EU indices slightly down this morning | TA focus on Ocado Group

INDICES

Yesterday, European stocks rebounded, with the Stoxx Europe 600 Index gaining 2.2%. Germany's DAX 30 rebounded 2.5%, France's CAC 40 climbed 2.4%, and the U.K.'s FTSE 100 was up 1.7%.

EUROPE ADVANCE/DECLINE

80% of STOXX 600 constituents traded higher yesterday.

69% of the shares trade above their 20D MA vs 55% Monday (below the 20D moving average).

22% of the shares trade above their 200D MA vs 20% Monday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 3.82pts to 34.51, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: none

3mths relative low: none

Europe Best 3 sectors

energy, financial services, automobiles & parts

Europe worst 3 sectors

food & beverage, retail, personal & household goods

INTEREST RATE

The 10yr Bund yield rose 2bps to -0.56% (below its 20D MA). The 2yr-10yr yield spread fell 3bps to -21bps (above its 20D MA).

ECONOMIC DATA

GE 07:00: Mar Factory Orders MoM, exp.: -1.4%

FR 08:50: Apr Markit Services PMI final, exp.: 27.4

FR 08:50: Apr Markit Composite PMI final, exp.: 28.9

GE 08:55: Apr Markit Services PMI final, exp.: 31.7

GE 08:55: Apr Markit Composite PMI final, exp.: 35

EC 09:00: Apr Markit Services PMI final, exp.: 26.4

EC 09:00: Apr Markit Composite PMI final, exp.: 29.7

UK 09:30: Apr Construction PMI, exp.: 39.3

EC 10:00: Mar Retail Sales YoY, exp.: 3%

EC 10:00: Mar Retail Sales MoM, exp.: 0.9%

FR 10:00: Mar Retail Sales MoM, exp.: 1.1%

FR 10:00: Mar Retail Sales YoY, exp.: 3.4%

GE 10:40: 5-Year Bobl auction, exp.: -0.66%

MORNING TRADING

In Asian trading hours, EUR/USD remained subdued at 1.0839 while GBP/USD was flat at 1.2439. USD/JPY slid further to 106.30.

Spot gold held above $1,700 an ounce.

#UK - IRELAND#

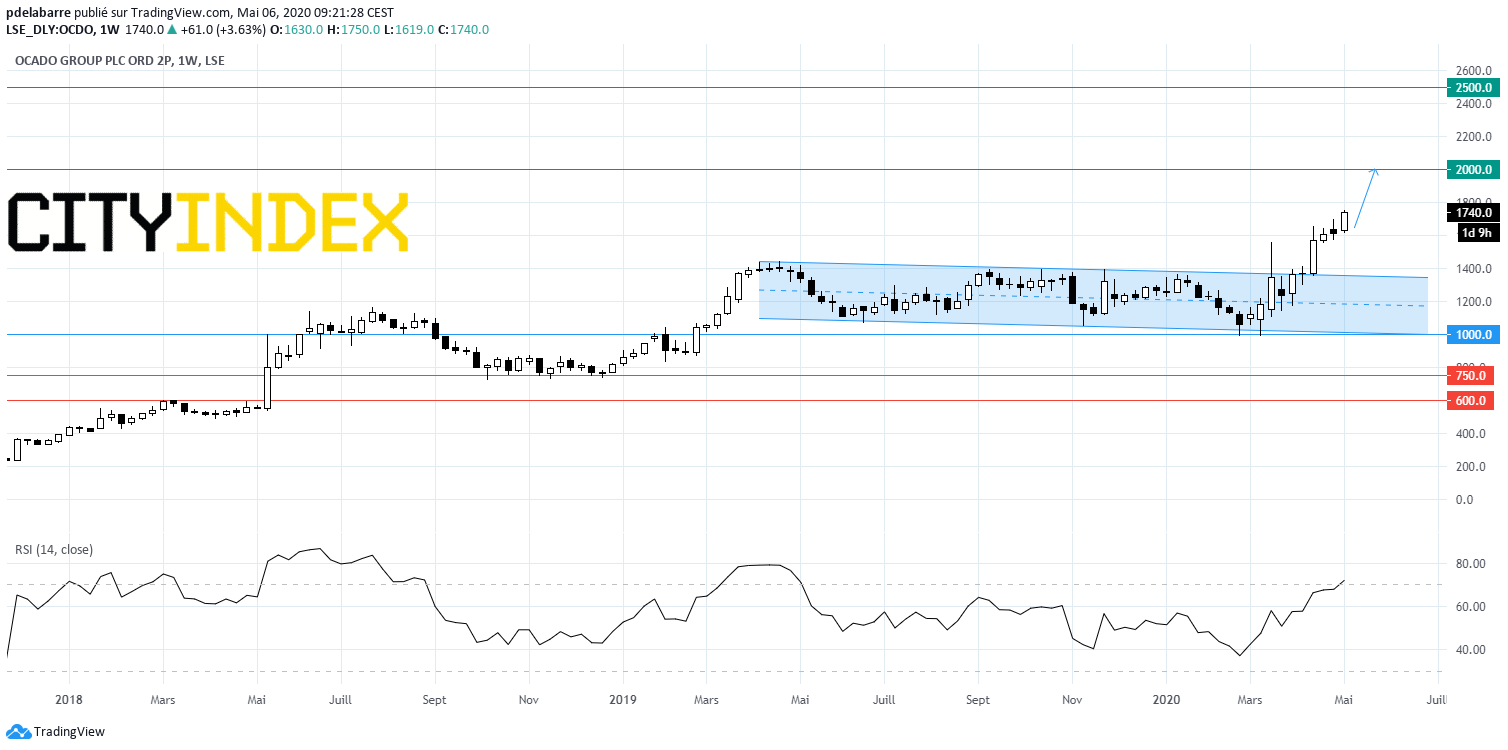

Ocado Group, an online grocery retailer, posted a trading update: "Growth in Retail Revenue in the Second Quarter to date is 40.4% up on last year, compared to 10.3% growth in the First Quarter. The number of items per basket appears to have passed its peak but remains high, as more normal shopping behaviors have returned, and the share of fresh and chilled products in the mix, relative to ambient, is also returning to normal."

Source: GAIN Capital, TradingView

ITV, a media company, released a 1Q trading statement: "Total external revenue was down 7% at £694m (2019: £743m). (...) Significant impact on the demand for advertising across most advertising categories, particularly from April which was down 42%. (...) The outlook remains uncertain and is changing rapidly and therefore we are not giving guidance for Q2 or for the remainder of the year."

JD Sports Fashion, a retailer of fashionable and own brand sports wear, commented on the Competition and Markets Authority's (CMA) decision to prohibit the Company's acquisition of Footasylum Limited: "We firmly believe that the CMA has failed to meet its objective of protecting consumer interests and today's decision will be detrimental for Footasylum, its customers, its 2,500 staff and the UK sports retail market as a whole. We are carefully considering whether to make an application to the Competition Appeal Tribunal to review this decision."

Smith and Nephew, a portfolio medical technology firm, provided a 1Q trading update: "Our first quarter revenue was 1,134 million dollars (2019: 1,202 million dollars), down -7.6% on an underlying basis, (...) Reported growth down -5.7% including a 3.4% benefit from acquisitions (...) Performance of all three global franchises held back by impact of COVID-19 to varying degrees (...) As previously announced, we expect that second quarter revenue and first half trading margin will be substantially down on the prior year."

AstraZeneca, a pharmaceutical group, said its Farxiga has been approved in the U.S. for the treatment of heart failure in patients with heart failure with reduced ejection fraction.

