Stock market snapshot as of [09/07/2019 0430 GMT]

- Ahead of the European opening session, Asian stock markets have continued to see profit taking activities for the 2nd consecutive day ahead of Fed Chair Powell’s testimony to Congress on monetary policy and the state of the U.S. economy this coming Wed and Thurs.

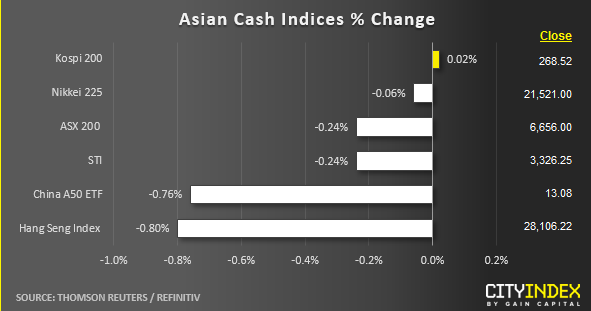

- The magnitude of decline seen in the key Asian benchmark stock indices as at today’s Asian mid-session is lesser versus yesterday’s decline that came in between a range of -1.00% to -2.00%. Interestingly, the previous worse performer, the Kospi 200 has started to stabilize where losses seen so far in the past three days have been attributed to the on-going trade spate over Japan’s exports curbs towards South Korean’s key semiconductor industry.

- From a technical analysis perspective, the recent decline of Kospi 200 from its 01 Jul high of 279.68 has almost met the 61.8% Fibonacci retracement of the previous entire up move from 29 May low to 01 Jul at 267.62. If the Kospi 200 can managed to stage a rebound above 267.62, a potential recovery can materialise.

- Latest news flow has indicated that the Japanese government is opened to talks with South Korea over the export curbs but Japan Trade Minister Seko has reiterated that it has no intention of withdrawing the measures put in place last week on the three specialist materials exports.

- The S&P 500 E-mini futures has continued to decline by -0.47% from yesterday, 08 Jul U.S. session close to print a current Asian session intraday low of 2965 which also confluences closely with a Fibonacci cluster support at 2960.

- European stock indices CFD futures are in the red as well where the FTSE 100 has dropped modestly by -0.17% and a more pronounced decline of -0.54% is seen in the German DAX.

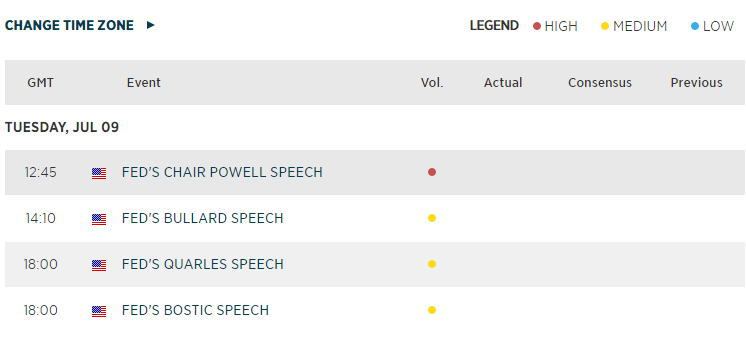

- No key European and U.K economic data releases for today. The main focus will be on Fed Chair Powell’s speech at the Boston Fed conference later at 1245 GMT. It is possible that he could drop a hit on Fed’s current monetary policy stance in the upcoming FOMC’s decision on 31 Jul.

Macroeconomic Calendar

*Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.

Latest market news

Today 10:37 AM

Today 08:25 AM

Yesterday 10:36 PM

Yesterday 05:36 PM

Latest Indices articles

Yesterday 10:36 PM

May 2, 2024 04:00 PM

May 2, 2024 04:23 AM

April 30, 2024 04:04 AM