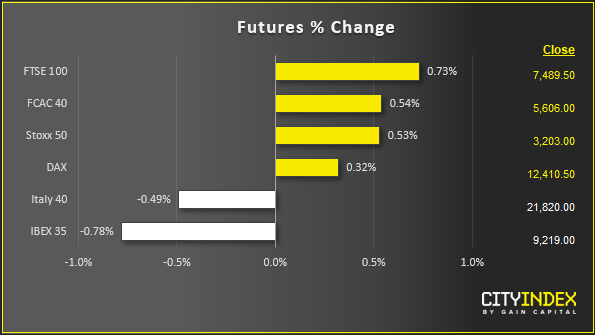

Stock market snapshot as of [26/7/2019 5:51 PM]

- Thursday’s Draghi-triggered heebie-jeebies have passed though markets are still monitoring anything with implications for rates whilst also staying finely tuned to earnings season

- That all adds up to a rebound that looks like it can make it to Wall Street’s close after European cash trading rounded-off the week on a firm note, albeit fractionally lower than the one before

- Aside from a surprise beat by Alphabet and relatively solid Twitter earnings (offsetting Amazon’s miss) upside influences included a continuing strain of resilience amid overall mixed company results, and a better-than-expected early assessment of second quarter U.S. GDP

- A low-momentum day in Treasury yields – with an eye to next week’s Fed meeting – may have played a part, as it kept a rein on the dollar bid. The greenback was also buffed by White House Economic Advisor Larry Kudlow ruling out retaliatory currency intervention; at least for the minority of speculators suspecting it. Still, with key economic readings tracking above forecast, it may only be a matter of time before rates anxiety returns, regardless of the Fed’s almost-certain 0.25% cut next week

- Kudlow did have encouraging words on trade talks for markets. He noted further tariffs would remain on hold, if discussions next week go well, a counterpoint to President Donald Trump’s latest threat. Kudlow cautioned there’s no deal yet

- In contrast to Europe, Wall Street is set to close the week definitively firmer, with the S&P 500 up about 1% on last Friday’s close

Corporate News

- One thing Friday trading has in common on both sides of the Atlantic is that cheer has been led by a relatively small set of companies, a small worry regarding market breadth

- Alphabet’s 10.8% rise a while ago constituted about 60% of the S&P 500’s gain in points. That ebullience is on the back of sharply better than expected earnings, revenue and key metrics than the market was expecting

- Amazon fared far worse as its star-unit, AWS, produced lower than expected growth for the first time in dozens of quarters, albeit growth was still at a high-double digit percentage rate. Profit—and profit guidance—also missed as one-day shipping costs are set to be higher than initially thought. The stock dipped 2.5% at Friday’s worst. Solid Twitter earnings and user growth helped reassure tech sector investors though. The group’s story of underlying improvement, including 7-straight profitable quarters, looks more and more credible. The stock was last up 9.5%

- In Europe, Vodafone, Nestle and Vivendi, helped carry the upside, whilst Gucci-owner Kering and Anglo were notable losers. The UK-based mobile giant launched a surprise pivot away from cell infrastructure ownership that could raise tens of billions of euros. Its stock surged almost 11%. Nestle gained 1.7% to a record high as the STOXX heavyweight’s deal with Starbucks gave profits a bigger than expected boost. Vivendi’s first-half adjusted net income also beat. Kering offset some of the gains with an 8% slump as Gucci sales disappointed. Miner Anglo American reported inconvenient news ahead of earnings next week. Its biggest shareholder will sell his stake. The stock fell 4%

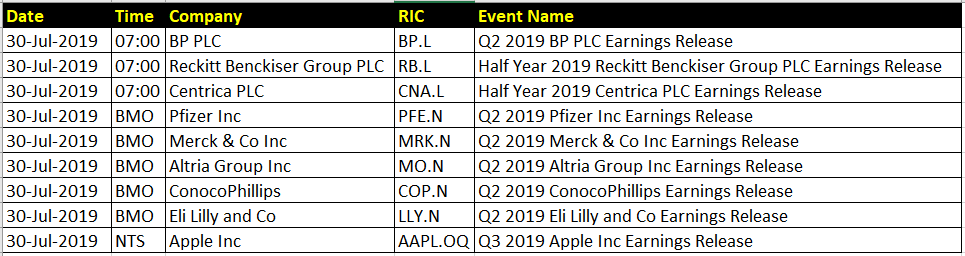

Upcoming corporate highlights

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Abe articles

October 24, 2023 09:00 AM

October 19, 2023 01:42 PM

October 11, 2023 02:28 PM

April 25, 2023 02:36 PM