EU indices up this morning | TA focus on Hennes & Mauritz

INDICES

Yesterday, European stocks were broadly higher. The Stoxx Europe 600 Index climbed 0.7%, Germany's DAX 30 rose 0.7%, France's CAC 40 jumped 1.0%, and the U.K.'s FTSE 100 was up 0.4%.

EUROPE ADVANCE/DECLINE

69% of STOXX 600 constituents traded higher yesterday.

34% of the shares trade above their 20D MA vs 29% Wednesday (below the 20D moving average).

41% of the shares trade above their 200D MA vs 39% Wednesday (below the 20D moving average).

The Euro Stoxx 50 Volatility index eased 2.12pts to 34.68, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: none

3mths relative low: none

Europe Best 3 sectors

financial services, automobiles & parts, banks

Europe worst 3 sectors

travel & leisure, real estate, media

INTEREST RATE

The 10yr Bund yield fell 3bps to -0.44% (below its 20D MA). The 2yr-10yr yield spread rose 1bp to -22bps (above its 20D MA).

ECONOMIC DATA

FR 07:45: Jun Consumer Confidence, exp.: 93

EC 09:00: May Loans to Households YoY, exp.: 3%

EC 09:00: May M3 Money Supply YoY, exp.: 8.3%

EC 09:00: May Loans to Companies YoY, exp.: 6.6%

UK 09:00: May Car Production YoY, exp.: -99.7%

MORNING TRADING

In Asian trading hours, EUR/USD was flat at 1.1220 while GBP/USD slipped to 1.2418. USD/JPY held gains at 107.19. This morning, official data showed that Japan's Tokyo CPI grew 0.3% on year in June (as expected).

Spot gold edged down to $1,761 an ounce.

#UK - IRELAND#

Aston Martin, a luxury sports cars manufacturer, released a trading statement: "Dealer stock had reduced by 617 units year-to-date to end May. (...) As expected, due to COVID-19 disruption, retail sales (dealer sales to customers) and wholesales are expected to be lower in Q2 than in Q1. (...) More than 90% of dealer network now open. (...) For the full year total wholesales are currently expected to be broadly evenly balanced between sports cars and DBX."

Weir Group, an engineering company, published a trading update: "Refinancing of US$950m RCF and £200m Term Loan, extending maturities to 2023 and 2022 respectively. (...) Minerals orders stable sequentially in Q2 to date despite Covid-19 restrictions. (...) Oil & Gas still expected to be cash generative for the full year; continuing to explore exit options."

Bunzl, a distribution and outsourcing company, was upgraded to "overweight" from "neutral" at JPMorgan.

Rentokil Initial, a business services group, was upgraded to "overweight" from "neutral" at JPMorgan.

#GERMANY#

Deutsche Lufthansa, an airline group, reported that its shareholders voted in favor of accepting the 9 billion euros bailout plan from the German government, who will establish a 20% stake in the company.

#FRANCE#

Air France-KLM's, an airline company, 3.4 billion euros aid package was approved by the French and Dutch governments, reported Reuters citing people familiar with the matter.

#SPAIN - PORTUGAL#

Iberdrola, a Spanish energy group, was downgraded to "hold" from "buy" at HSBC.

EDP, a Portuguese electric utilities company, was downgraded to "hold" from "buy" at HSBC.

#ITALY#

Enel, an energy company, was downgraded to "hold" from "buy" at HSBC.

#SWITZERLAND#

Novartis, a pharmaceutical group, announced that it has agreed to pay the U.S. regulators 347 million dollars to settle all Foreign Corrupt Practices Act investigations into its bribery law violation.

#SCANDINAVIA#

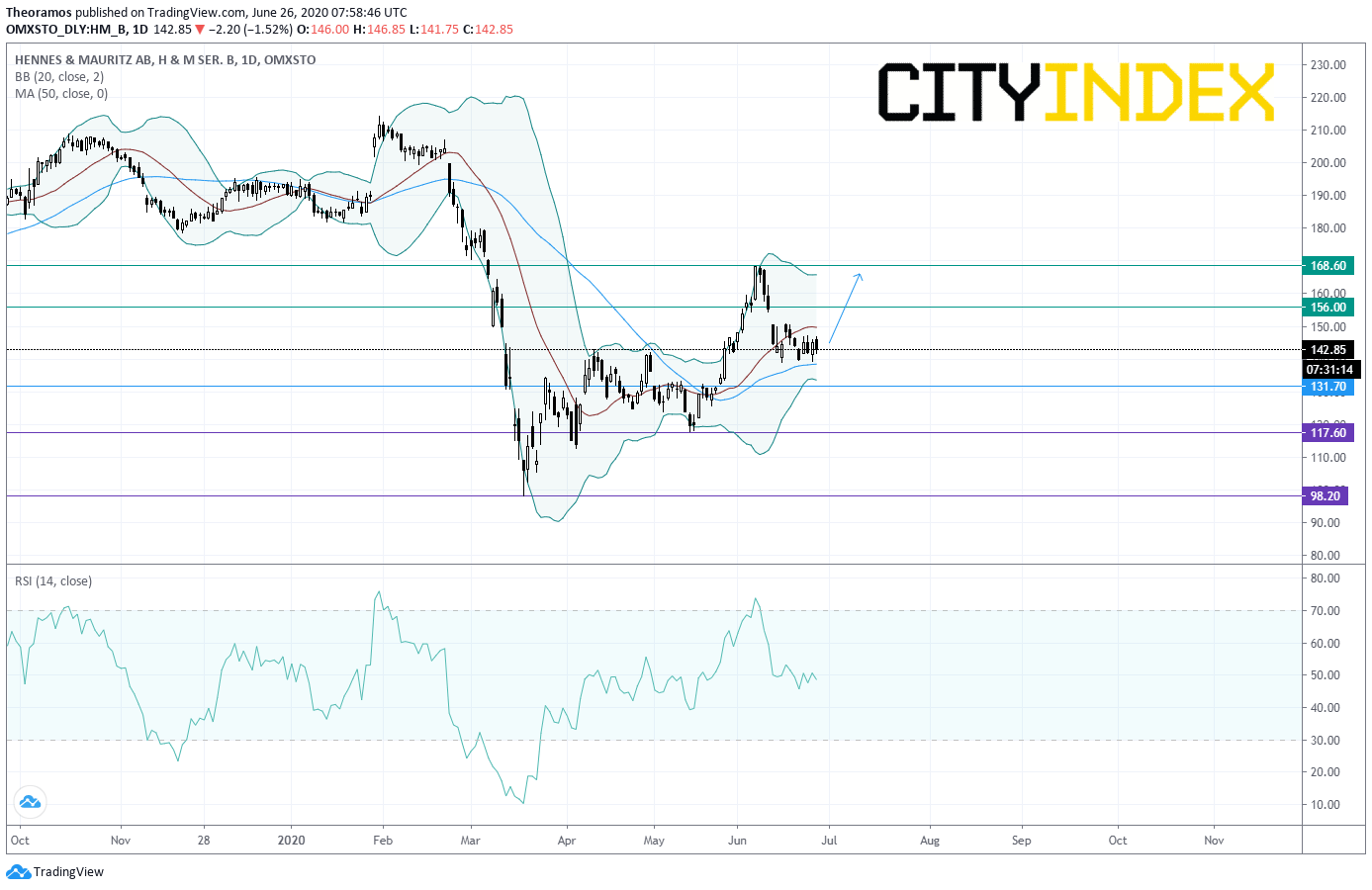

Hennes & Mauritz, a swedish clothing-retail company, posted second quarter earnings in line with estimates. The company expects 2020 net decrease of stores. From a chartist point of view, the share consolidates above the support at 131.7 swedish krona and remains on the upside since March. It is supported by its rising 50-period moving average (in blue). Above 131.7, the share aims 168.6 and 179.8 krona.

Source: GAIN Capital, TradingView

Yesterday, European stocks were broadly higher. The Stoxx Europe 600 Index climbed 0.7%, Germany's DAX 30 rose 0.7%, France's CAC 40 jumped 1.0%, and the U.K.'s FTSE 100 was up 0.4%.

EUROPE ADVANCE/DECLINE

69% of STOXX 600 constituents traded higher yesterday.

34% of the shares trade above their 20D MA vs 29% Wednesday (below the 20D moving average).

41% of the shares trade above their 200D MA vs 39% Wednesday (below the 20D moving average).

The Euro Stoxx 50 Volatility index eased 2.12pts to 34.68, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: none

3mths relative low: none

Europe Best 3 sectors

financial services, automobiles & parts, banks

Europe worst 3 sectors

travel & leisure, real estate, media

INTEREST RATE

The 10yr Bund yield fell 3bps to -0.44% (below its 20D MA). The 2yr-10yr yield spread rose 1bp to -22bps (above its 20D MA).

ECONOMIC DATA

FR 07:45: Jun Consumer Confidence, exp.: 93

EC 09:00: May Loans to Households YoY, exp.: 3%

EC 09:00: May M3 Money Supply YoY, exp.: 8.3%

EC 09:00: May Loans to Companies YoY, exp.: 6.6%

UK 09:00: May Car Production YoY, exp.: -99.7%

MORNING TRADING

In Asian trading hours, EUR/USD was flat at 1.1220 while GBP/USD slipped to 1.2418. USD/JPY held gains at 107.19. This morning, official data showed that Japan's Tokyo CPI grew 0.3% on year in June (as expected).

Spot gold edged down to $1,761 an ounce.

#UK - IRELAND#

Aston Martin, a luxury sports cars manufacturer, released a trading statement: "Dealer stock had reduced by 617 units year-to-date to end May. (...) As expected, due to COVID-19 disruption, retail sales (dealer sales to customers) and wholesales are expected to be lower in Q2 than in Q1. (...) More than 90% of dealer network now open. (...) For the full year total wholesales are currently expected to be broadly evenly balanced between sports cars and DBX."

Weir Group, an engineering company, published a trading update: "Refinancing of US$950m RCF and £200m Term Loan, extending maturities to 2023 and 2022 respectively. (...) Minerals orders stable sequentially in Q2 to date despite Covid-19 restrictions. (...) Oil & Gas still expected to be cash generative for the full year; continuing to explore exit options."

Bunzl, a distribution and outsourcing company, was upgraded to "overweight" from "neutral" at JPMorgan.

Rentokil Initial, a business services group, was upgraded to "overweight" from "neutral" at JPMorgan.

#GERMANY#

Deutsche Lufthansa, an airline group, reported that its shareholders voted in favor of accepting the 9 billion euros bailout plan from the German government, who will establish a 20% stake in the company.

#FRANCE#

Air France-KLM's, an airline company, 3.4 billion euros aid package was approved by the French and Dutch governments, reported Reuters citing people familiar with the matter.

#SPAIN - PORTUGAL#

Iberdrola, a Spanish energy group, was downgraded to "hold" from "buy" at HSBC.

EDP, a Portuguese electric utilities company, was downgraded to "hold" from "buy" at HSBC.

#ITALY#

Enel, an energy company, was downgraded to "hold" from "buy" at HSBC.

#SWITZERLAND#

Novartis, a pharmaceutical group, announced that it has agreed to pay the U.S. regulators 347 million dollars to settle all Foreign Corrupt Practices Act investigations into its bribery law violation.

#SCANDINAVIA#

Hennes & Mauritz, a swedish clothing-retail company, posted second quarter earnings in line with estimates. The company expects 2020 net decrease of stores. From a chartist point of view, the share consolidates above the support at 131.7 swedish krona and remains on the upside since March. It is supported by its rising 50-period moving average (in blue). Above 131.7, the share aims 168.6 and 179.8 krona.

Source: GAIN Capital, TradingView

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Commodities articles

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM

April 14, 2024 11:37 PM