EUR AUD A Terrible Horrible No Good Very Bad Day

The popular children’s book “Alexander and the Terrible, Horrible, No Good, Very Bad Day” describes the travails of a child named Alexander who endures gum […]

The popular children’s book “Alexander and the Terrible, Horrible, No Good, Very Bad Day” describes the travails of a child named Alexander who endures gum […]

The popular children’s book “Alexander and the Terrible, Horrible, No Good, Very Bad Day” describes the travails of a child named Alexander who endures gum in his hair, sitting in the middle of the back seat, no dessert at lunch, and eating lima beans, among other slights.

After this morning’s economic data euro bulls are starting to feel a bit like Alexander. Every hour from 6:00 – 9:00 GMT brought another disappointing economic report for the Eurozone, prompting traders to increase bets that the European Central Bank (ECB) will have to expand its Quantitative Easing (QE) program:

6:00 GMT: German Retail Sales (Aug)

Retail sales, a critical measure of the health of the consumer, fell by 0.4% m/m in Europe’s largest economy. This figure was notably lower than both the 0.2% rise expected and the revised 1.6% growth in July. That said, this report tends to be volatile on a month-by-month basis, so traders generally took the data in stride.

6:45 GMT: French Consumer Spending (Aug)

Just 45 minutes later, a similar report from France, the Eurozone’s second-largest economy, showed the same lackluster consumer last month. French consumer spending was flat in August, missing expectations of a 0.4% rise. This marked the lowest reading for the report in five months.

7:55 GMT: German Employment Report (Aug)

Unfortunately for euro bulls, the hits just kept coming. A little over an hour later, we learned that unemployment in Germany rose by 2k citizens in August, above the expectations of a 5k decline. Astute traders will note this report also precedes the recent struggles at Volkswagon, one of Germany’s largest employers, so more layoffs could be coming down the pipeline in the next few months.

9:00 GMT: Eurozone CPI (Sept) and Unemployment (Aug)

For traders who pinned their hopes on today’s two most important economic reports out of the Eurozone, things went from bad to worse. The flash estimate of the consumer price index (CPI) report showed a 0.1% m/m decline in inflation (i.e. deflation) in September, while the August report was also revised lower to show just a 0.1% increase in prices. Meanwhile, last month’s Eurozone unemployment rate came in at 11.0%, above the 10.9% rate expected.

In aggregate, these reports show that the Eurozone economy is rolling over after signs of optimism around the middle of the year. As we noted above, continued weak economic data could force the ECB to expand or extend its QE program in the months to come. This possibility could act as a long-term anchor on the value of the euro.

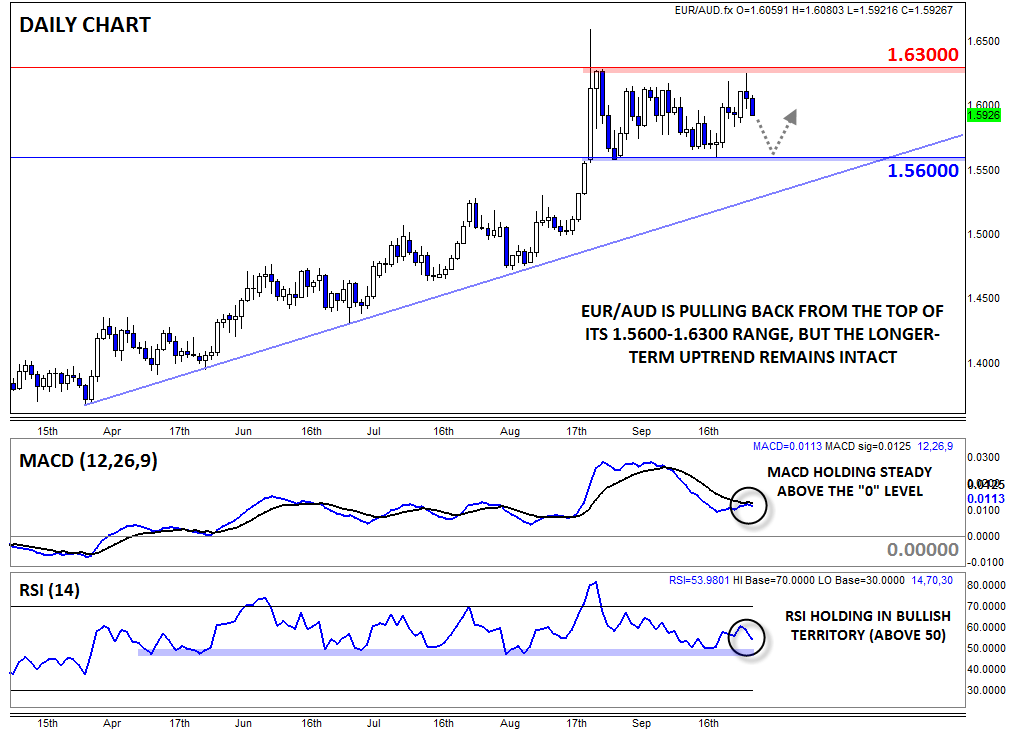

Technical View: EUR/AUD

Today’s unanimously euro-negative data has taken a toll on EUR/AUD, which is retreating back below the 1.60 level as of writing. That said, the pair remains essentially in the middle of its five-week consolidation range from 1.5600 to 1.6300. In the short-term, more weakness toward the bottom of the range around 1.5600 is possible, but the medium-term outlook is far more constructive.

To wit, the pair appears to be correcting through time, rather than through price, back to its five-month bullish trend line. Meanwhile, both the MACD and RSI indicators remain in bullish territory, suggesting that no significant long-term damage has been done. For now, traders may prefer to play the established range by looking to fade drops down toward 1.5600 or rallies up to 1.6300 until the key trend line can catch up with price.

Source: City Index

Source: City Index