Stock market snapshot as of [25/07/2019 0527 GMT]

- Ahead of the European opening session, most Asian stock markets are showing positive performances triggered by the stellar gains seen in key U.S. semiconductors stocks that have helped to lead the S&P 500 and Nasdaq 100 to another record fresh all-time highs.

- The key catalyst came from Texas Instruments, a major U.S. chipmaker that soared by 7.4% on better than expected earnings results that offset the headwinds from U.S./China trade tensions and fallout from China’s Huawei Technologies where it has contributed to 3% to 4% of Texas Instruments’ global revenue.

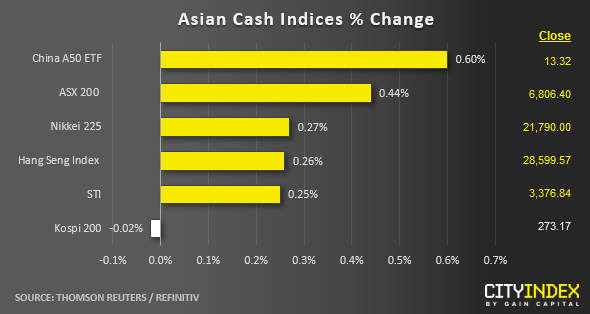

- The Australia’s ASX 200 is now just 0.5% away from its all-time high level of 6851 printed in Oct 2007 on the backdrop of an easing liquidity condition. RBA governor Lowe has commented in a public speech today that low interest rates are here to stay and can go lower if economic activities fail to take off.

- The underperformer as at today’s Asian mid-session is Korea’s Kospi 200; almost unchanged due to rising regional geopolitical risk where North Korea has launched two projectiles from the eastern part of the Korean Peninsula.

- After the S&P 500 closed at a new record all-time high of 3019, the S&P E-min futures has remained firm in today’s Asian session as it has inched higher by 0.22% to print a current intraday high of 3024.

- European stock indices CFD futures are recording modest gains at this juncture where the FTSE 100 is up by 0.30% after its underperformance seen in yesterday, 24 Jul where it declined by -0.73% due to Brexit uncertainties. The German DAX CFD futures has rallied by 0.54% after a bullish break and a daily close above the 12500 key medium-term resistance.

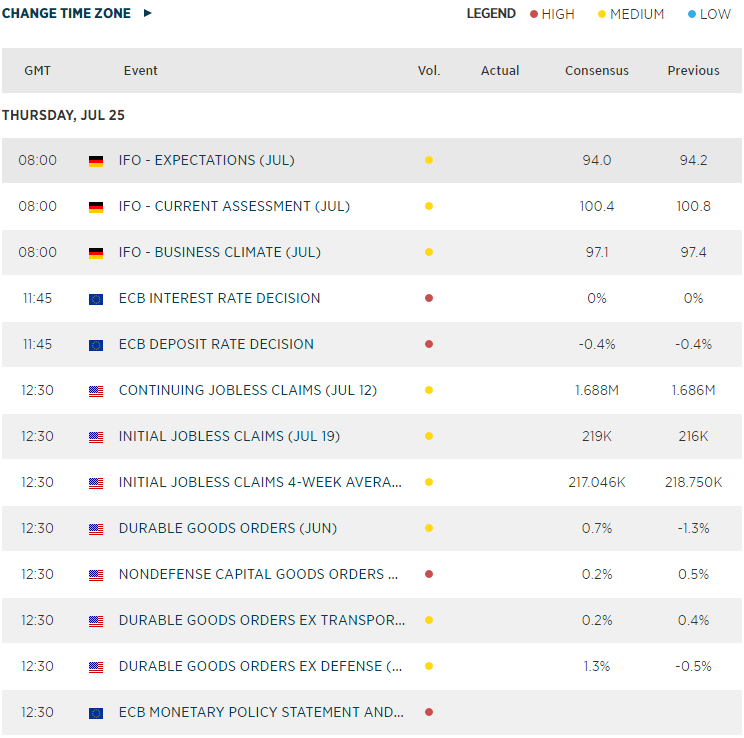

- ECB monetary policy decision at 1145 GMT follow by its press conference at 1230 GMT. The consensus is set for no interest rate cut on its key deposit rate now at -0.4%. A dovish statement from ECB out-going governor Draghi can firm up the forward guidance for a cut in the Sep meeting follow by a restart of the QE programme that may see European stocks extending their gains.

- U.S. bellwether tech and FAANG stock, Amazon will report its Q2 earnings after the close of U.S. session today. Consensus for its EPS is set at $5.29 where a beat is likely to see a retest on its current all-time high of 2050.50 printed on 04 Sep 2018; it closed at 2000.81 yesterday, 24 Jul. Further gains in Amazon can drive up the S&P 500 and Nasdaq 100 where it has a significant market capitalised weightage in these indices (3rd largest in the S&P 500 & the 2nd largest in the Nasdaq 100).

Macroeconomic Calendar

*Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Indices articles

April 18, 2024 04:46 PM

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM