Stock market snapshot as of [19/7/2019 2:47 PM]

- It’s a lacklustre tug of war between index bulls and bears and Friday, as the main gauges dither a few tenths of a percentage point over the flat line. They last stood a little higher

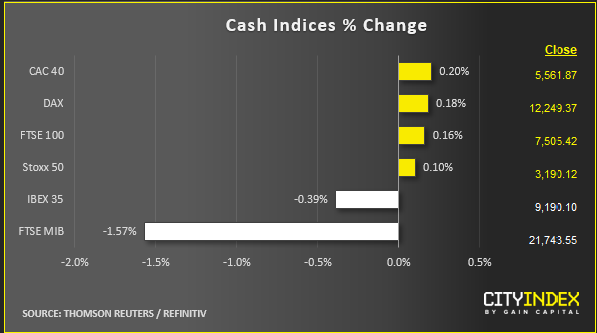

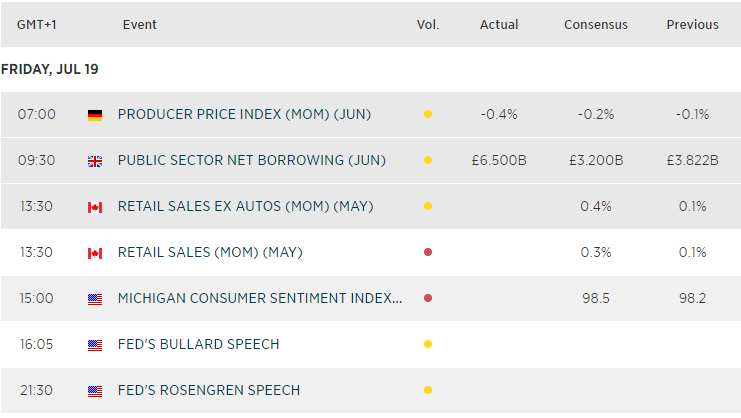

- Familiar frets strum out a familiar tune as Europe’s all-country STOXX 600 remains hamstrung by everything from resistance last tested in April, frequent data undershoots (on Friday it was Germany’s PPI) and earnings that do little to contradict pessimistic estimates

- At least anxieties over whether the pressure is coming off the Fed and the ECB to move quickly and aggressively with rate cuts, is fading. Even then, doubts remain. Two Fed officials have essentially contradicted each other in the space of a few minutes, albeit ultra-dovish comments by New York Fed President John Williams have mostly prevailed on Friday. This has contained the dollar and buffed interest in silver and gold

- ECB prospects also look less equivocal as economists assess the downward spiral of Eurozone readings in light of comments by the central bank’s president Mario Draghi. He said in last month that he’s ready to add stimulus if the economic outlook doesn’t improve. Consensus forecasts now point to a 10-basis point deposit rate cut to a record-low minus 0.5%, though not at next week’s ECB policy meeting. Strong hints will be the likely outcome instead

- Wall Street indices open a tad higher than the Continent’s, rising 0.3% to 0.5% so far

Corporate News

- Non-earnings-related corporate news is another positive distraction on the northern side of the Atlantic. Swedish/Swiss ABB’s China unit plans to sell stakes in two JVs. ABB grinds higher in Zurich, taking machinery peers with it

- Anglo/German tourism firm TUI also stands out, with a 6.4% gain offering much-needed relief to the travel & leisure sector. The €4.7bn group is seen as a beneficiary of Boeing 737 Max compensation. Travel-industry data showing improving demand in the UK and Germany also helps

- JC Penney, BlackRock and Microsoft are in focus among U.S. heavyweights. Retailer JCP is reportedly corralling investments banks as it readies a large-scale debt restructuring. The stock tanks 10%. Asset manager BlackRock missed estimates though its shares rose 1% on promising active management and software licensing fees

- Boeing bounces back by 2% from a slide on Thursday that followed its pre-announcement of a $5bn hit related to its 737 Max

Upcoming corporate highlights

BMO: before market open

Upcoming economic highlights

Latest market news

Today 05:00 PM

Today 07:55 AM

Today 04:47 AM

Latest Indices articles

Yesterday 08:00 PM

Yesterday 04:54 PM

April 15, 2024 06:08 AM