Stock market snapshot as of [18/6/2019 3:19 PM]

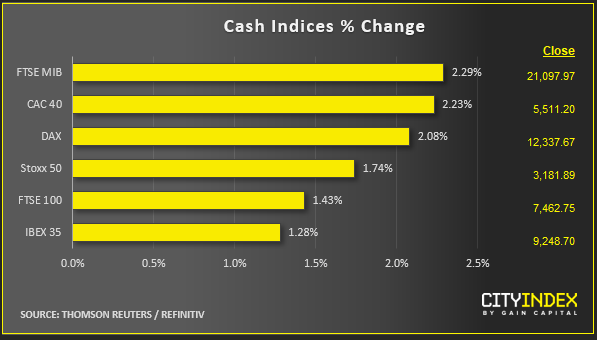

- If European Central Bank president Mario Draghi really is as resigned as he seems, to being remembered just for policy easing, Tuesday’s stock market rally is a fair parting shot

- His comments at the ECB’s Forum on Central Banking in Portugal look responsible for hauling sentiment out of the doldrums and setting major European indices on course for gains this week

- Noting that pressures on growth were “persisting”, Draghi indicated that “additional stimulus may be needed” if the economic outlook doesn’t improve, and that rate cuts remain “part of our tools”

- His words reinvigorated Wall Street futures enabling Dow Jones, S&P, Nasdaq and Russell indices to open firm and reach six-week highs

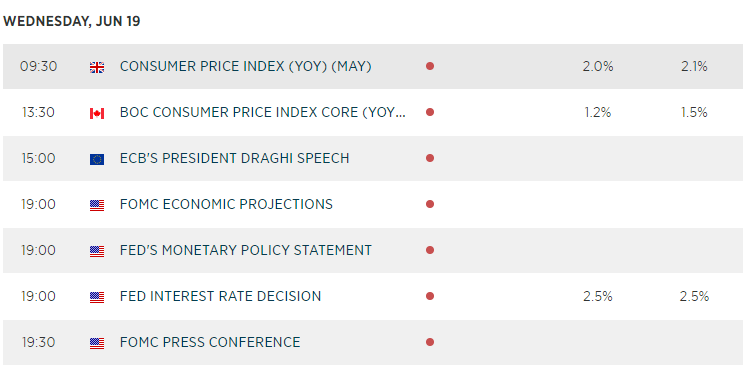

- For now, investors aren’t looking too closely under the hood. Draghi’s scheduled ECB departure, by the end of October, adds policy uncertainty linked to his successor. As well, any easing signalled by the Federal Reserve on Wednesday would weaken possible ECB accommodation, which is pretty accommodative already, to say the least

Corporate News

- All European industrial sectors rally hard, but utilities advance as much as materials, rising over 2%. Such ‘safe-haven’ plays betray that a fair amount of caution accompanies Tuesday’s cheer

- U.S. techs continue a solid advance that began on Monday with the FANG notably buoyed. However, the top technology gainers are tariff-hit chip and hardware shares that could benefit from lower borrowing costs. Broadcom, Nvidia, Texas Instruments and Qualcomm surge 3%-6% higher

Upcoming corporate highlights

BMO: before market open

Upcoming economic highlights

Latest market news

Today 07:55 AM

Today 04:47 AM

Yesterday 11:23 PM

Yesterday 10:19 PM

Yesterday 08:00 PM

Latest Indices articles

Yesterday 08:00 PM

Yesterday 04:54 PM

April 15, 2024 06:08 AM

April 14, 2024 04:00 AM