EU indices significantly up this morning | TA focus on Adidas

INDICES

On Friday, European stocks were broadly lower, with the Stoxx Europe 600 Index falling 1.1%. Germany's DAX 30 fell 1.7%, and both the U.K.'s FTSE 100 and France's CAC 40 were down 1.3%.

EUROPE ADVANCE/DECLINE

74% of STOXX 600 constituents traded lower or unchanged Friday.

65% of the shares trade above their 20D MA vs 74% Thursday (above the 20D moving average).

21% of the shares trade above their 200D MA vs 21% Thursday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 0.18pt to 40.17, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Healthcare

3mths relative low: none

Europe Best 3 sectors

health care, real estate, food & beverage

Europe worst 3 sectors

travel & leisure, banks, energy

INTEREST RATE

The 10yr Bund yield fell 2bps to -0.42% (below its 20D MA). The 2yr-10yr yield spread rose 1bp to -23bps (above its 20D MA).

ECONOMIC DATA

FR 11:00: Mar Jobseekers Total, exp.: 3233.8K

FR 11:00: Mar Unemployment Benefit Claims, exp.: -31K

FR 14:00: 12-Mth BTF auction, exp.: -0.39%

FR 14:00: 3-Mth BTF auction, exp.: -0.45%

FR 14:00: 6-Mth BTF auction, exp.: -0.41%

MORNING TRADING

In Asian trading hours, EUR/USD held gains at 1.0824 and GBP/USD advanced to 1.2388. USD/JPY dropped to 107.36. Earlier today, the Bank of Japan announced that it will purchase necessary amount of Japanese government bonds with no limit, compared with a previous target of 80 trillion yen, while keeping its benchmark rate at -0.1% unchanged.

Spot gold dropped to $1,722 an ounce.

On Friday, European stocks were broadly lower, with the Stoxx Europe 600 Index falling 1.1%. Germany's DAX 30 fell 1.7%, and both the U.K.'s FTSE 100 and France's CAC 40 were down 1.3%.

EUROPE ADVANCE/DECLINE

74% of STOXX 600 constituents traded lower or unchanged Friday.

65% of the shares trade above their 20D MA vs 74% Thursday (above the 20D moving average).

21% of the shares trade above their 200D MA vs 21% Thursday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 0.18pt to 40.17, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Healthcare

3mths relative low: none

Europe Best 3 sectors

health care, real estate, food & beverage

Europe worst 3 sectors

travel & leisure, banks, energy

INTEREST RATE

The 10yr Bund yield fell 2bps to -0.42% (below its 20D MA). The 2yr-10yr yield spread rose 1bp to -23bps (above its 20D MA).

ECONOMIC DATA

FR 11:00: Mar Jobseekers Total, exp.: 3233.8K

FR 11:00: Mar Unemployment Benefit Claims, exp.: -31K

FR 14:00: 12-Mth BTF auction, exp.: -0.39%

FR 14:00: 3-Mth BTF auction, exp.: -0.45%

FR 14:00: 6-Mth BTF auction, exp.: -0.41%

MORNING TRADING

In Asian trading hours, EUR/USD held gains at 1.0824 and GBP/USD advanced to 1.2388. USD/JPY dropped to 107.36. Earlier today, the Bank of Japan announced that it will purchase necessary amount of Japanese government bonds with no limit, compared with a previous target of 80 trillion yen, while keeping its benchmark rate at -0.1% unchanged.

Spot gold dropped to $1,722 an ounce.

#UK - IRELAND#

InterContinental Hotels Group, a hospitality company, posted a trading update: "IHG has secured new financing arrangements to further strengthen its liquidity position. (...) The amendment introduces a minimum liquidity covenant of $400m, tested at half year and full year, up to and including 30 June 2021. (...) The Bank of England has also now confirmed IHG as an eligible issuer for the UK Government's CCFF, and IHG has issued £600m (~$740m) in commercial paper under this facility. (...) we expect to report that Q1 Global RevPAR decreased approximately 25%, including a 55% decline in March, in line with the Business Update we provided on 20 March. Trading in Greater China continues to steadily improve, with only 12 out of 470 hotels now closed. In the US, ~10% of our hotels are currently closed."

Ashtead Group, an industrial equipment rental company, released a COVID-19 update: "As a result of these market dynamics, rental-only revenue for Sunbelt US in March was 2% higher than prior year and we expect April US rental-only revenue to be c. 15% lower than April 2019. (...) Since 10 April, we have seen the level of US fleet on rent stabilize and show a modest improvement. (...) Given these revenue trends, the Group now expects underlying profit before tax for the year ending 30 April 2020 to be c. £1,050m."

Admiral Group, a financial services provider, said it has decided to suspend the 20.7p per share dividend proposal for 2019, while confirming the normal dividend of 56.3p per share.

BAE Systems, a defense and aerospace company, was upgraded to "overweight" from "equalweight" at Goldman Sachs.

#GERMANY#

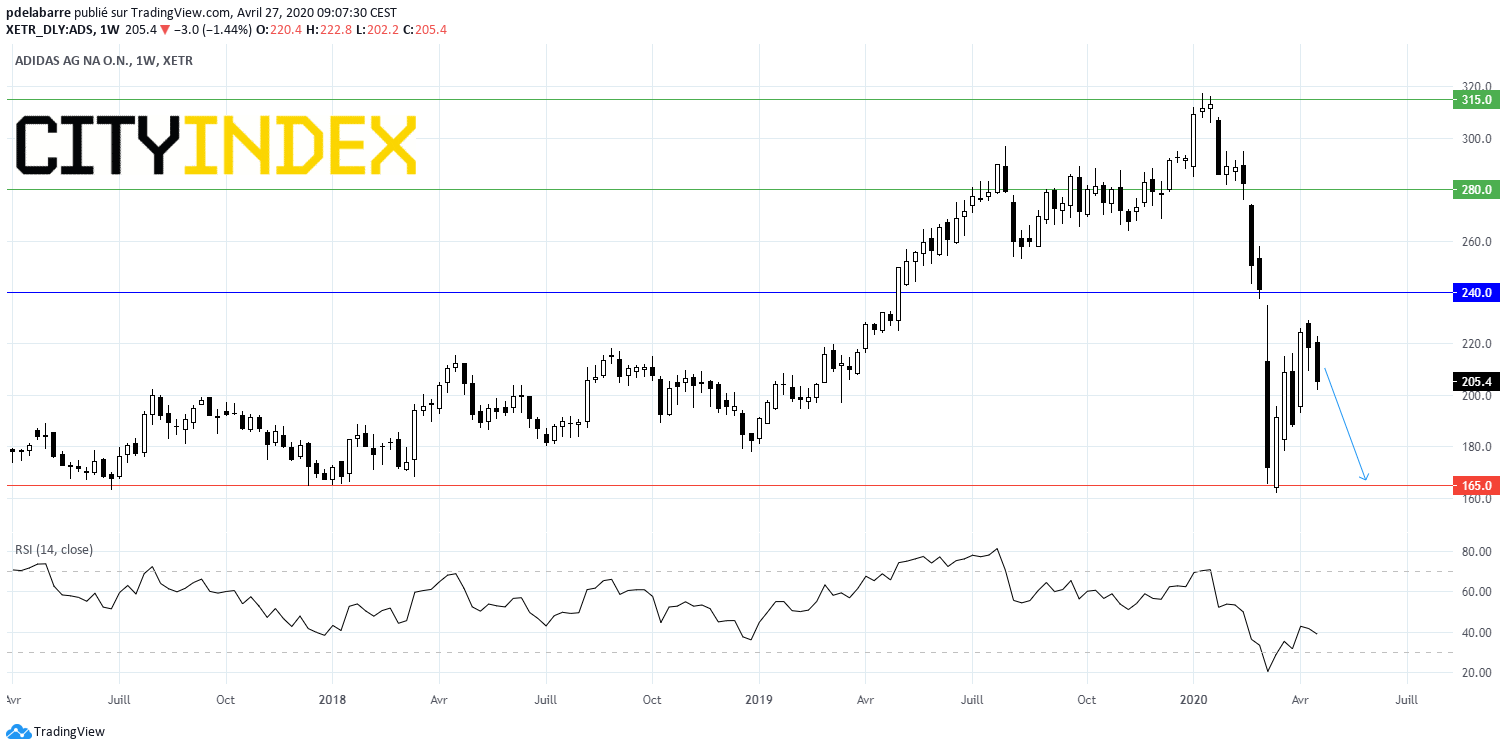

Adidas, a multinational sportswear company, announced that 1Q net income slumped 95.1% on year to 31 million euros and operating income plunged 92.6% to 65 million euros on net sales of 4.75 billion euros, down 19.2%. The company stated: "At this point in time, more than 70% of the company's store fleet is still closed. (...) Consequently, both top- and bottom-line declines in the second quarter of 2020 are currently expected to be more pronounced than those recorded in the first quarter, with currency-neutral sales projected to come in more than 40% below the prior year level and the operating result to be negative. (...) Adidas is still not able to provide an outlook for the full year 2020 that includes this impact."

Source: GAIN Capital, TradingView

Deutsche Bank, a banking group, announced that it expects 1Q net income of 66 million euros, "above market expectations", and revenues are estimated to be 6.4 billion euros. Also, CET1 ratio fell to 12.8% at quarter end from 13.6% at the end of prior year. Regarding financial targets, the bank stated: "The short-term implications of the COVID-19 pandemic make it difficult for the bank to accurately reflect the timing and the magnitude of changes to its original capital plan. Deutsche Bank's priority is to stand by its clients without compromising on capital strength. It is therefore possible that the bank will fall modestly and temporarily below its previous CET1 target of at least 12.5%. (...) This potential additional balance sheet growth also means that the bank is unlikely to reach its 2020 fully-loaded leverage ratio target of 4.5%."

#FRANCE#

Air France-KLM, an airline group, reported that it as secured funding of 7 billion euros from the French government and banks, to help overcome the coronavirus crisis. Meanwhile, the company said activity may bounce back to 70% of its potential by the end of year if passengers are recovered from the coronavirus panic, according to CEO Ben Smith cited by French newspaper Le Journal du Dimanche.

#PORTUGAL#

Galp Energia, a Portuguese oil and gas company, announced that 1Q adjusted net income dropped 72% on year to 29 million euros and adjusted EBITDA fell 5% to 469 million euros on revenue of 3.69 billion euros, up 4%.

#ITALY#

Leonardo, an aerospace and defense company, was downgraded to "equalweight" from "overweight" at Morgan Stanley.

#SWITZERLAND#

Kuehne + Nagel, a transport and logistics company, posted 1Q net income declined 23.2% on year to 139 million Swiss franc and EBITDA fell 9.6% to 378 million euros on revenue of 4.91 billion euros, down 6.2%.

#SWEDEN#

Sandvik, an engineering group, was upgraded to "overweight" from "neutral" at JPMorgan.

EX-DIVIDEND

Akzo Nobel: E1.49, Heineken: E1.04, Nestle: SF2.7, Wolters Kluwer: E0.79

Latest market news

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM