Stock market snapshot as of [02/08/2019 0540 GMT]

- Ahead of the European opening session, Asian stocks have continued to stage three days of consecutive decline reinforced by U.S. President Trump’s sudden fresh tariff of 10% on US$ 300 billion of Chinese imports to take effect from 01 Sep despite U.S. and China trade officials have scheduled the next trade negotiation talks to take place in early Sep in Washington.

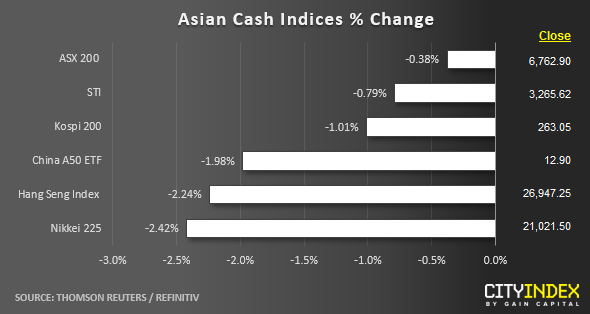

- As at today’s Asian mid-session, the worst performers are China related plays, together with Japan’s Nikkei 225 that has declined by -2.42% triggered by a stronger JPY and an escalating trade dispute between Japan and South Korea over curbs on Japanese exports of three high-tech materials needed to make memory chips and display panels by South Korean chip-makers. Japan has removed South Korea’s fast-track export status with effect on 28 Aug due to national security reasons as per cited by Japanese government official.

- So far, there is no official response from the Chinese government on Trump’s latest tariff hike other than China Foreign Minister Wang Yi told reports on the sidelines of an Association of Southeast Nations event in Thailand that the additional tariffs were “not a correct way” to deal with bilateral dispute”.

- From an intermarket perspective, a break above the key psychological 7.00 level on the USD/CNH (offshore yuan) does not bode well for Asian ex Japan and emerging markets equities in the coming week (click here for more details on our report).

- The S&P 500 E-mini futures has continued to inch lower in today’s Asia session to print a current intraday low of 2938. European stock indices CFD futures are now playing negative catch-up where both the FTSE 100 and German DAX are down significantly by -1.74% and -1.09% respectively.

Up Next

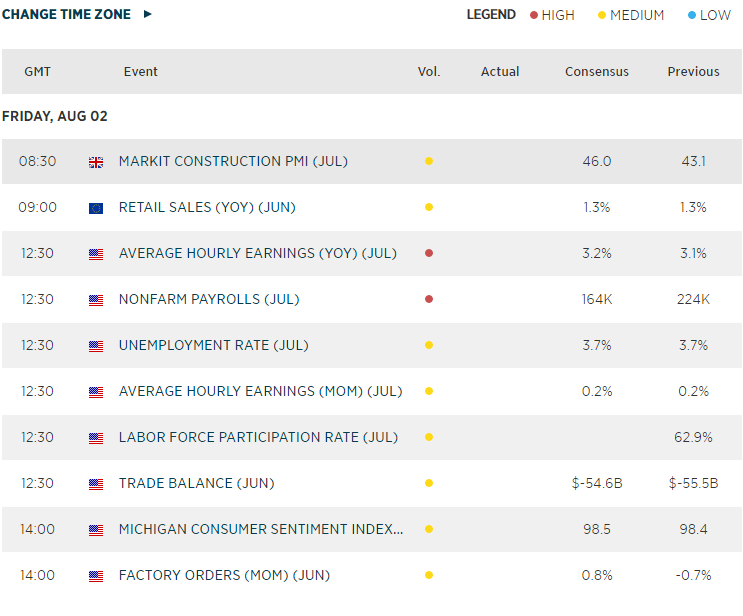

- Eurozone Retail Sales for Jun at 0900 GMT where consensus is set at 1.3%

- U.S. non-farm payrolls for Jul at 1230 GMT where consensus is set at +164K and unemployment rate is expected to remain unchanged at 3.7%.

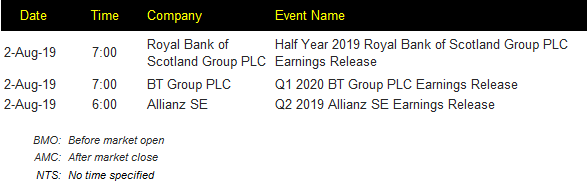

Corporate Highlights

Macroeconomic Calendar

*Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Indices articles

Yesterday 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM