EU indices up this morning | TA focus on EssilorLuxottica

INDICES

Yesterday, European stocks got heavier, with the Stoxx Europe 600 Index slumping 2.7%. Germany's DAX 30 tumbled 3.6%, France's CAC 40 plunged 4.2%, and the U.K.'s FTSE 100 edged down a little 0.2%.

EUROPE ADVANCE/DECLINE

87% of STOXX 600 constituents traded lower or unchanged yesterday.

55% of the shares trade above their 20D MA vs 74% Friday (below the 20D moving average).

20% of the shares trade above their 200D MA vs 20% Friday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 4.41pts to 38.32, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: none

3mths relative low: none

Europe Best 3 sectors

health care, retail, telecommunications

Europe worst 3 sectors

energy, banks, automobiles & parts

INTEREST RATE

The 10yr Bund yield was unchanged to -0.59% (below its 20D MA). The 2yr-10yr yield spread fell 1bp to -19bps (above its 20D MA).

ECONOMIC DATA

FR 07:45: Mar Budget Balance, exp.: E-35.2B

UK 09:00: Apr New Car Sales YoY, exp.: -44.4%

UK 09:30: Apr Markit/CIPS UK Services PMI final, exp.: 34.5

UK 09:30: Apr Markit/CIPS Composite PMI final, exp.: 36

EC 10:00: Mar PPI MoM, exp.: -0.6%

EC 10:00: Mar PPI YoY, exp.: -1.3%

MORNING TRADING

In Asian trading hours, EUR/USD held above the 1.0900 level while GBP/USD bounced slight to 1.2468. USD/JPY remained subdued at 106.58. AUD/USD climbed further to 0.6452 ahead of the Reserve Bank of Australia's rates decision.

Spot gold fell to $1,697 an ounce.

#UK - IRELAND#

Wizz Air, a low-cost airline company, reported that passengers capacity slumped 97.1% on year to 104,956 in April and the load factor dropped 17.3 percentage points to 74.7%.

Royal Mail, a postal service provider, was downgraded to "hold" from "sell" at Deutsche Bank.

#GERMANY#

Infineon Technologies, a semiconductor manufacturer, reported that 2Q net income dropped 15.2% on year to 178 million euros on revenue of 1.99 billion euros, up 3.7%. The company sees full-year revenue of "around E7.6 billion excluding Cypress and around E8.4 billion including Cypress, plus or minus 5 percent", citing a significantly weaker 2H outlook due to the coronavirus crisis.

SAP, a multinational software developer, said it "has identified that some of its cloud products do not meet one or several contractually agreed or statutory IT security standards at present", though "it does not believe that any customer data has been compromised as a result of these issues". The company added that it has initiated remediation of the identified areas of shortcoming, while the related expenses are expected to be covered within the range of its current financial outlook. Meanwhile, the company reported that it has agreed to sell its Digital Interconnect group to Sinch for 225 million euros.

Beiersdorf, a personal-care products manufacturer, posted 1Q revenue fell 1.9% on year (-3.6% organic growth) to 1.91 billion euros. The company said it has withdrawn its 2020 guidance issued on March 3, due to the coronavirus crisis.

Vonovia, a real estate group, announced that 1Q funds from operations increased 10.5% to 336 million euros and adjusted EDBITA grew 6.1% to 456 million euros on rental income of 564 million euros, up 12.3%. Regarding full-year outlook, the company stated: "We assume that the coronavirus will have only a limited impact on all business segments and will lead to slightly reduced growth. We therefore also assume that adjusted EBITDA total will be within the range of our most recently published guidance."

#FRANCE#

Total, a giant oil producer, reported that 1Q adjusted net income declined 35% on year to 1.78 billion dollars and adjusted net operating income slid 33% to 2.30 billion dollars. Also, daily average hydrocarbon production grew 4.8% to 3.09 million barrel of oil equivalent (boe). The company said it now expects 2020 production between 2.95 - 3.00 million boe per day, down 5% from its previous forecast, "reflecting the voluntary curtailment measures in Canada, the exceptional quotas announced by OPEC+, lower local demand for gas and the situation in Libya."

BNP Paribas, a banking group, announced that 1Q net income declined 33.2% on year to 1.28 billion euros and operating income dropped 32.2% to 1.31 billion euros on revenue of 10.89 billion euros, down 2.3%. Also, cost of risk rose 85.4% to 1.43 billion euros, amid coronavirus impacts. The bank said its full-year net income "could be about 15% to 20% lower than in 2019".

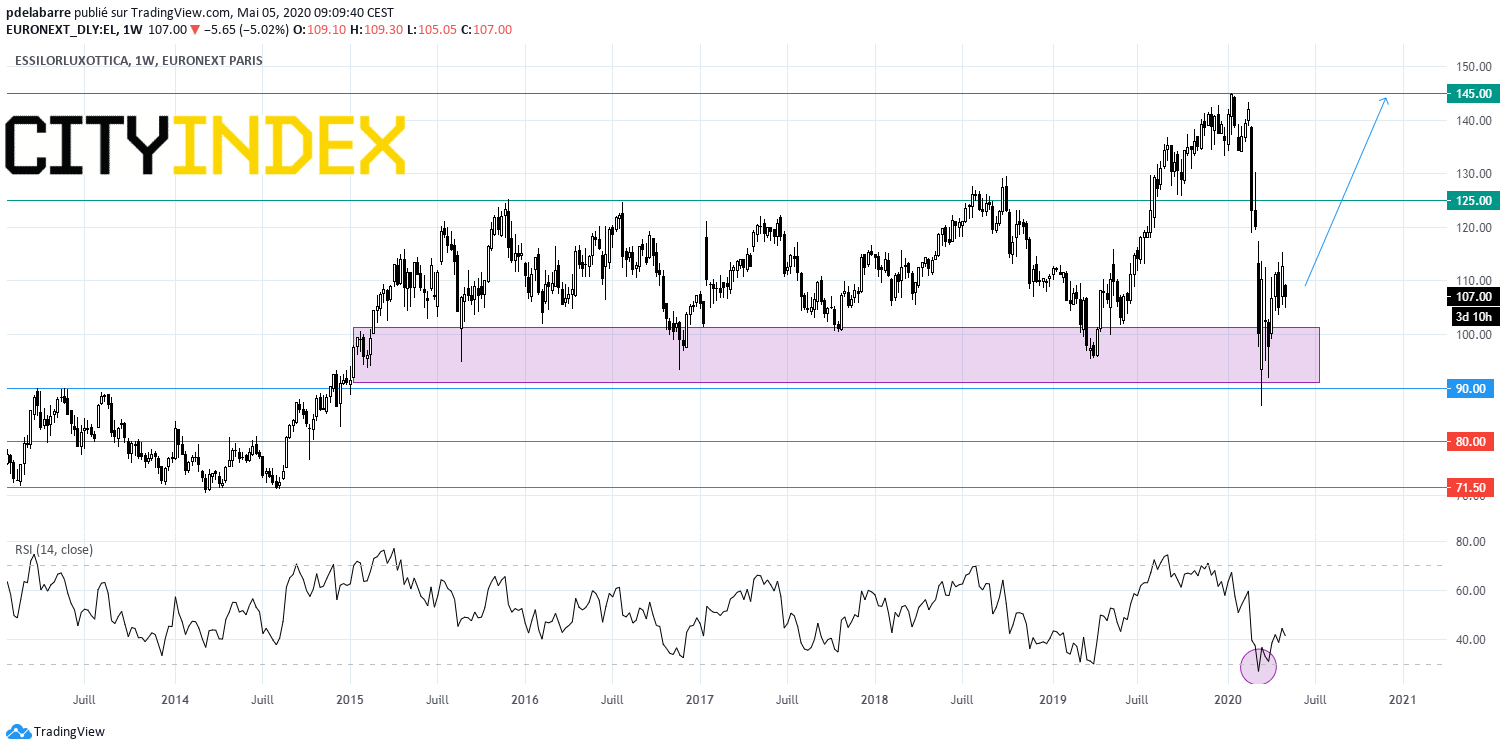

EssilorLuxottica, an eye-wear conglomerate, reported that 1Q revenue slid 10.1% on year (-10.9% at constant rates) to 3.78 billion euros.

Source: GAIN Capital, TradingView

#SPAIN#

Endesa, an electric utility group, announced that 1Q net income surged to 844 million euros from 363 million euros in the prior-year period and EBITDA jumped 59% on year to 1.48 billion euros on revenue of 5.07 billion euros, down 0.3%.

Repsol, a fossil fuel company, reported that 1Q adjusted net income dropped 28% on year to 447 million euros and CCS EBITDA slid 19% to 1.46 billion euros.

#SWITZERLAND#

Adecco, a human resources company, reported that it swung to a 1Q net loss of 348 million euros, citing a 362 million euros goodwill impairment. Also, EBITA dropped 38% to 136 million euros on revenue of 5.14 billion euros, down 9% (-8% organic growth).

#DENMARK#

Pandora, a jewelry manufacturer and retailer, reported that 1Q revenue declined 13% on year (-14% organic growth) to 4.17 billion Danish krone, citing negative impacts of COVID-19. The company said: "To protect the business during the pandemic and preserve a conservative balance sheet during these uncertain times, Pandora has arranged funding for a stress-test scenario. (...) Additional committed loan facilities of DKK 3.0 billion with the main relationship banks have been established. Additionally, Pandora intends to sell 8 million treasury shares in an accelerated book-building."

EX-DIVIDEND

Bouygues: E1.7, Philips: E0.85, Schneider Electric: E2.55

Yesterday, European stocks got heavier, with the Stoxx Europe 600 Index slumping 2.7%. Germany's DAX 30 tumbled 3.6%, France's CAC 40 plunged 4.2%, and the U.K.'s FTSE 100 edged down a little 0.2%.

EUROPE ADVANCE/DECLINE

87% of STOXX 600 constituents traded lower or unchanged yesterday.

55% of the shares trade above their 20D MA vs 74% Friday (below the 20D moving average).

20% of the shares trade above their 200D MA vs 20% Friday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 4.41pts to 38.32, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: none

3mths relative low: none

Europe Best 3 sectors

health care, retail, telecommunications

Europe worst 3 sectors

energy, banks, automobiles & parts

INTEREST RATE

The 10yr Bund yield was unchanged to -0.59% (below its 20D MA). The 2yr-10yr yield spread fell 1bp to -19bps (above its 20D MA).

ECONOMIC DATA

FR 07:45: Mar Budget Balance, exp.: E-35.2B

UK 09:00: Apr New Car Sales YoY, exp.: -44.4%

UK 09:30: Apr Markit/CIPS UK Services PMI final, exp.: 34.5

UK 09:30: Apr Markit/CIPS Composite PMI final, exp.: 36

EC 10:00: Mar PPI MoM, exp.: -0.6%

EC 10:00: Mar PPI YoY, exp.: -1.3%

MORNING TRADING

In Asian trading hours, EUR/USD held above the 1.0900 level while GBP/USD bounced slight to 1.2468. USD/JPY remained subdued at 106.58. AUD/USD climbed further to 0.6452 ahead of the Reserve Bank of Australia's rates decision.

Spot gold fell to $1,697 an ounce.

#UK - IRELAND#

Wizz Air, a low-cost airline company, reported that passengers capacity slumped 97.1% on year to 104,956 in April and the load factor dropped 17.3 percentage points to 74.7%.

Royal Mail, a postal service provider, was downgraded to "hold" from "sell" at Deutsche Bank.

#GERMANY#

Infineon Technologies, a semiconductor manufacturer, reported that 2Q net income dropped 15.2% on year to 178 million euros on revenue of 1.99 billion euros, up 3.7%. The company sees full-year revenue of "around E7.6 billion excluding Cypress and around E8.4 billion including Cypress, plus or minus 5 percent", citing a significantly weaker 2H outlook due to the coronavirus crisis.

SAP, a multinational software developer, said it "has identified that some of its cloud products do not meet one or several contractually agreed or statutory IT security standards at present", though "it does not believe that any customer data has been compromised as a result of these issues". The company added that it has initiated remediation of the identified areas of shortcoming, while the related expenses are expected to be covered within the range of its current financial outlook. Meanwhile, the company reported that it has agreed to sell its Digital Interconnect group to Sinch for 225 million euros.

Beiersdorf, a personal-care products manufacturer, posted 1Q revenue fell 1.9% on year (-3.6% organic growth) to 1.91 billion euros. The company said it has withdrawn its 2020 guidance issued on March 3, due to the coronavirus crisis.

Vonovia, a real estate group, announced that 1Q funds from operations increased 10.5% to 336 million euros and adjusted EDBITA grew 6.1% to 456 million euros on rental income of 564 million euros, up 12.3%. Regarding full-year outlook, the company stated: "We assume that the coronavirus will have only a limited impact on all business segments and will lead to slightly reduced growth. We therefore also assume that adjusted EBITDA total will be within the range of our most recently published guidance."

#FRANCE#

Total, a giant oil producer, reported that 1Q adjusted net income declined 35% on year to 1.78 billion dollars and adjusted net operating income slid 33% to 2.30 billion dollars. Also, daily average hydrocarbon production grew 4.8% to 3.09 million barrel of oil equivalent (boe). The company said it now expects 2020 production between 2.95 - 3.00 million boe per day, down 5% from its previous forecast, "reflecting the voluntary curtailment measures in Canada, the exceptional quotas announced by OPEC+, lower local demand for gas and the situation in Libya."

BNP Paribas, a banking group, announced that 1Q net income declined 33.2% on year to 1.28 billion euros and operating income dropped 32.2% to 1.31 billion euros on revenue of 10.89 billion euros, down 2.3%. Also, cost of risk rose 85.4% to 1.43 billion euros, amid coronavirus impacts. The bank said its full-year net income "could be about 15% to 20% lower than in 2019".

EssilorLuxottica, an eye-wear conglomerate, reported that 1Q revenue slid 10.1% on year (-10.9% at constant rates) to 3.78 billion euros.

Source: GAIN Capital, TradingView

#SPAIN#

Endesa, an electric utility group, announced that 1Q net income surged to 844 million euros from 363 million euros in the prior-year period and EBITDA jumped 59% on year to 1.48 billion euros on revenue of 5.07 billion euros, down 0.3%.

Repsol, a fossil fuel company, reported that 1Q adjusted net income dropped 28% on year to 447 million euros and CCS EBITDA slid 19% to 1.46 billion euros.

#SWITZERLAND#

Adecco, a human resources company, reported that it swung to a 1Q net loss of 348 million euros, citing a 362 million euros goodwill impairment. Also, EBITA dropped 38% to 136 million euros on revenue of 5.14 billion euros, down 9% (-8% organic growth).

#DENMARK#

Pandora, a jewelry manufacturer and retailer, reported that 1Q revenue declined 13% on year (-14% organic growth) to 4.17 billion Danish krone, citing negative impacts of COVID-19. The company said: "To protect the business during the pandemic and preserve a conservative balance sheet during these uncertain times, Pandora has arranged funding for a stress-test scenario. (...) Additional committed loan facilities of DKK 3.0 billion with the main relationship banks have been established. Additionally, Pandora intends to sell 8 million treasury shares in an accelerated book-building."

EX-DIVIDEND

Bouygues: E1.7, Philips: E0.85, Schneider Electric: E2.55

Latest market news

Latest Commodities articles

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM

April 14, 2024 11:37 PM