EU indices are rebounding this morning | TA focus on Ubisoft Entertainment

INDICES

Yesterday, European stocks were broadly lower, with the Stoxx Europe 600 Index falling 2.2%. Germany's DAX 30 dropped 2.0%, France's CAC 40 declined 1.7% and the U.K.'s FTSE 100 was down 2.8%.

EUROPE ADVANCE/DECLINE

88% of STOXX 600 constituents traded lower or unchanged yesterday.

29% of the shares trade above their 20D MA vs 50% Wednesday (below the 20D moving average).

21% of the shares trade above their 200D MA vs 24% Wednesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 2.9pts to 36.32, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Healthcare

3mths relative low: Insurance

Europe Best 3 sectors

basic resources, telecommunications, banks

Europe worst 3 sectors

retail, food & beverage, industrial goods & services

INTEREST RATE

The 10yr Bund yield fell 3bps to -0.53% (below its 20D MA). The 2yr-10yr yield spread rose 0bp to -20bps (above its 20D MA).

ECONOMIC DATA

GE 07:00: Apr PPI YoY, exp.: -0.8%

GE 07:00: Apr PPI MoM, exp.: -0.8%

FR 07:45: Apr Inflation Rate YoY final, exp.: 0.7%

FR 07:45: Apr Inflation Rate MoM final, exp.: 0.1%

FR 07:45: Apr Harmonised Inflation Rate MoM final, exp.: 0.1%

FR 07:45: Apr Harmonised Inflation Rate YoY final, exp.: 0.8%

GE 09:00: Q1 GDP Growth Rate QoQ Flash, exp.: 0%

GE 09:00: Q1 GDP Growth Rate YoY Flash, exp.: 0.4%

EC 10:00: Q1 GDP Growth Rate YoY 2nd Est, exp.: 1%

EC 10:00: Q1 GDP Growth Rate QoQ 2nd Est, exp.: 0.1%

EC 10:00: Q1 Employment chg QoQ Prel, exp.: 0.3%

EC 10:00: Q1 Employment chg YoY Prel, exp.: 1.1%

EC 10:00: Mar Balance of Trade, exp.: E23B

MORNING TRADING

In Asian trading hours, EUR/USD was flat at 1.0804 while GBP/USD fell to 1.2212. USD/JPY edged up to 107.33. AUD/USD eased to 0.6454. This morning, official data showed that China's industrial production rose 3.9% on year in April (+1.5% expected) while retail sales dropped 7.5% (-6.0% expected).

Spot gold advanced further to $1,733 an ounce.

#UK - IRELAND#

Computacenter, computer services provider, released a trading update for the four months to April 30: "We stated in our trading statement on 23rd April 2020 that current trading was more robust than we had anticipated at the start of the crisis. Since that date business has accelerated further and we have managed to secure some substantial Technology Sourcing contracts due to our ability to scale our operations to meet the demand. These incremental volumes mean that we now believe that the first half of 2020 will be considerably ahead of the same period of last year."

BP, a giant oil producer, was downgraded to "underweight" from "equalweight" at Morgan Stanley.

#GERMANY#

Hapag-Lloyd, a shipping and container transportation company, announced that 1Q net income slumped 74.0% on year to 25 million euros and EBITDA fell 4.1% to 469 billion euros on revenue of 3.34 billion euros, up 9.1%. Regarding full-year outlook, the company said: "Hapag-Lloyd admittedly still continues to expect EBITDA of EUR 1.7 - 2.2 billion and EBIT of EUR 0.5 - 1.0 billion for the current financial year. However, unless there is a recovery in demand for container transport services earlier and stronger than currently expected by the relevant market participants, the upper end of the forecast ranges is barely achievable from today’s perspective."

#FRANCE#

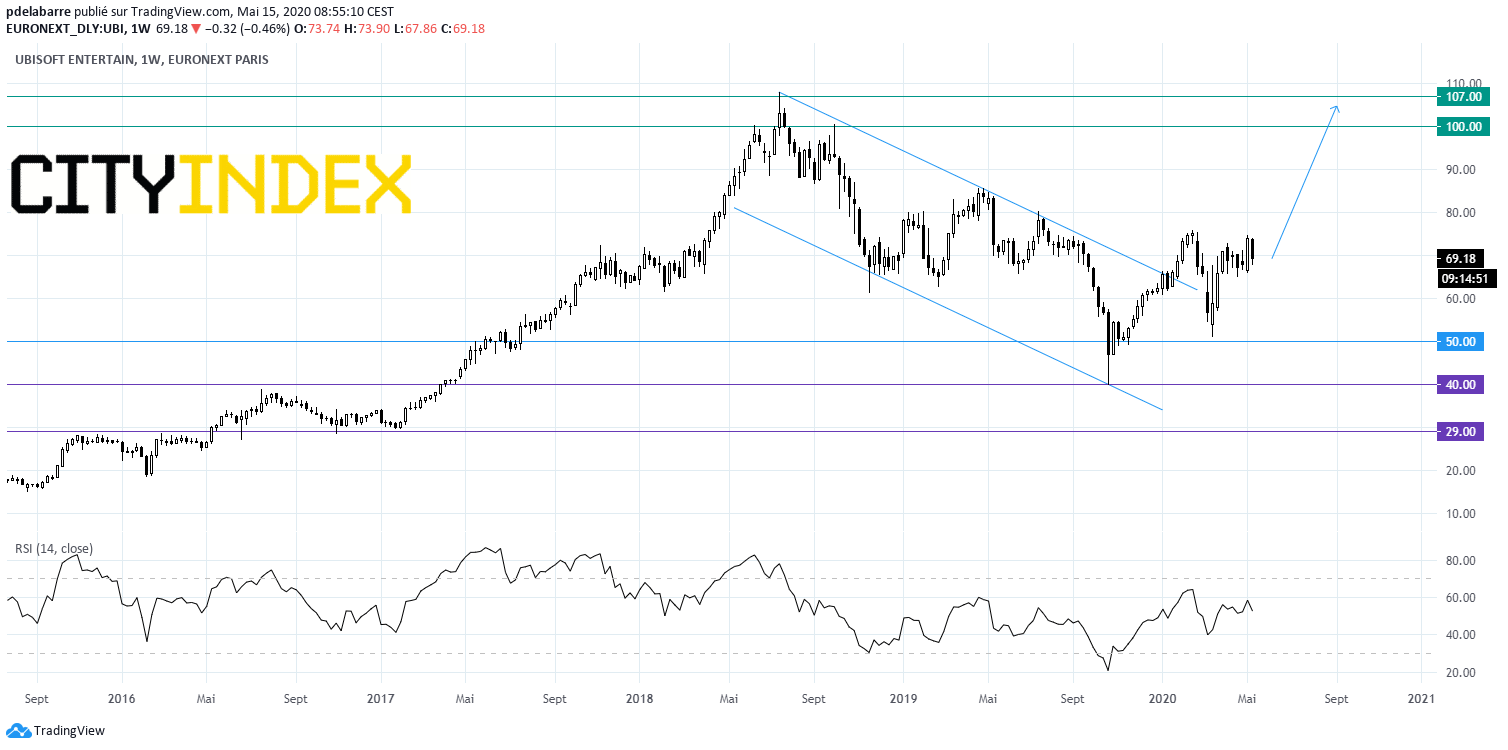

Ubisoft Entertainment, a video game producer, announced full-year adjusted LPS of 0.09 euros from an adjusted EPS of 2.80 in the prior year and adjusted operating income plunged to 34 million euros from 446 million euros last year. Also, revenue was down 13.6% on year to 1.59 billion euros and net bookings dropped 24.4% to 1.53 billion dollars. The company said it now expects 2020 - 2021 net bookings of 2.35 - 2.65 billion euros, compared with 2.60 billion euros previously, and adjusted operating income forecast is lowered to 400 - 600 million euros from 600 million euros.

Source: GAIN Capital, TradingView

#BENELUX#

Aegon's, an insurance company, "A-" credit rating outlook was revised to "Negative" from "Stable" at Fitch. The rating agency said: "The Outlook revision reflects disruption to economic activity and financial markets from the coronavirus pandemic."

#SWITZERLAND#

Richemont, a luxury goods company, announced that full-year net income declined 67% on year to 1.65 billion euros and operating profit dropped 22% to 1.52 billion euros on revenue of 14.24 billion euros, up 2%. The company stated: " The closures of our internal and external points of sales, changing attitudes towards consumption and subdued consumer sentiment will weigh on this year's results, even if, at the time of writing, we are gradually resuming operations as parts of the world emerge from lock-down. It is impossible to make meaningful predictions at this time."

Straumann, a tooth replacement solutions provider, was downgraded to "underweight" from "neutral" at JPMorgan.

#FINLAND#

Fortum, a Finnish energy company, announced that 1Q EPS jumped to 1.05 euros from 0.38 euro in the prior-year period while comparable EBITDA slipped 0.4% to 543 million euros on revenue of 1.36 billion euros, down 19.7%.

EX-DIVIDEND

Adidas: E3.85, BMW: E2.5, Equinor (EQNR): $0.27, LafargeHolcim: SF2, Partners Group: SF25.5

Yesterday, European stocks were broadly lower, with the Stoxx Europe 600 Index falling 2.2%. Germany's DAX 30 dropped 2.0%, France's CAC 40 declined 1.7% and the U.K.'s FTSE 100 was down 2.8%.

EUROPE ADVANCE/DECLINE

88% of STOXX 600 constituents traded lower or unchanged yesterday.

29% of the shares trade above their 20D MA vs 50% Wednesday (below the 20D moving average).

21% of the shares trade above their 200D MA vs 24% Wednesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 2.9pts to 36.32, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Healthcare

3mths relative low: Insurance

Europe Best 3 sectors

basic resources, telecommunications, banks

Europe worst 3 sectors

retail, food & beverage, industrial goods & services

INTEREST RATE

The 10yr Bund yield fell 3bps to -0.53% (below its 20D MA). The 2yr-10yr yield spread rose 0bp to -20bps (above its 20D MA).

ECONOMIC DATA

GE 07:00: Apr PPI YoY, exp.: -0.8%

GE 07:00: Apr PPI MoM, exp.: -0.8%

FR 07:45: Apr Inflation Rate YoY final, exp.: 0.7%

FR 07:45: Apr Inflation Rate MoM final, exp.: 0.1%

FR 07:45: Apr Harmonised Inflation Rate MoM final, exp.: 0.1%

FR 07:45: Apr Harmonised Inflation Rate YoY final, exp.: 0.8%

GE 09:00: Q1 GDP Growth Rate QoQ Flash, exp.: 0%

GE 09:00: Q1 GDP Growth Rate YoY Flash, exp.: 0.4%

EC 10:00: Q1 GDP Growth Rate YoY 2nd Est, exp.: 1%

EC 10:00: Q1 GDP Growth Rate QoQ 2nd Est, exp.: 0.1%

EC 10:00: Q1 Employment chg QoQ Prel, exp.: 0.3%

EC 10:00: Q1 Employment chg YoY Prel, exp.: 1.1%

EC 10:00: Mar Balance of Trade, exp.: E23B

MORNING TRADING

In Asian trading hours, EUR/USD was flat at 1.0804 while GBP/USD fell to 1.2212. USD/JPY edged up to 107.33. AUD/USD eased to 0.6454. This morning, official data showed that China's industrial production rose 3.9% on year in April (+1.5% expected) while retail sales dropped 7.5% (-6.0% expected).

Spot gold advanced further to $1,733 an ounce.

#UK - IRELAND#

Computacenter, computer services provider, released a trading update for the four months to April 30: "We stated in our trading statement on 23rd April 2020 that current trading was more robust than we had anticipated at the start of the crisis. Since that date business has accelerated further and we have managed to secure some substantial Technology Sourcing contracts due to our ability to scale our operations to meet the demand. These incremental volumes mean that we now believe that the first half of 2020 will be considerably ahead of the same period of last year."

BP, a giant oil producer, was downgraded to "underweight" from "equalweight" at Morgan Stanley.

#GERMANY#

Hapag-Lloyd, a shipping and container transportation company, announced that 1Q net income slumped 74.0% on year to 25 million euros and EBITDA fell 4.1% to 469 billion euros on revenue of 3.34 billion euros, up 9.1%. Regarding full-year outlook, the company said: "Hapag-Lloyd admittedly still continues to expect EBITDA of EUR 1.7 - 2.2 billion and EBIT of EUR 0.5 - 1.0 billion for the current financial year. However, unless there is a recovery in demand for container transport services earlier and stronger than currently expected by the relevant market participants, the upper end of the forecast ranges is barely achievable from today’s perspective."

#FRANCE#

Ubisoft Entertainment, a video game producer, announced full-year adjusted LPS of 0.09 euros from an adjusted EPS of 2.80 in the prior year and adjusted operating income plunged to 34 million euros from 446 million euros last year. Also, revenue was down 13.6% on year to 1.59 billion euros and net bookings dropped 24.4% to 1.53 billion dollars. The company said it now expects 2020 - 2021 net bookings of 2.35 - 2.65 billion euros, compared with 2.60 billion euros previously, and adjusted operating income forecast is lowered to 400 - 600 million euros from 600 million euros.

Source: GAIN Capital, TradingView

#BENELUX#

Aegon's, an insurance company, "A-" credit rating outlook was revised to "Negative" from "Stable" at Fitch. The rating agency said: "The Outlook revision reflects disruption to economic activity and financial markets from the coronavirus pandemic."

#SWITZERLAND#

Richemont, a luxury goods company, announced that full-year net income declined 67% on year to 1.65 billion euros and operating profit dropped 22% to 1.52 billion euros on revenue of 14.24 billion euros, up 2%. The company stated: " The closures of our internal and external points of sales, changing attitudes towards consumption and subdued consumer sentiment will weigh on this year's results, even if, at the time of writing, we are gradually resuming operations as parts of the world emerge from lock-down. It is impossible to make meaningful predictions at this time."

Straumann, a tooth replacement solutions provider, was downgraded to "underweight" from "neutral" at JPMorgan.

#FINLAND#

Fortum, a Finnish energy company, announced that 1Q EPS jumped to 1.05 euros from 0.38 euro in the prior-year period while comparable EBITDA slipped 0.4% to 543 million euros on revenue of 1.36 billion euros, down 19.7%.

EX-DIVIDEND

Adidas: E3.85, BMW: E2.5, Equinor (EQNR): $0.27, LafargeHolcim: SF2, Partners Group: SF25.5

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM