EUR USD hits lowest since July as Yellen data point to Dec hike

The EUR/USD has fallen to its lowest level since July. Evidently, investors are continuing to favour the higher-yielding dollar over the euro amid the growing […]

The EUR/USD has fallen to its lowest level since July. Evidently, investors are continuing to favour the higher-yielding dollar over the euro amid the growing […]

The EUR/USD has fallen to its lowest level since July. Evidently, investors are continuing to favour the higher-yielding dollar over the euro amid the growing disparity between the European Central Bank and Federal Reserve’s monetary policies. Whereas the ECB is contemplating on increasing its monetary stimuli in December, the Fed is seriously considering a first rate increase in more than a decade in the same month. Today saw the dollar take another lurch higher, finding support from stronger-than-expected US economic data and hawkish comments from Janet Yellen that the downside risks to the US economy are diminishing and that a December rate increase remains a “live possibility.” A live possibility it may well be if last month’s employment report, due on Friday, shows solid gains in non-farm payrolls and wages. And judging by the latest jobs market data and the corresponding reaction of the financial markets, traders are certainly starting to price in this possibility.

Indeed, the closely-watched employment component of the US ISM Non-Manufacturing PMI for October rose nearly a whole point to 59.2, while the ADP private sector jobs reports showed a solid 182 thousand job gains in October. Today’s other US macro numbers were likewise better than had been anticipated with the ISM non-manufacturing PMI unexpectedly climbing 2.2 points to 59.1 from 56.9 and the US trade deficit narrowing sharply in September to $40.8 billion from $48.0 billion the month before. Earlier today, the latest services PMI data out of the Eurozone were mixed with downward revision in Germany offsetting gains in countries like Spain. As a result, the final Eurozone services PMI was revised a touch lower to 54.1 from 54.2 previously.

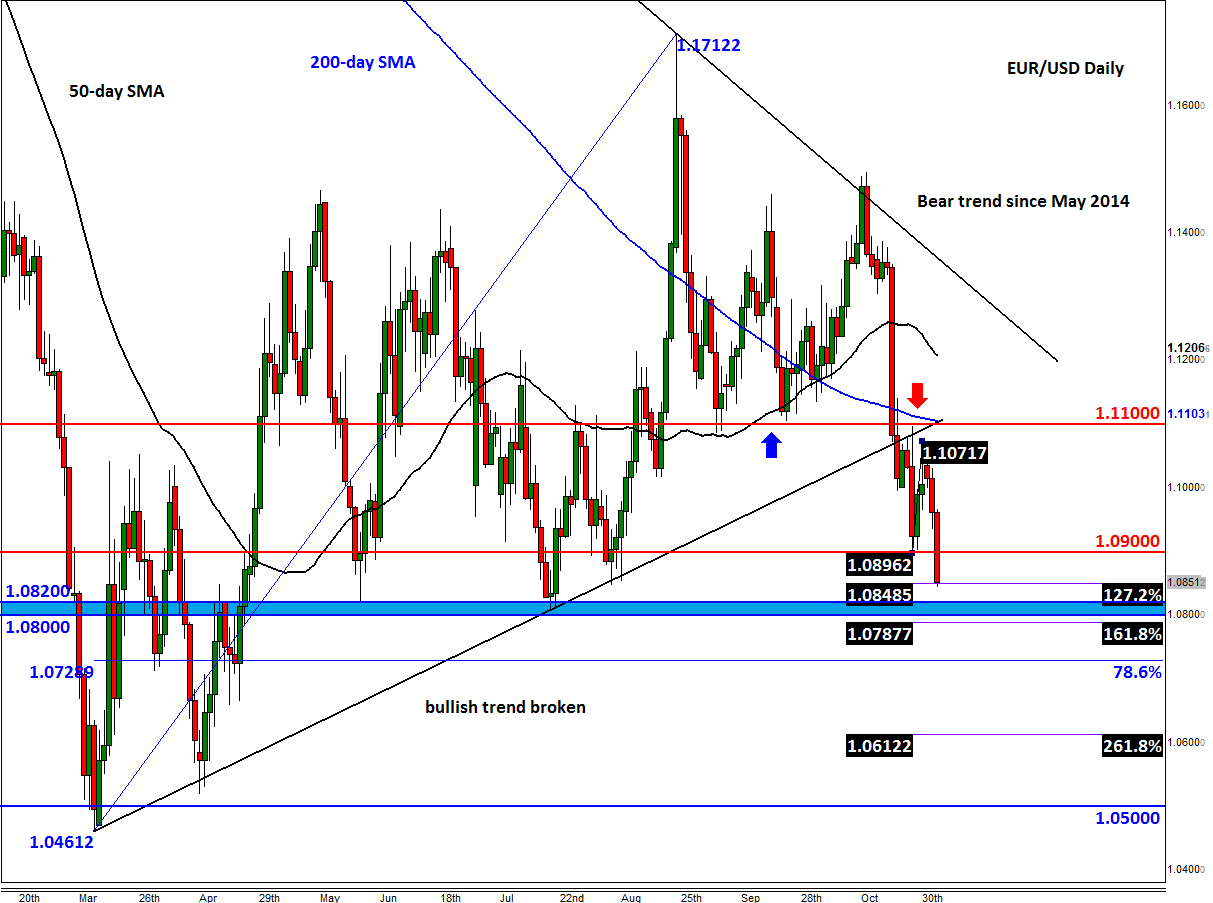

Following the release of stronger US data today, the yield on the US two-year Treasury note rose to its highest level since April 2011, while the fed funds futures implied a probability of 58% that the lift off will occur in December – an increase of 4 percentage points from the day before. Consequently, the EUR/USD has dropped to a low so far of 1.0845, its lowest level since July 21. The next key support for the world’s most heavily-traded FX pair comes in around 1.0800/20, which corresponds with the low hit in July. Below this level, there’s little further support seen until the 78.6% Fibonacci retracement at 1.0725/30, followed by the March low at 1.0460. For the euro to breach the March low and head towards parity, we will need to see continued hawkish talk from Fed and a significant improvement in US data, starting with the jobs report on Friday. Meanwhile some short-term resistance levels to watch include 1.0900, the previous support, followed by 1.1000 and then 1.1100. The bulls would do very well to push rates back towards 1.1100, let alone break above it. But they may get a helping hand from a disappointing US jobs report on Friday. But for now at least, the path of least resistance is clearly to the downside.