EUR GBP policy divergence in focus again amid contrasting UK EZ data

Contrasting data from the UK and Eurozone has caused the EUR/GBP to turn sharply lower and the cross now appears to be on the verge […]

Contrasting data from the UK and Eurozone has caused the EUR/GBP to turn sharply lower and the cross now appears to be on the verge […]

Contrasting data from the UK and Eurozone has caused the EUR/GBP to turn sharply lower and the cross now appears to be on the verge of a much larger sell-off as the focus returns to the growing disparity of monetary policy between the ECB and the BoE. According to the Office for National Statistics (ONS), the 3-month moving average of UK Average Earnings Index (which includes bonuses) rose to 2.9% in July compared to the same period a year earlier, up from a revised +2.6% reading the month prior. This was also much better than expected (+2.5%) and represents the best reading in six years. UK employment was up by a good 42,000, significantly above the 18,000 expected. As a result, the rate of unemployment unexpectedly fell to 5.5% from 5.6% previously. The only disappointing aspect of today’s employment data was that jobless claims rose unexpectedly by 1,200 in August when a drop of 5,100 was expected. Nevertheless, FX traders chose to focus on the brighter side of the report and as a result decided to buy the pound against all major currencies.

The cheerful UK jobs data comes on the back of a string of disappointing macro numbers of late and removes some concerns about the health of the UK economy. With earnings growth now accelerating, it is only a matter of time before consumer price inflation responds. In other words, we are getting closer to a rate hike from the Bank of England which could possibly happen in the first quarter of 2016.

In contrast, the European Central Bank may have to wait for a longer period of time before trimming or ending QE, let alone talk about rate rises. That’s because inflation in the Eurozone is virtually non-existent at the moment. This morning, for example, Eurostat reported the final estimate for the change in the price of goods and services purchased by consumers in August. The data showed an unexpected slowdown in inflation, with the headline CPI dropping to 0.1% from 0.2% and core CPI to 0.9% from 1.0% on a year-over-year basis in August.

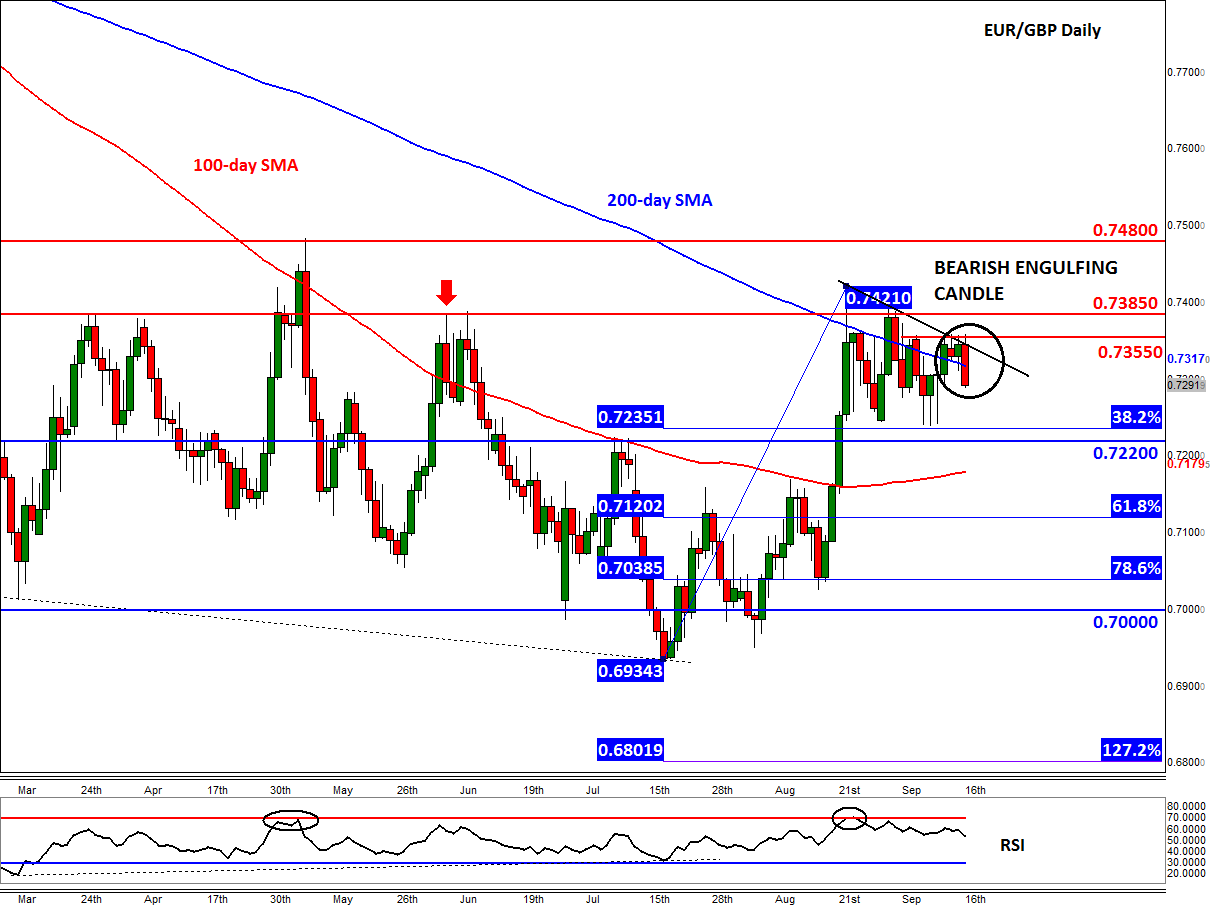

Because of the stronger UK jobs data and the surprisingly weak inflation figures from the Eurozone, the EUR/GBP has been a big mover today. At the time of this writing, the cross is showing a large bearish engulfing candle on its daily chart, suggesting that the sellers have now taken over once more. The bears have caused the EUR/GBP to break back below the 200-day moving average around 0.7315, which incidentally has occurred around the same time as the bulls have managed to hold their own above this moving average on the GBP/USD pair.

Consequently, as things stand, it looks like the next leg lower may have started for the EUR/GBP. The bears may now be targeting at least the 38.2% Fibonacci level of the most recent upswing at 0.7235, with further support seen slightly lower at 0.7220 (previously resistance). But should the EUR/GBP break below here then the next bearish targets could be the 100-day moving average at 0.7180 or the 61.8% Fibonacci level at 0.7120. Below 0.7120, there are not many more technically-important levels until that psychological 0.7000 handle. Meanwhile this bearish outlook would become invalid if price climbs back above the 0.7355/85 resistance range. If this happens, we should then expect to see some further follow-up technical buying towards the next key resistance at 0.7480.