Stock market snapshot as of [22/07/2019 0510 GMT]

- Ahead of the European opening session, most Asian stock markets have started a new week on a cautious stance due to rising geopolitical tensions in the Persian Gulf where Iran’s armed forces seized a British oil tanker last Fri, 19 Jul.

- Secondly, market participants had started to scale back on the expectations of a 50 bps Fed rate cut on 31 Jul after a Wall Street Journal report that stated that the Fed was likely to cut rates by 25 bps and may make further cuts in the future due to trade uncertainties. The CME FedWatch Tool is now pricing in a 22.5% probability of a 50 bps cut after the 31 Jul FOMC meeting, down from a high of 46.2% seen last week, after the dovish remarks made by New York Fed official Williams.

- The worst performer is the Hong Kong’s Hang Seng Index which has declined by -0.77% as at today’s Asian mid-session led by the consumer cyclicals and telecommunications sectors; down by -0.98% and -1.50% respectively.

- A sell-off was seen in the S&P 500 E-mini futures on last Fri, 19 Jul U.S. session that broke last Thurs, 18 Jul low of 2974 (last Fri, it closed at 2971 at the end of the U.S. session). In today’s Asian session, the S&P 500 E-mini futures has managed to inch up by 0.32% to print a current intraday high of 2980. Overall, a potential medium-top is in place for the S&P 500 where further down move can trigger a negative feedback loop into the Asian stock markets coupled with the U.S. earnings season still in play. Click here to read our latest weekly technical outlook.

- European stock indices CFD futures are not showing any significant movement at this junction where both the FTSE 100 and German DAX are almost unchanged. From a technical analysis perspective, the DAX is still not showing any clear signs of a recovery, watch the 12200 near-term support next.

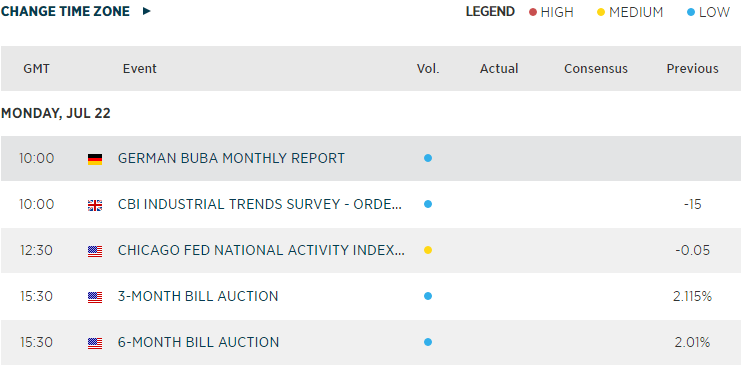

Macroeconomic Calendar

*Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Indices articles

Yesterday 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM