The Bank of Japan and European Central Bank are both scheduled to announce their latest monetary policy decisions this week – on Tuesday and Thursday, respectively. EUR/JPY will therefore be a logical focus of currency markets this week just as global central bankers, finance ministers, top government officials and business leaders will meet in Davos, Switzerland for the highly anticipated World Economic Forum.

Up first will be the Bank of Japan, which issues its interest rate decision, monetary policy statement, and press conference on Tuesday in Japan. Though there are no expectations of any substantive changes to BoJ monetary policy or longstanding negative interest rates, markets will be watching closely for any signs that the central bank may be looking to wind down its massive stimulus program at some point in the foreseeable future. Recently, the BoJ unexpectedly reduced its purchases of Japanese government bonds, which provided a sharp boost for the Japanese yen on speculation that the central bank may be leaning towards tighter monetary policy. Any further indication on Tuesday of future stimulus reduction or an otherwise more hawkish Bank of Japan could result in another boost for the yen. In contrast, any lack of such indications would likely continue to weigh on the yen.

Thursday will feature the monetary policy decision from the European Central Bank. As with the Bank of Japan, markets will also be focusing on how the central bank may frame its path towards ending stimulus with respect to winding down its asset purchases. The euro has recently extended its persistent strength, both on a weaker US dollar as well as continuing strength in European economic growth. The ECB recently released its monetary policy meeting accounts from its last meeting in December. The minutes were seen as hawkish, as ECB officials hinted that tighter monetary policy, which includes the possibility of higher interest rates as well as the winding down of asset purchases, could be on the horizon amid an optimistic growth outlook for the euro zone. While inflation in the euro zone still remains below target, any hawkish signals on Tuesday that may indicate steps towards policy tightening could give the euro a further boost.

Over the past weekend, the German Social Democrats (SPD) voted to enter into coalition talks with Angela Merkel’s Christian Democratic Union (CDU) party. Prior to Sunday’s vote, there had been significant concerns that an opposite outcome would potentially cause chaos and crisis in Germany and throughout Europe, which would likely weigh heavily on the euro. For now, that bullet has been dodged, paving the path for potentially more gains for the shared currency.

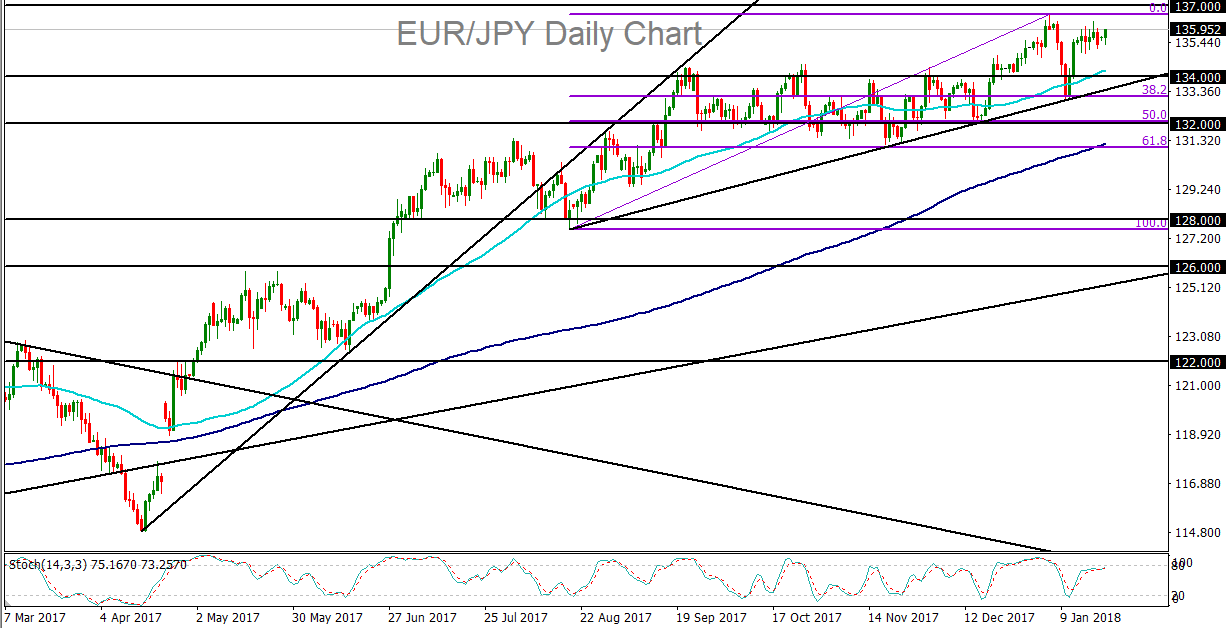

From a technical perspective, EUR/JPY continues to trade within a well-established uptrend, as longstanding euro strength and resilience have remained in sharp contrast against a persistently lagging Japanese yen. Early in the month (and the new year), the currency pair reached more than a two-year high at 136.62 before pulling back. As of Monday, EUR/JPY continues to re-approach those highs. On any further boost for the currency pair amid this week’s central bank decisions, a breakout to new highs would confirm a continuation of the bullish trend, with the next major upside target around the 139.00 level. Any failure to break to new highs could pressure the currency back down towards the 134.00 support area.

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Euro articles

April 2, 2024 03:02 PM

February 15, 2024 07:29 PM

January 4, 2024 07:14 PM

December 20, 2023 07:17 PM