Stock market snapshot as of [17/07/2019 0500 GMT]

- Ahead of the European opening session, most Asian stock markets are trading in red after market participants digested U.S. President Trump’s remarks made in yesterday, 16 Jul U.S. session on the possibility of imposing additional tariffs on Chinese imports, citing displeasure over China’s failure to kickstart the purchase of U.S agriculture products.

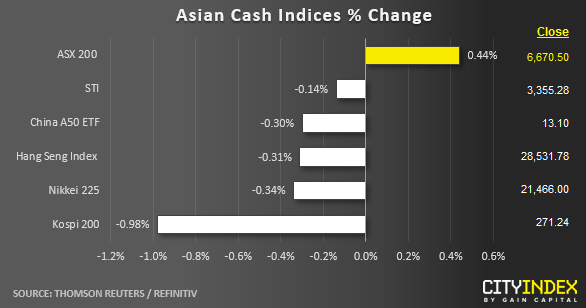

- The Australia’s ASX 200 is the outlier and as at today’s Asian mid-session, it has staged a rally of 0.44% after 3-day of consecutive losses led by the telecommunications services and consumer non-cyclicals sectors that have gained by around 0.80%.

- Singapore exports have continued to decline as it posted a 4th consecutive month of double-digit loss with -17.3% y/y plunge seen in Jun. Modest loss of -0.14% seen in the Singapore’s STI so far with key short-term support holding at 3320.

- Despite yesterday’s weakness seen in the U.S. stock markets where key indices have declined by -0.34% to -0.50%, the key benchmark S&P 500 is still holding above its significant short-term support at 3005/3000. In today’s Asian session, the S&P 500 E-mini futures is trading near the top of a flat range above yesterday’s U.S. session low of 3004 with a high/low range of 3009 to 3003.

- European stock indices CFD futures are trading in the red as well with the FTSE 100 down by -0.26% and the German DAX slide by -0.16%.

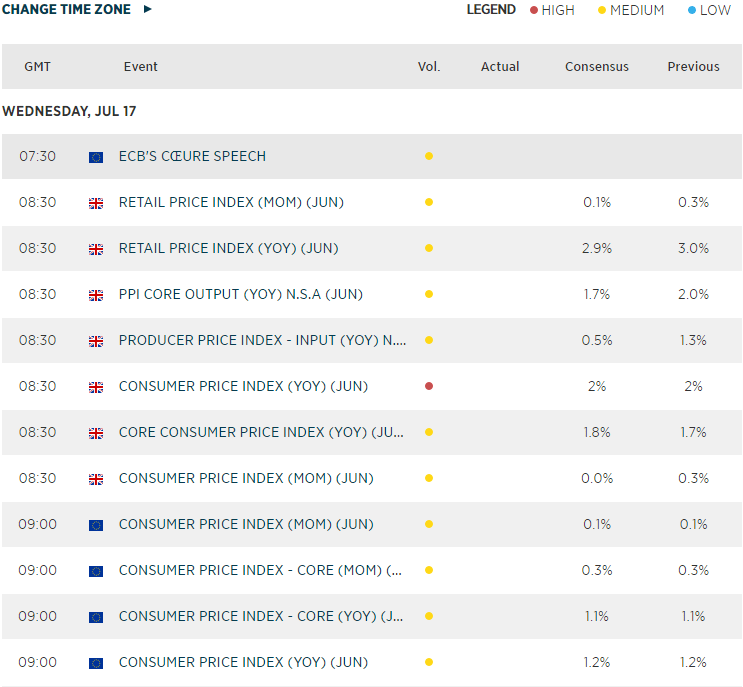

- Key economic data release to watch later will be U.K retail sales and inflation data for Jun out at 0830 GMT.

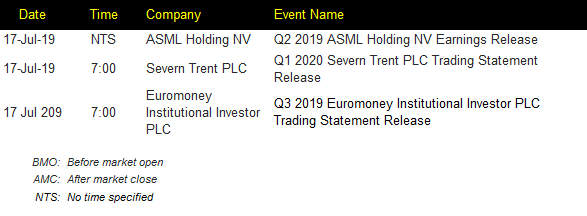

Corporate Highlights

Macroeconomic Calendar

*Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Indices articles

Yesterday 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM