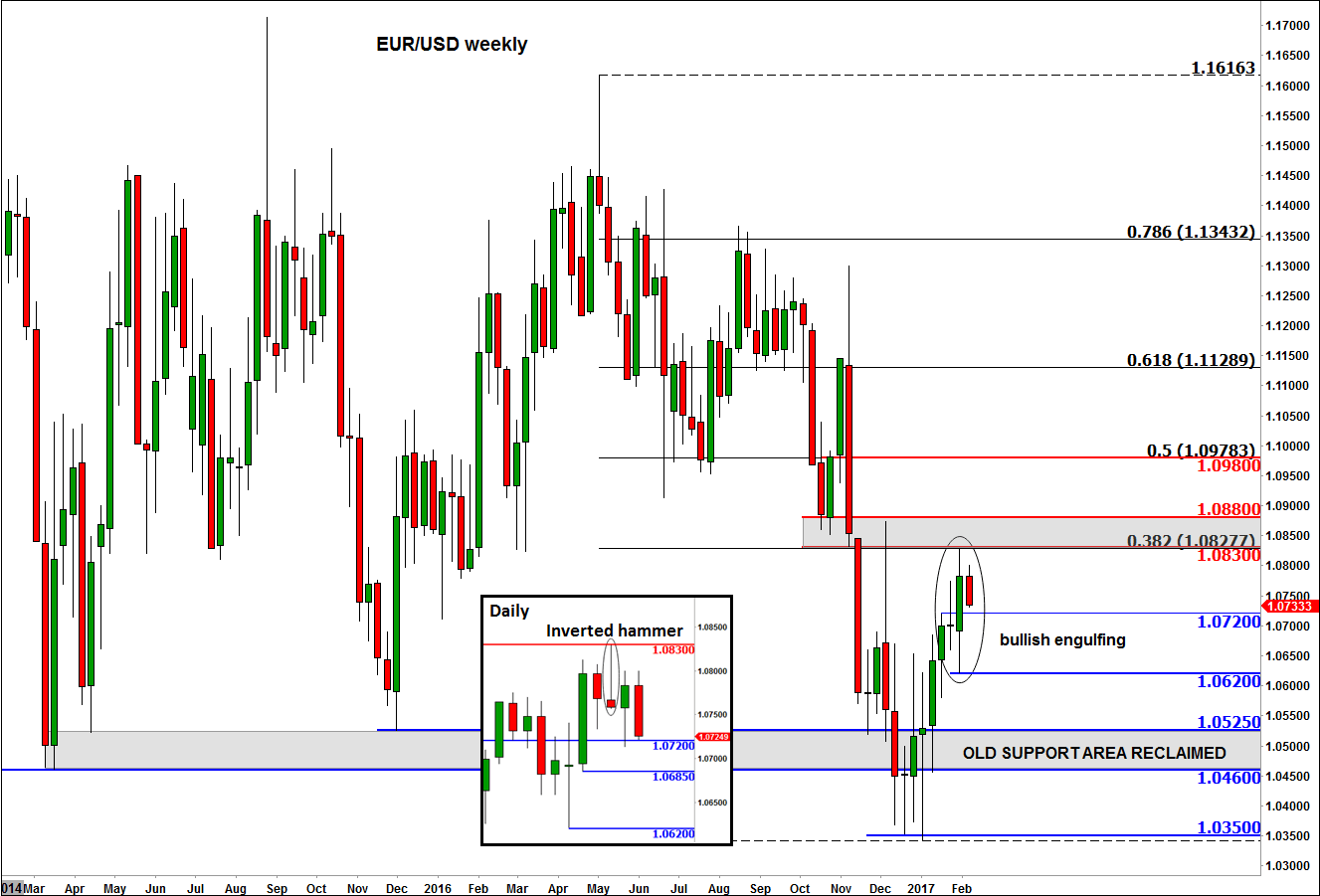

But as far as today’s session is concerned and at the time of this writing we haven’t seen any signs yet that the EUR/USD is bouncing back, though it may do so ahead of Draghi’s speech. That daily inverted hammer candle from Thursday (see the inset) off of the 1.0830 resistance level is still dominating the technical agenda for now. However on the main weekly chart one can observe a large bullish engulfing candle, which is obviously bullish. Thus the weakness at the start of this week may be short-lived. The slightly longer-term-focused bullish speculators could potentially step in after this morning’s retracement in anticipation of hearing hawkish or less dovish remarks from Mario Draghi. Technically, the area around 1.0710/20 is a key short-term support zone, where the EUR/USD was trading at the time of this writing. The outlook on the fibre remains moderately bullish unless last week’s low at 1.0620 breaks. Even so, the longer-term bearish outlook will only be fully re-instated if and when price moves back below the 1.0460/1.0525 long-term support area. Until and unless that happens, we are wary of a possible short-squeeze rally in the EUR/USD, perhaps towards 1.0980 or 1.1000 area.