The contrast between European and US equities could not be more striking. Whereas the S&P 500 is just shy of its all-time high, in Europe, most major stock indices are still limping following their early 2016 wobble. This is despite the ECB’s on-going bond buying programme is at full throttle, which has helped to push benchmark government bond yields to record lows with the German 10-year being just above zero and UK’s equivalent dropping to a fresh low today.

Falling yields or rising bond prices is “supposed” to encourage yield-seeking investors into investing in riskier assets such as equities, especially when you consider the fact that the ECB, as part of its QE stimulus programme, is purchasing corporate bonds as well (as government debt). Yet, the European markets are struggling to keep up with their US counterparts, which is even more bizarre given that another interest rate rise there looks almost inevitable in the coming months (which in theory should be bad news for US equities).

Additionally, the surging prices of crude oil have likewise failed to underpin the European indices in a meaningful way thus far. Clearly then, investors here must be holding fire either because of domestic growth fears or concerns about the potential implications of Britain leaving the EU. If the latter is the case, then a vote to stay in the EU, if seen, should lead to a big rally for European markets.

Thus, until the June 23 referendum is out of the way, the European indices will most likely remain out of favour or range-bound, or at best continue to underperform the US markets. Thereafter, if Britain is still part of the EU, they should begin to outperform given the growing divergence between monetary policies in Europe and the US.

Technical outlook: DAX buying pressure building up?

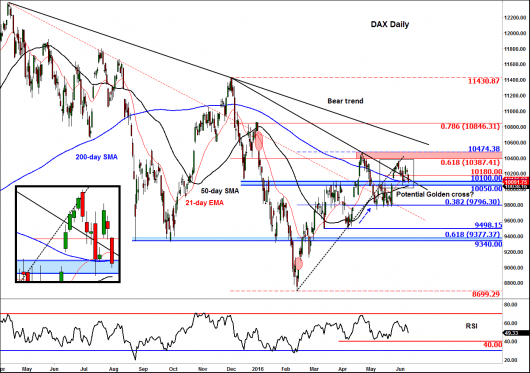

That being said, the underlying technical trend remains somewhat bullish for the likes of the DAX, which means weaknesses, like this morning’s performance, could be faded. As can be seen from the chart, below, the German index recently found good support around the 38.2% Fibonacci retracement level of the rally from this year’s earlier lows, at just below 9800. The shallow pullback and lengthy consolidation prior to the bounce suggests bullish pressure may be building up beneath the surface.

The index is once again consolidating in a relatively tight range around the previous resistance area of 10050-10100, where the 50- and 200-day moving averages also come into play. The 50-day MA has been trending higher of late and looks set to move above the 200 to create a so-called “golden crossover,” which is a prerequisite for some bullish momentum traders. Thus the crossover, if seen, could see this group of market participants come into the market and help fuel a potential rally.

If the bulls are successful at defending the above support levels, they will still need to chop some wood. Short-term resistances that will then need to be cleared include 10180; the range between 10390 and 10475, and the bearish trend line.

However, if support at 10050 breaks down first then we may see a more noticeable correction before a potential bounce. And needless to say, if the UK public decide to vote in favour of an exit from the EU (Brexit) then it is anyone’s guess how far the markets could drop in the short term, regardless of fundamentals at the time.