EU indices down this morning | TA focus on ENI

INDICES

Yesterday, European stocks remained firm, with the Stoxx Europe 600 Index adding 0.9%. Both Germany's DAX 30 and the U.K.'s FTSE 100 climbed 1.0%, and France's CAC 40 was up 0.9%..

EUROPE ADVANCE/DECLINE

73% of STOXX 600 constituents traded higher yesterday.

74% of the shares trade above their 20D MA vs 69% Wednesday (below the 20D moving average).

21% of the shares trade above their 200D MA vs 20% Wednesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 3.6pts to 40.35, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: none

3mths relative low: none

Europe Best 3 sectors

banks, energy, basic resources

Europe worst 3 sectors

retail, construction & materials, utilities

INTEREST RATE

The 10yr Bund yield rose 7bps to -0.41% (above its 20D MA). The 2yr-10yr yield spread rose 1bp to -24bps (below its 20D MA).

ECONOMIC DATA

UK 07:00: Mar Retail Sales MoM, exp.: -0.3%

UK 07:00: Mar Retail Sales YoY, exp.: 0%

UK 07:00: Mar Retail Sales ex Fuel MoM, exp.: -0.5%

UK 07:00: Mar Retail Sales ex Fuel YoY, exp.: 0.5%

GE 09:00: Apr Ifo Current Conditions, exp.: 93

GE 09:00: Apr Ifo expectations, exp.: 79.7

GE 09:00: Apr Ifo Business Climate, exp.: 86.1

MORNING TRADING

In Asian trading hours, EUR/USD remained subdued at 1.0770 while GBP/USD was broadly flat at 1.2349. USD/JPY was little changed at 107.63. This morning, government data showed that Japan's national CPI grew 0.4% on year in March (as expected).

Spot gold retreated to $1,724 an ounce.

#UK - IRELAND#

Pearson, publishing and education company, posted a 1Q trading update: "Trading is in line with revised expectations, revenue declined by 5% versus prior year driven by COVID-19. (...) Global Assessment revenue declined 3%. (...) International revenue declined 10%. (...) North American Course-ware revenue declined 10%. (...) Global Online Learning revenue grew 6%."

Persimmon, a house-building company, a house-building company, announced that it will begin a phased re-opening of its construction sites from April 27.

AstraZeneca, a bio-pharmaceutical company, said its Lynparza demonstrated overall survival benefit in phase 3 PROfound trial for BRCA1/2 or ATM-mutated metastatic castration-resistant prostate cancer.

Hikma Pharmaceuticals, a drug maker, was downgraded to "neutral" from "buy" at Goldman Sachs.

BAE Systems, a defense and aerospace company, was upgraded to "buy" from "hold" at Societe Generale.

Rolls-Royce and Meggitt, the two engineering groups were downgraded to "sell" from "hold" at Societe Generale.

#GERMANY#

Deutsche Lufthansa, an airline group, said it "expects a significant decline in liquidity in the coming weeks" and is "in intensive negotiations with the governments of its home countries regarding various financing instruments to sustainably secure the Group's solvency in the near future". Meanwhile, the company announced that preliminary 1Q adjusted EBIT loss widened to 1.2 billion euros from 336 million euros in the prior-year period and revenue dropped 18% on year to 6.4 billion euros. Also, available liquidity currently amounts to around 4.4 billion euros.

Uniper, an energy company, posted preliminary 1Q adjusted net income jumped to 500 million euros from 117 million euros in the prior-year period and adjusted EBIT surged to 650 million euros from 185 million euros.

#FRANCE#

Casino, a mass-market retail group, announced that 1Q net sales fell 0.8% on year (+7.9% organic growth) to 8.29 billion euros, citing "an unprecedented growth in demand directed for food retailing" due to the Covid-19 epidemic. The company added: "Sales in the last four weeks grew +24% on average at Franprix, Casino Supermarkets, and Convenience stores, which have seen a surge in new customers, and triple-figure growth in food E-commerce, especially in home delivery by Monoprix."

Air Liquide, an industrial gases supplier, reported that 1Q revenue fell 1.3% on year (+0.6% on a comparable basis) to 5.37 billion euros. The company stated: "The most widely held hypothesis today is that the second quarter will be highly impacted by the crisis, followed by gradual relaxation of lock-down measures between the end of the second quarter and the beginning of the third quarter, depending on the continent. (...) Air Liquide is nonetheless confident in its ability to further increase its operating margin and to deliver (full-year) net profit close to the 2019 level, at constant exchange rates."

Vinci, a concessions and construction company, reported that 1Q revenue was broadly flat on year at 9.69 billion euros (-3.3% on a like-for-like basis). The company said: "In these circumstances, we expect a pronounced decline in the Group's revenue in the next few months. (...) It appears nevertheless that VINCI will be unable to meet its target, announced on 5 February 2020, of achieving revenue and net income growth in 2020."

Saint-Gobain, a construction materials producer, reported that 1Q revenue slid 9.8% on year (-4.9% like-for-like) to 9.36 billion euros, with volumes down 5.5%. The company said: "Given the impact of the global economic crisis caused by the coronavirus, the Group expects a challenging second quarter 2020 before a recovery in the second half."

Bureau Veritas, a laboratory testing and certification services provider, posted 1Q revenue fell 3.0% on year (-1.6% organic growth) to 1.14 billion euros. Regarding the outlook, the company said: "In these unprecedented circumstances, the 2020 targets are no longer relevant. (...) The Group expects a very significant impact on the second quarter (Q2) of 2020, due to the lockdown measures that have been put in place in Europe, the United States and Latin America notably. (...) Bureau Veritas' Board of Directors took the exceptional decision to cancel the dividend (EUR 0.56 per share) due to be proposed."

Safran, a defense and aerospace company, was downgraded to "sell" from "hold" at Societe Generale.

#ITALY#

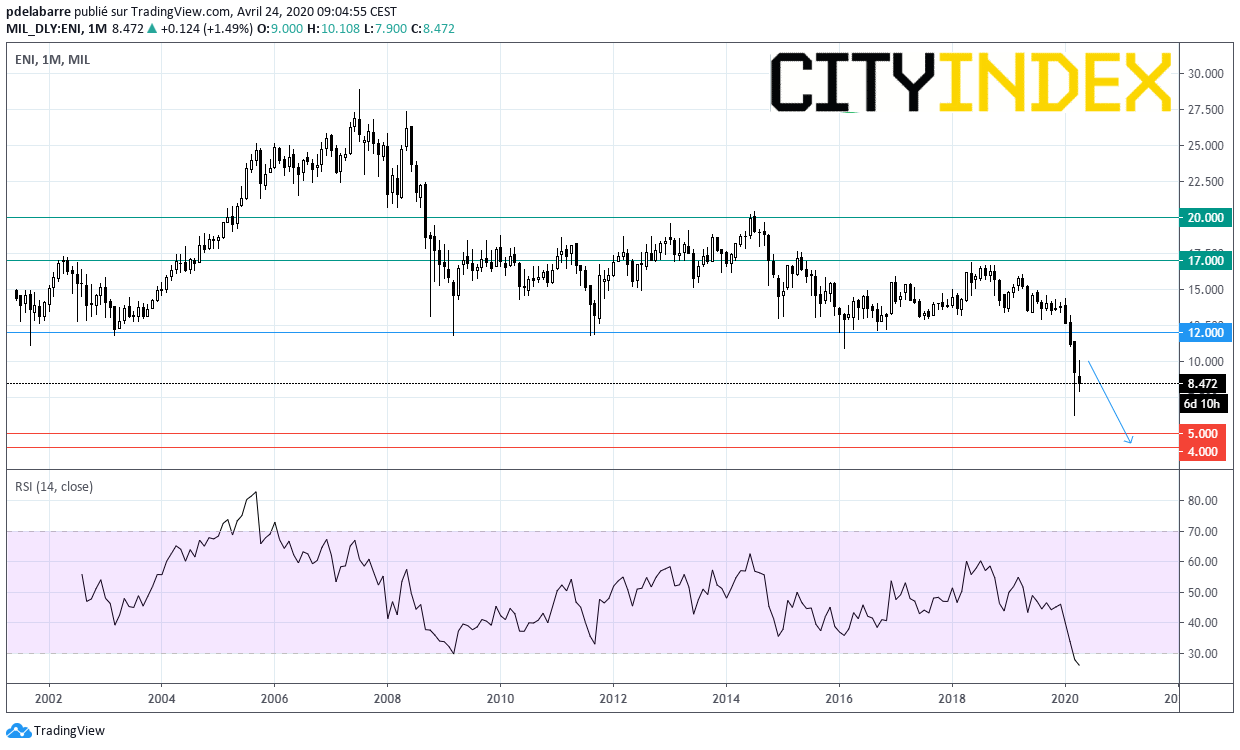

ENI, an oil and gas company, reported that 1Q net income slumped to 59 million euros from 992 million euros in the prior-year period and adjusted operating income declined 44% on year to 1.31 billion euros. The company said it has lowered 2020 capex forecast by 30%, compared with its initial plan, and suspended the share repurchase plan for 2020.

Source: GAIN Capital, TradingView

#SWITZERLAND#

Nestle, a food and drink processing conglomerate, announced that 1Q revenue slid 6.2% on year (+4.3% organic growth) to 20.81 billion Swiss franc. Regarding the outlook, the company said: "As it is still too early to assess the full impact of COVID-19, we maintain our original full-year 2020 guidance for the time being. We expect continued improvement in organic sales growth and underlying trading operating profit margin. Underlying earnings per share in constant currency and capital efficiency are expected to increase."

#SCANDINAVIA - DENMARK#

Saab, a Swedish aerospace and defense company, reported that 1Q net income decreased 14% on year to 342 million Swedish krona and EBIT fell 5% to 560 million Swedish krona on revenue of 8.04 billion Swedish krona, down 5%.

EX-DIVIDEND

ASML Holding: E1.35, Atlas Copco: SEK3.5

Yesterday, European stocks remained firm, with the Stoxx Europe 600 Index adding 0.9%. Both Germany's DAX 30 and the U.K.'s FTSE 100 climbed 1.0%, and France's CAC 40 was up 0.9%..

EUROPE ADVANCE/DECLINE

73% of STOXX 600 constituents traded higher yesterday.

74% of the shares trade above their 20D MA vs 69% Wednesday (below the 20D moving average).

21% of the shares trade above their 200D MA vs 20% Wednesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 3.6pts to 40.35, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: none

3mths relative low: none

Europe Best 3 sectors

banks, energy, basic resources

Europe worst 3 sectors

retail, construction & materials, utilities

INTEREST RATE

The 10yr Bund yield rose 7bps to -0.41% (above its 20D MA). The 2yr-10yr yield spread rose 1bp to -24bps (below its 20D MA).

ECONOMIC DATA

UK 07:00: Mar Retail Sales MoM, exp.: -0.3%

UK 07:00: Mar Retail Sales YoY, exp.: 0%

UK 07:00: Mar Retail Sales ex Fuel MoM, exp.: -0.5%

UK 07:00: Mar Retail Sales ex Fuel YoY, exp.: 0.5%

GE 09:00: Apr Ifo Current Conditions, exp.: 93

GE 09:00: Apr Ifo expectations, exp.: 79.7

GE 09:00: Apr Ifo Business Climate, exp.: 86.1

MORNING TRADING

In Asian trading hours, EUR/USD remained subdued at 1.0770 while GBP/USD was broadly flat at 1.2349. USD/JPY was little changed at 107.63. This morning, government data showed that Japan's national CPI grew 0.4% on year in March (as expected).

Spot gold retreated to $1,724 an ounce.

#UK - IRELAND#

Pearson, publishing and education company, posted a 1Q trading update: "Trading is in line with revised expectations, revenue declined by 5% versus prior year driven by COVID-19. (...) Global Assessment revenue declined 3%. (...) International revenue declined 10%. (...) North American Course-ware revenue declined 10%. (...) Global Online Learning revenue grew 6%."

Persimmon, a house-building company, a house-building company, announced that it will begin a phased re-opening of its construction sites from April 27.

AstraZeneca, a bio-pharmaceutical company, said its Lynparza demonstrated overall survival benefit in phase 3 PROfound trial for BRCA1/2 or ATM-mutated metastatic castration-resistant prostate cancer.

Hikma Pharmaceuticals, a drug maker, was downgraded to "neutral" from "buy" at Goldman Sachs.

BAE Systems, a defense and aerospace company, was upgraded to "buy" from "hold" at Societe Generale.

Rolls-Royce and Meggitt, the two engineering groups were downgraded to "sell" from "hold" at Societe Generale.

#GERMANY#

Deutsche Lufthansa, an airline group, said it "expects a significant decline in liquidity in the coming weeks" and is "in intensive negotiations with the governments of its home countries regarding various financing instruments to sustainably secure the Group's solvency in the near future". Meanwhile, the company announced that preliminary 1Q adjusted EBIT loss widened to 1.2 billion euros from 336 million euros in the prior-year period and revenue dropped 18% on year to 6.4 billion euros. Also, available liquidity currently amounts to around 4.4 billion euros.

Uniper, an energy company, posted preliminary 1Q adjusted net income jumped to 500 million euros from 117 million euros in the prior-year period and adjusted EBIT surged to 650 million euros from 185 million euros.

#FRANCE#

Casino, a mass-market retail group, announced that 1Q net sales fell 0.8% on year (+7.9% organic growth) to 8.29 billion euros, citing "an unprecedented growth in demand directed for food retailing" due to the Covid-19 epidemic. The company added: "Sales in the last four weeks grew +24% on average at Franprix, Casino Supermarkets, and Convenience stores, which have seen a surge in new customers, and triple-figure growth in food E-commerce, especially in home delivery by Monoprix."

Air Liquide, an industrial gases supplier, reported that 1Q revenue fell 1.3% on year (+0.6% on a comparable basis) to 5.37 billion euros. The company stated: "The most widely held hypothesis today is that the second quarter will be highly impacted by the crisis, followed by gradual relaxation of lock-down measures between the end of the second quarter and the beginning of the third quarter, depending on the continent. (...) Air Liquide is nonetheless confident in its ability to further increase its operating margin and to deliver (full-year) net profit close to the 2019 level, at constant exchange rates."

Vinci, a concessions and construction company, reported that 1Q revenue was broadly flat on year at 9.69 billion euros (-3.3% on a like-for-like basis). The company said: "In these circumstances, we expect a pronounced decline in the Group's revenue in the next few months. (...) It appears nevertheless that VINCI will be unable to meet its target, announced on 5 February 2020, of achieving revenue and net income growth in 2020."

Saint-Gobain, a construction materials producer, reported that 1Q revenue slid 9.8% on year (-4.9% like-for-like) to 9.36 billion euros, with volumes down 5.5%. The company said: "Given the impact of the global economic crisis caused by the coronavirus, the Group expects a challenging second quarter 2020 before a recovery in the second half."

Bureau Veritas, a laboratory testing and certification services provider, posted 1Q revenue fell 3.0% on year (-1.6% organic growth) to 1.14 billion euros. Regarding the outlook, the company said: "In these unprecedented circumstances, the 2020 targets are no longer relevant. (...) The Group expects a very significant impact on the second quarter (Q2) of 2020, due to the lockdown measures that have been put in place in Europe, the United States and Latin America notably. (...) Bureau Veritas' Board of Directors took the exceptional decision to cancel the dividend (EUR 0.56 per share) due to be proposed."

Safran, a defense and aerospace company, was downgraded to "sell" from "hold" at Societe Generale.

#ITALY#

ENI, an oil and gas company, reported that 1Q net income slumped to 59 million euros from 992 million euros in the prior-year period and adjusted operating income declined 44% on year to 1.31 billion euros. The company said it has lowered 2020 capex forecast by 30%, compared with its initial plan, and suspended the share repurchase plan for 2020.

Source: GAIN Capital, TradingView

#SWITZERLAND#

Nestle, a food and drink processing conglomerate, announced that 1Q revenue slid 6.2% on year (+4.3% organic growth) to 20.81 billion Swiss franc. Regarding the outlook, the company said: "As it is still too early to assess the full impact of COVID-19, we maintain our original full-year 2020 guidance for the time being. We expect continued improvement in organic sales growth and underlying trading operating profit margin. Underlying earnings per share in constant currency and capital efficiency are expected to increase."

#SCANDINAVIA - DENMARK#

Saab, a Swedish aerospace and defense company, reported that 1Q net income decreased 14% on year to 342 million Swedish krona and EBIT fell 5% to 560 million Swedish krona on revenue of 8.04 billion Swedish krona, down 5%.

EX-DIVIDEND

ASML Holding: E1.35, Atlas Copco: SEK3.5

Latest market news

Today 08:15 AM

Today 05:45 AM

Yesterday 11:09 PM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM