EUR USD could plunge if ECB denies taper talk

According to a CNN poll, Hillary Clinton won last night’s debate with Donald Trump, ensuring a 3-0 aggregate score. Market participants seem to be convinced […]

According to a CNN poll, Hillary Clinton won last night’s debate with Donald Trump, ensuring a 3-0 aggregate score. Market participants seem to be convinced […]

According to a CNN poll, Hillary Clinton won last night’s debate with Donald Trump, ensuring a 3-0 aggregate score. Market participants seem to be convinced that Clinton will now become the next US President and as such they are not foreseeing any major economic or political shocks that would discourage the Fed to raise rates in December or threaten its independence. At the same time though, the Brexit experience in the UK goes to show that opinion polls are just that and they are not always accurate in predicting the actual outcome of political events. Consequently, traders are holding back from opening bold positions in the dollar ahead of the US presidential election and the upcoming Fed meetings. It should also be noted that a Clinton win does not necessarily mean the dollar would go higher, as the markets are by nature forward-looking.

Nevertheless, the USD/JPY is trading a touch higher today, the EUR/USD has slipped to its weakest level since July 27 and equity markets are holding up well too even if earnings from eBay missed the mark overnight. Generally speaking though, US earnings have been rather good so far which is why the S&P 500 is still holding near its record high, even if technically the benchmark stock index looks a little bit heavy which points to a potential correction of some sort.

Today’s focus will be on the European Central Bank and more so on ECB President Mario Draghi’s press conference at 13:30 BST (08:30 ET). Specifically, the market will be keen to find out what the ECB will do when the bond purchases programme ends next year and if they have thought about tapering the programme prematurely. If the Mr Draghi denies the taper rumour then that should, in theory, apply further downward pressure on the euro, while a confirmation of the talk could be euro-positive. Though not many people are expecting it, any suggestions that the ECB is thinking about extending the QE programme beyond March would almost certainly cause the euro to slump and lead to a rally in the stock markets.

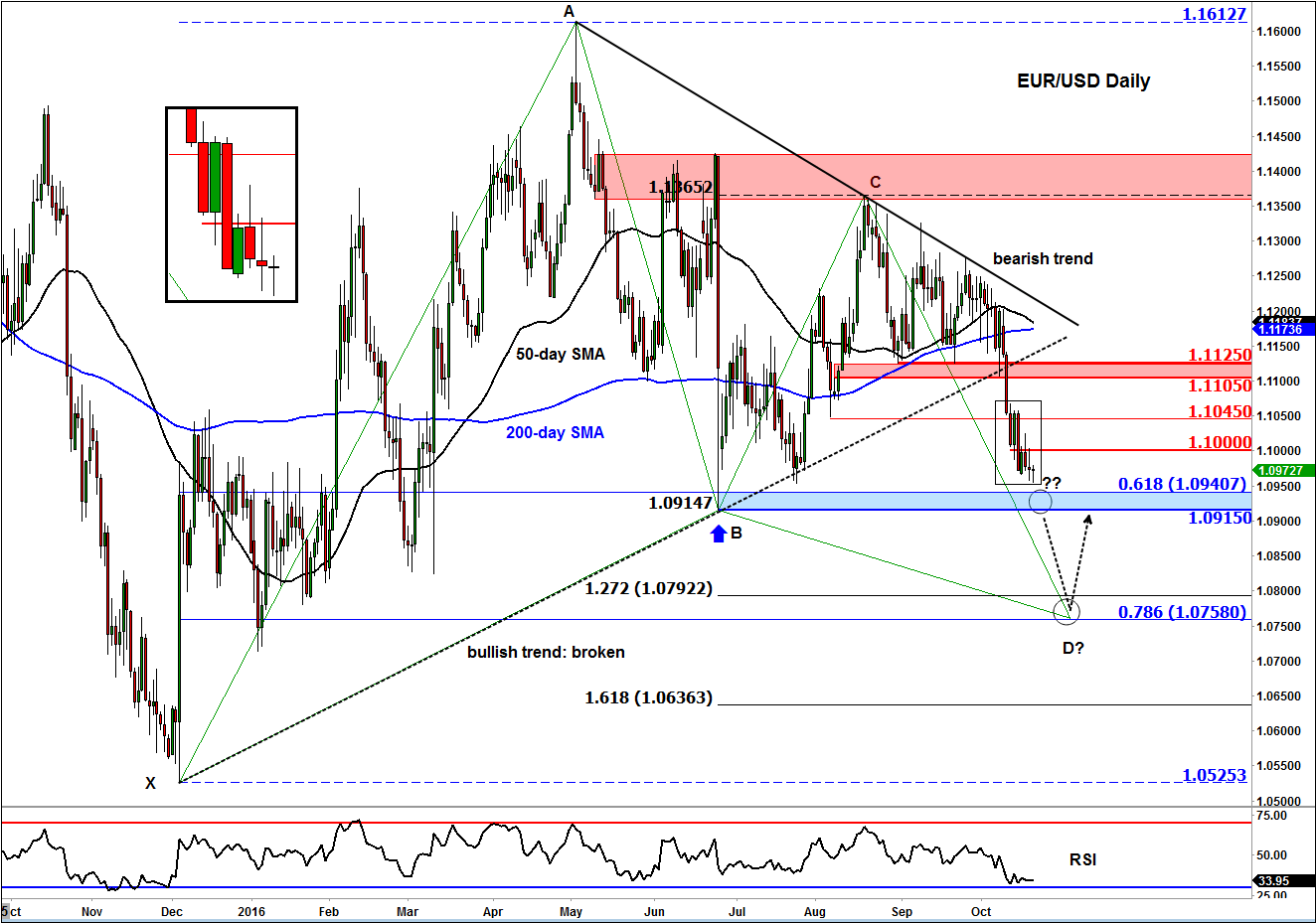

Ahead of the ECB meeting and presser, the EUR/USD had managed to bounce off its lowest level since Jul 27 but was still holding below the key 1.10 handle. The Fibre has been trending lower in recent days after its laborious consolidation phase during most of the summer. As a result, several support levels have broken down including the 50- and 200-day moving averages, the bullish trend line and the key 1.1105-1.1125 range. While this 1.1105-1.1125 range holds as resistance, the path of least resistance would remain to the downside, even if we do see a sharp rebound in the coming days. The next area of support to watch is around 1.0915-10940 where the low from June meets the 61.8% Fibonacci retracement of the last significant upswing. Given the slow and steady move lower, a potential drop to this area will more likely lead to a breakdown rather than a meaningful bounce. If so, the breakdown of support here will potentially pave the way towards the next bearish objective of 1.0755-1.0790 which is where the 78.6% Fibonacci retracement level convergences with the 127.2% extension of the corrective up move since June. Meanwhile some of the short-term resistance levels to watch include 1.1000, 1.1045 and that 1.1105-25 range as mentioned above.