National Express, a public transport company, posted a market update: "In addition to the extensive series of measures the Group announced on 19 March and 14 April 2020 to help the business withstand this period of extreme uncertainty, National Express is today separately announcing a proposed placing of up to 19.99% of the Company's existing issued share capital."

#GERMANY#

Fresenius, a health care company, reported that 1Q net income grew 1% on year to 459 million euros and EBIT increased 1% to 1.13 billion euros on revenue of 9.14 billion euros, up 8%. The company said: "Fresenius will revisit this guidance when communicating its Q2/20 results with the aim to incorporate a reliable assessment of COVID-19 effects. (...) Fresenius expects to see a more pronounced negative COVID-19 effect on its financial results in the second quarter than in the first quarter of 2020."

Fresenius Medical Care, a dialysis products and services provider, posted 1Q net income rose 4% on year to 283 million euros and operating income climbed 3% to 555 million euros on revenue of 4.49 billion euros, up 9% (+7% at constant currency).

Hannover Re, an insurance group, announced that 1Q net income grew 2.5% on year to 301 million euros while EBIT slid 5.2% to 427 million euros on gross written premium of 7.0 billion euros, up 9.4% (+8.5% currency adjusted).

Fraport, an airport operator, said it swung to a 1Q net loss of 36 million euros from a net profit of 28 million euros in the prior-year period and EBIT sank 85.7% on year to 12 million euros on revenue of 661 million euros, down 17.8%. Regarding the outlook, the company said: "Since there continues to be a high level of uncertainty, it is impossible to make any detailed forecasts at this time. However, the Executive Board confirms its outlook that all key performance indicators will decline significantly, and anticipates a negative Group result for the full 2020 fiscal year."

#FRANCE#

Credit Agricole, a banking group, announced that 1Q net income declined 32.8% on year to 908 million euros and operating income fell 5.4% to 2.36 billion euros on revenue of 8.37 billion euros, up 2.1%. Also, cost of risk jumped to 930 million euros from 281 million euros in the prior-year period, while CET1 slipped 0.7 percentage point to 11.4%.

Veolia Environnement, an utility and public transportation group, reported that 1Q current net income slid 41.9% on year to 121 million euros and EBITDA fell 5.9% to 970 million euros on revenue of 6.68 billion euros, down 1.6% (-0.5% at constant scope and exchange rates).

Arkema, specialty chemicals and advanced materials company, reported that 1Q adjusted net income declined 39.4% on year to 100 million euros and EBITDA dropped 18.9% to 300 million euros on revenue of 2.09 billion euros, down 5.7%.

#SPAIN#

Siemens Gamesa, a wind turbines manufacturer, said it swung to a 2Q net loss of 165 million euros from a net profit of 49 million euros, and adjusted EBIT slumped to 33 million euros from 178 million euros on revenue of 2.20 billion euros, down 7.7% on year.

#BENELUX#

Solvay, a chemical company, reported that 1Q net income posted 1Q underlying net income dropped 18.3% on year to 236 million euros and underlying EBITDA fell 0.4% to 569 million euros on net sales of 2.47 billion euros, down 3.8% (-4.3% organic growth).

#ITALY#

UniCredit, an Italian bank, announced that it swung to a 1Q net loss of 2.71 billion euros and loan-loss provision increased to 1.26 billion euros from 467 million euros in the prior-year period. Also, revenue was down 8.2% on year to 4.38 billion euros, while CET1 ratio rose 23 basis points from the prior quarter to 13.44%.

#DENMARK#

Novo Nordisk, a pharmaceutical group, reported that 1Q net income increased 14% on year to 11.90 billion Danish krone and operating profit rose 14% to 16.30 billion Danish krone on net sales of 33.88 billion Danish krone, up 16% (+14% at constant exchange rates). The company confirmed its full-year sales growth forecast of 3% - 6% and operating growth of 1% - 5%, both at constant exchange rates.

Yesterday, European stocks rebounded, with the Stoxx Europe 600 Index gaining 2.2%. Germany's DAX 30 rebounded 2.5%, France's CAC 40 climbed 2.4%, and the U.K.'s FTSE 100 was up 1.7%.

EUROPE ADVANCE/DECLINE

80% of STOXX 600 constituents traded higher yesterday.

69% of the shares trade above their 20D MA vs 55% Monday (below the 20D moving average).

22% of the shares trade above their 200D MA vs 20% Monday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 3.82pts to 34.51, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: none

3mths relative low: none

Europe Best 3 sectors

energy, financial services, automobiles & parts

Europe worst 3 sectors

food & beverage, retail, personal & household goods

INTEREST RATE

The 10yr Bund yield rose 2bps to -0.56% (below its 20D MA). The 2yr-10yr yield spread fell 3bps to -21bps (above its 20D MA).

ECONOMIC DATA

GE 07:00: Mar Factory Orders MoM, exp.: -1.4%

FR 08:50: Apr Markit Services PMI final, exp.: 27.4

FR 08:50: Apr Markit Composite PMI final, exp.: 28.9

GE 08:55: Apr Markit Services PMI final, exp.: 31.7

GE 08:55: Apr Markit Composite PMI final, exp.: 35

EC 09:00: Apr Markit Services PMI final, exp.: 26.4

EC 09:00: Apr Markit Composite PMI final, exp.: 29.7

UK 09:30: Apr Construction PMI, exp.: 39.3

EC 10:00: Mar Retail Sales YoY, exp.: 3%

EC 10:00: Mar Retail Sales MoM, exp.: 0.9%

FR 10:00: Mar Retail Sales MoM, exp.: 1.1%

FR 10:00: Mar Retail Sales YoY, exp.: 3.4%

GE 10:40: 5-Year Bobl auction, exp.: -0.66%

MORNING TRADING

In Asian trading hours, EUR/USD remained subdued at 1.0839 while GBP/USD was flat at 1.2439. USD/JPY slid further to 106.30.

Spot gold held above $1,700 an ounce.

#UK - IRELAND#

Ocado Group, an online grocery retailer, posted a trading update: "Growth in Retail Revenue in the Second Quarter to date is 40.4% up on last year, compared to 10.3% growth in the First Quarter. The number of items per basket appears to have passed its peak but remains high, as more normal shopping behaviors have returned, and the share of fresh and chilled products in the mix, relative to ambient, is also returning to normal."

Source: GAIN Capital, TradingView

ITV, a media company, released a 1Q trading statement: "Total external revenue was down 7% at £694m (2019: £743m). (...) Significant impact on the demand for advertising across most advertising categories, particularly from April which was down 42%. (...) The outlook remains uncertain and is changing rapidly and therefore we are not giving guidance for Q2 or for the remainder of the year."

JD Sports Fashion, a retailer of fashionable and own brand sports wear, commented on the Competition and Markets Authority's (CMA) decision to prohibit the Company's acquisition of Footasylum Limited: "We firmly believe that the CMA has failed to meet its objective of protecting consumer interests and today's decision will be detrimental for Footasylum, its customers, its 2,500 staff and the UK sports retail market as a whole. We are carefully considering whether to make an application to the Competition Appeal Tribunal to review this decision."

Smith and Nephew, a portfolio medical technology firm, provided a 1Q trading update: "Our first quarter revenue was 1,134 million dollars (2019: 1,202 million dollars), down -7.6% on an underlying basis, (...) Reported growth down -5.7% including a 3.4% benefit from acquisitions (...) Performance of all three global franchises held back by impact of COVID-19 to varying degrees (...) As previously announced, we expect that second quarter revenue and first half trading margin will be substantially down on the prior year."

AstraZeneca, a pharmaceutical group, said its Farxiga has been approved in the U.S. for the treatment of heart failure in patients with heart failure with reduced ejection fraction.

National Express, a public transport company, posted a market update: "In addition to the extensive series of measures the Group announced on 19 March and 14 April 2020 to help the business withstand this period of extreme uncertainty, National Express is today separately announcing a proposed placing of up to 19.99% of the Company's existing issued share capital."

#GERMANY#

Fresenius, a health care company, reported that 1Q net income grew 1% on year to 459 million euros and EBIT increased 1% to 1.13 billion euros on revenue of 9.14 billion euros, up 8%. The company said: "Fresenius will revisit this guidance when communicating its Q2/20 results with the aim to incorporate a reliable assessment of COVID-19 effects. (...) Fresenius expects to see a more pronounced negative COVID-19 effect on its financial results in the second quarter than in the first quarter of 2020."

Fresenius Medical Care, a dialysis products and services provider, posted 1Q net income rose 4% on year to 283 million euros and operating income climbed 3% to 555 million euros on revenue of 4.49 billion euros, up 9% (+7% at constant currency).

Hannover Re, an insurance group, announced that 1Q net income grew 2.5% on year to 301 million euros while EBIT slid 5.2% to 427 million euros on gross written premium of 7.0 billion euros, up 9.4% (+8.5% currency adjusted).

Fraport, an airport operator, said it swung to a 1Q net loss of 36 million euros from a net profit of 28 million euros in the prior-year period and EBIT sank 85.7% on year to 12 million euros on revenue of 661 million euros, down 17.8%. Regarding the outlook, the company said: "Since there continues to be a high level of uncertainty, it is impossible to make any detailed forecasts at this time. However, the Executive Board confirms its outlook that all key performance indicators will decline significantly, and anticipates a negative Group result for the full 2020 fiscal year."

#FRANCE#

Credit Agricole, a banking group, announced that 1Q net income declined 32.8% on year to 908 million euros and operating income fell 5.4% to 2.36 billion euros on revenue of 8.37 billion euros, up 2.1%. Also, cost of risk jumped to 930 million euros from 281 million euros in the prior-year period, while CET1 slipped 0.7 percentage point to 11.4%.

Veolia Environnement, an utility and public transportation group, reported that 1Q current net income slid 41.9% on year to 121 million euros and EBITDA fell 5.9% to 970 million euros on revenue of 6.68 billion euros, down 1.6% (-0.5% at constant scope and exchange rates).

Arkema, specialty chemicals and advanced materials company, reported that 1Q adjusted net income declined 39.4% on year to 100 million euros and EBITDA dropped 18.9% to 300 million euros on revenue of 2.09 billion euros, down 5.7%.

#SPAIN#

Siemens Gamesa, a wind turbines manufacturer, said it swung to a 2Q net loss of 165 million euros from a net profit of 49 million euros, and adjusted EBIT slumped to 33 million euros from 178 million euros on revenue of 2.20 billion euros, down 7.7% on year.

#BENELUX#

Solvay, a chemical company, reported that 1Q net income posted 1Q underlying net income dropped 18.3% on year to 236 million euros and underlying EBITDA fell 0.4% to 569 million euros on net sales of 2.47 billion euros, down 3.8% (-4.3% organic growth).

#ITALY#

UniCredit, an Italian bank, announced that it swung to a 1Q net loss of 2.71 billion euros and loan-loss provision increased to 1.26 billion euros from 467 million euros in the prior-year period. Also, revenue was down 8.2% on year to 4.38 billion euros, while CET1 ratio rose 23 basis points from the prior quarter to 13.44%.

#DENMARK#

Novo Nordisk, a pharmaceutical group, reported that 1Q net income increased 14% on year to 11.90 billion Danish krone and operating profit rose 14% to 16.30 billion Danish krone on net sales of 33.88 billion Danish krone, up 16% (+14% at constant exchange rates). The company confirmed its full-year sales growth forecast of 3% - 6% and operating growth of 1% - 5%, both at constant exchange rates.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM