EU indices consolidate | TA focus on Zalando

INDICES

Yesterday, European stocks were firm, with the Stoxx Europe 600 Index rising 0.7%. Germany's DAX 30 increased 0.5%, France's CAC 40 advanced 0.9%, and the U.K.'s FTSE 100 was up 0.2%.

EUROPE ADVANCE/DECLINE

56% of STOXX 600 constituents traded higher yesterday.

73% of the shares trade above their 20D MA vs 73% Tuesday (below the 20D moving average).

41% of the shares trade above their 200D MA vs 38% Tuesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 0.74pt to 35.36, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Technology

3mths relative low: Telecom

Europe Best 3 sectors

health care, technology, retail

Europe worst 3 sectors

automobiles & parts, insurance, energy

INTEREST RATE

The 10yr Bund yield rose 2bps to -0.43% (below its 20D MA). The 2yr-10yr yield spread fell 4bps to -26bps (below its 20D MA).

ECONOMIC DATA

EC 09:00: ECB Economic Bulletin

FR 10:00: 3-Year BTAN auction, exp.: -0.53%

FR 10:00: 5-Year BTAN auction, exp.: -0.33%

UK 12:00: BoE Interest Rate Decision, exp.: 0.1%

UK 12:00: BoE Quantitative Easing, exp.: £645B

UK 12:00: MPC Meeting Minutes

UK 12:00: BoE MPC Vote Hike, exp.: 0/9

UK 12:00: BoE MPC Vote Unchanged, exp.: 44083

UK 12:00: BoE MPC Vote Cut, exp.: 0/9

MORNING TRADING

In Asian trading hours, EUR/USD fell to 1.1237 and GBP/USD dipped to 1.2534. USD/JPY dropped to 106.81. AUD/USD declined to 0.6853. This morning, official data showed that Australia's economy shed 227,700 jobs in May (-78,800 jobs expected), while jobless rate rose to 7.1% (6.9% expected) from 6.2% in April,

Spot gold was little changed at $1,725 an ounce.

#UK - IRELAND#

Tesco, a groceries and general merchandise retailer, said it has agreed to sell its business in Poland to Salling Group for a total enterprise value of 181 million pounds.

Taylor Wimpey, a housebuilding company, reported that it has raised 515 million pounds through the placing of 355 million new ordinary shares.

Schroders, an asset management company, was downgraded to "sell" from "neutral" at Goldman Sachs.

Marks & Spencer, a retailer, was upgraded to "buy" from "hold" at HSBC.

#GERMANY#

Source: GAIN Capital, TradingView

Wirecard, a payment processor and financial services provider, is expected to report 1Q results.

#FRANCE#

Remy Cointreau, a spirits company, was upgraded to "overweight" from "underweight" at Barclays.

#SPAIN#

Siemens Gamesa, a wind turbines manufacturer, announced the appointment of Andreas Nauen, currently Offshore head, as new CEO with immediate effect. At the same time, the company said "project costs and the financial impact of COVID-19 disruptions will result in a negative EBIT in the third quarter", and "the anticipated positive EBIT in the fourth quarter is not expected to completely offset the negative development for the full fiscal year".

Aena, an airport and heliport operator, was upgraded to "neutral" from "underweight" at JPMorgan.

#SWEDEN#

EQT, a Swedish investment group, has agreed to sell its 3.9 billion euros credit arm to private equity firm Bridgepoint, reported the Financial Times citing people familiar with the matter.

EX-DIVIDEND

ArcelorMittal: $0.3, Henkel: E1.85, Informa:15.95p, Investor: SEK9, Symrise: E0.95

Yesterday, European stocks were firm, with the Stoxx Europe 600 Index rising 0.7%. Germany's DAX 30 increased 0.5%, France's CAC 40 advanced 0.9%, and the U.K.'s FTSE 100 was up 0.2%.

EUROPE ADVANCE/DECLINE

56% of STOXX 600 constituents traded higher yesterday.

73% of the shares trade above their 20D MA vs 73% Tuesday (below the 20D moving average).

41% of the shares trade above their 200D MA vs 38% Tuesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index eased 0.74pt to 35.36, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Technology

3mths relative low: Telecom

Europe Best 3 sectors

health care, technology, retail

Europe worst 3 sectors

automobiles & parts, insurance, energy

INTEREST RATE

The 10yr Bund yield rose 2bps to -0.43% (below its 20D MA). The 2yr-10yr yield spread fell 4bps to -26bps (below its 20D MA).

ECONOMIC DATA

EC 09:00: ECB Economic Bulletin

FR 10:00: 3-Year BTAN auction, exp.: -0.53%

FR 10:00: 5-Year BTAN auction, exp.: -0.33%

UK 12:00: BoE Interest Rate Decision, exp.: 0.1%

UK 12:00: BoE Quantitative Easing, exp.: £645B

UK 12:00: MPC Meeting Minutes

UK 12:00: BoE MPC Vote Hike, exp.: 0/9

UK 12:00: BoE MPC Vote Unchanged, exp.: 44083

UK 12:00: BoE MPC Vote Cut, exp.: 0/9

MORNING TRADING

In Asian trading hours, EUR/USD fell to 1.1237 and GBP/USD dipped to 1.2534. USD/JPY dropped to 106.81. AUD/USD declined to 0.6853. This morning, official data showed that Australia's economy shed 227,700 jobs in May (-78,800 jobs expected), while jobless rate rose to 7.1% (6.9% expected) from 6.2% in April,

Spot gold was little changed at $1,725 an ounce.

#UK - IRELAND#

Tesco, a groceries and general merchandise retailer, said it has agreed to sell its business in Poland to Salling Group for a total enterprise value of 181 million pounds.

Taylor Wimpey, a housebuilding company, reported that it has raised 515 million pounds through the placing of 355 million new ordinary shares.

Schroders, an asset management company, was downgraded to "sell" from "neutral" at Goldman Sachs.

Marks & Spencer, a retailer, was upgraded to "buy" from "hold" at HSBC.

#GERMANY#

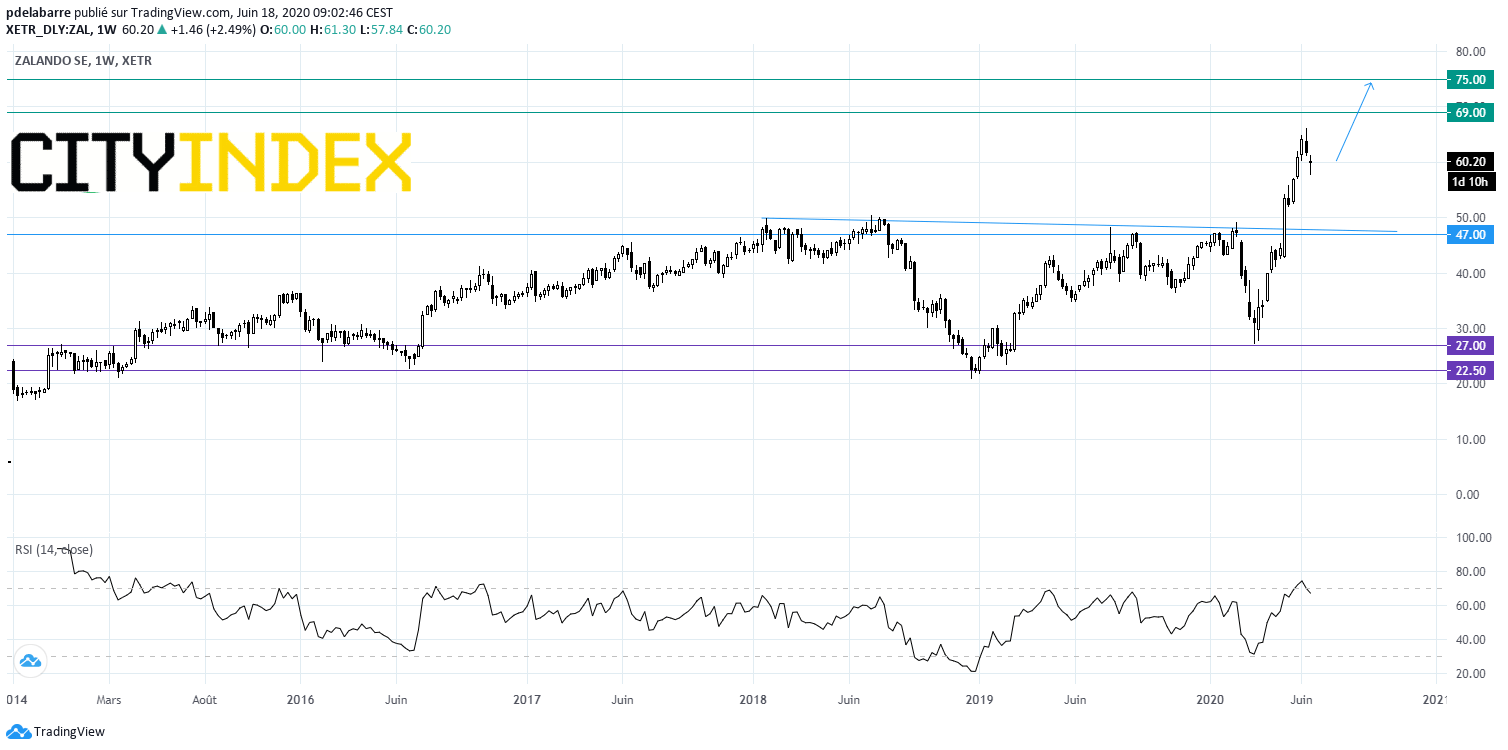

Zalando, an e-commerce company, said it "expects a significant increase in sales and EBIT in the second quarter, which is significantly above current market expectations", citing a strongly increasing consumer preference for digital offerings. From a chartist point of view, the upward breakout above the 48 area (resistance between 2018 & 2020) has triggered a new measured move up towards 75.

Source: GAIN Capital, TradingView

Wirecard, a payment processor and financial services provider, is expected to report 1Q results.

#FRANCE#

Remy Cointreau, a spirits company, was upgraded to "overweight" from "underweight" at Barclays.

#SPAIN#

Siemens Gamesa, a wind turbines manufacturer, announced the appointment of Andreas Nauen, currently Offshore head, as new CEO with immediate effect. At the same time, the company said "project costs and the financial impact of COVID-19 disruptions will result in a negative EBIT in the third quarter", and "the anticipated positive EBIT in the fourth quarter is not expected to completely offset the negative development for the full fiscal year".

Aena, an airport and heliport operator, was upgraded to "neutral" from "underweight" at JPMorgan.

#SWEDEN#

EQT, a Swedish investment group, has agreed to sell its 3.9 billion euros credit arm to private equity firm Bridgepoint, reported the Financial Times citing people familiar with the matter.

EX-DIVIDEND

ArcelorMittal: $0.3, Henkel: E1.85, Informa:15.95p, Investor: SEK9, Symrise: E0.95

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM