Stock market snapshot as of [25/7/2019 4:07 PM]

- European stock markets fleetingly experienced the best of days, before sliding back to experience the day’s worst levels as initial euphoria over the prospect of a new round of European Central Bank easing rapidly faded due to a lack of policy detail

- Rates would "remain at their present OR LOWER levels (emphasis mine) at least through the first half of 2020" according to the ECB’s statement

- Bank stocks initially led the sharp relief rally. Ironically, this looked partly based on the fact that rates had been kept rates on hold. The ECB also mentioned “tiered” rates though, referring to a system which could exempt some lenders from full exposure to the central bank’s deepened negative deposit rate. That currently stands at minus 0.4% and is forecast to fall to -0.5%, perhaps as early as September

- As such, market sentiment, including on banks, was afforded much of the benefits from easier policy, whilst spared the numerous downsides, though the mood later reversed

- The central bank’s president, Mario Draghi was keen to reiterate the Governing Council’s displeasure with weak inflation and the economic conditions, which he suggested were “getting worse and worse”, especially in manufacturing

- Yet he was coyer on policy detail, suggesting more would come at the bank’s next meeting in September. This leaves the overall policy outlook rather vague, especially on a possible resumption of QE

- European stock markets have fallen back into that temporary policy vacuum. In the end, Draghi/ECB coyness plus their negative assessment of the outlook cut short the cheer from news of pending rate cuts. This left Europe’s broadest equity gauge, the STOXX, down 0.9% a short while ago, after it initially surged higher by the same amount

- Perhaps unsurprisingly, ECB news has not been Armageddon for the euro. It did plunge to a new two-month low of $1.11015, but subsequently bounced and was last holding higher on the day around $1.116 levels

- Turkey’s lira proved similarly resilient despite the CBRT’s much deeper than forecast 425 basis point cut to 19.75%. It just goes to show that in a world where G10 market and base rates are tumbling, the search for yield trumps all

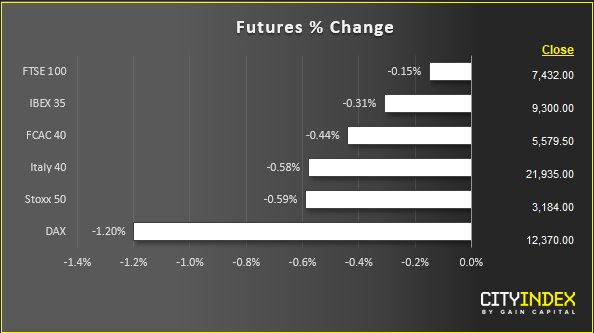

- Elsewhere, neither Britain’s FTSE 100, nor the pound seemed much better or worse off, for now, amid the latest UK political drama. The new Prime Minister Boris Johnson has administered a wholesale cull of the cabinet, installing allies instead, in what appears to be preparations for a possible general election, according to some commentators

- ECB disappointment remains the main focus outside of Europe though. The Dow and S&P 500 are bedding down in negative territory. The Nasdaq fares worse given the latest regulatory broadsides against giant U.S. web firms, plus another set of disappointing earnings from Tesla

Corporate News

- Only the defensive European healthcare sector was left standing in the green late in the session, led by an 8% jump by AstraZeneca. Its second quarter revenues neatly beat analyst expectations on the back of improving sales, though net income was a tad light

- STOXX’s Banks sub-index ground 1% lower, whilst less than a handful of the 11 EURO STOXX 50 companies that reported earnings on Thursday traded higher. Lacklustre results was one of their issues

- Nokia was also amongst Europe’s top gainers with a rise of 8% after beating quarterly expectations and claiming a lead in the forthcoming 5G explosion. AB InBev rallied for an eighth session, continuing to shrug off a canned Asia IPO as it burnished successful deleveraging despite reporting so-so earnings

- PayPal added weight to Wall Street’s technology sector slump, falling 5% after missing sales forecasts. Facebook also slipped, losing 1.5%, despite topping revenue, profit and some user expectations overnight. The stock rose somewhat in after-hours trading on Wednesday, but the surprise announcement of a new investigation by the Federal Trade Commission has proved to be a fly in the ointment. Amazon and Alphabet also retreat ahead of their own earnings releases this evening on the latest indication that the regulatory environment for dominant techs is becoming less accommodating. Tesla is among the deepest large-cap fallers though, tanking 13% at last check. Despite promising news on its automobile margin and a maintained delivery target of 360,000-400,000 cars in 2019, the group reported a deeper loss per share than even the worst estimate of a consensus compiled by Bloomberg.

Upcoming corporate highlights

AMC: after market close NTS: no time specified

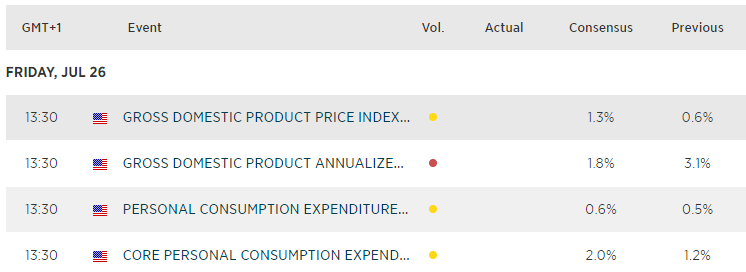

Upcoming economic highlights

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest EUR articles

April 13, 2024 08:00 PM

March 25, 2024 02:55 AM

January 22, 2024 04:19 AM

January 18, 2024 04:46 AM