October 12, 2021 4:42 AM

Reinforced as crude oil closed above $80 overnight for the first time since 2014 and China’s most traded thermal coal futures contract jumped by the daily limit of 8% yesterday as floods forced the closure of 60 coal mines in China.

The driver of the energy crunch an interplay of the following:

- Green energy policies and a rush to hit energy control targets

- Surging power demand in the wake of COVID restrictions easing.

- Power-generation shortfalls on coal shortages and unstable renewable supply.

- Geopolitical developments including OPEC+, Russia, and Iran.

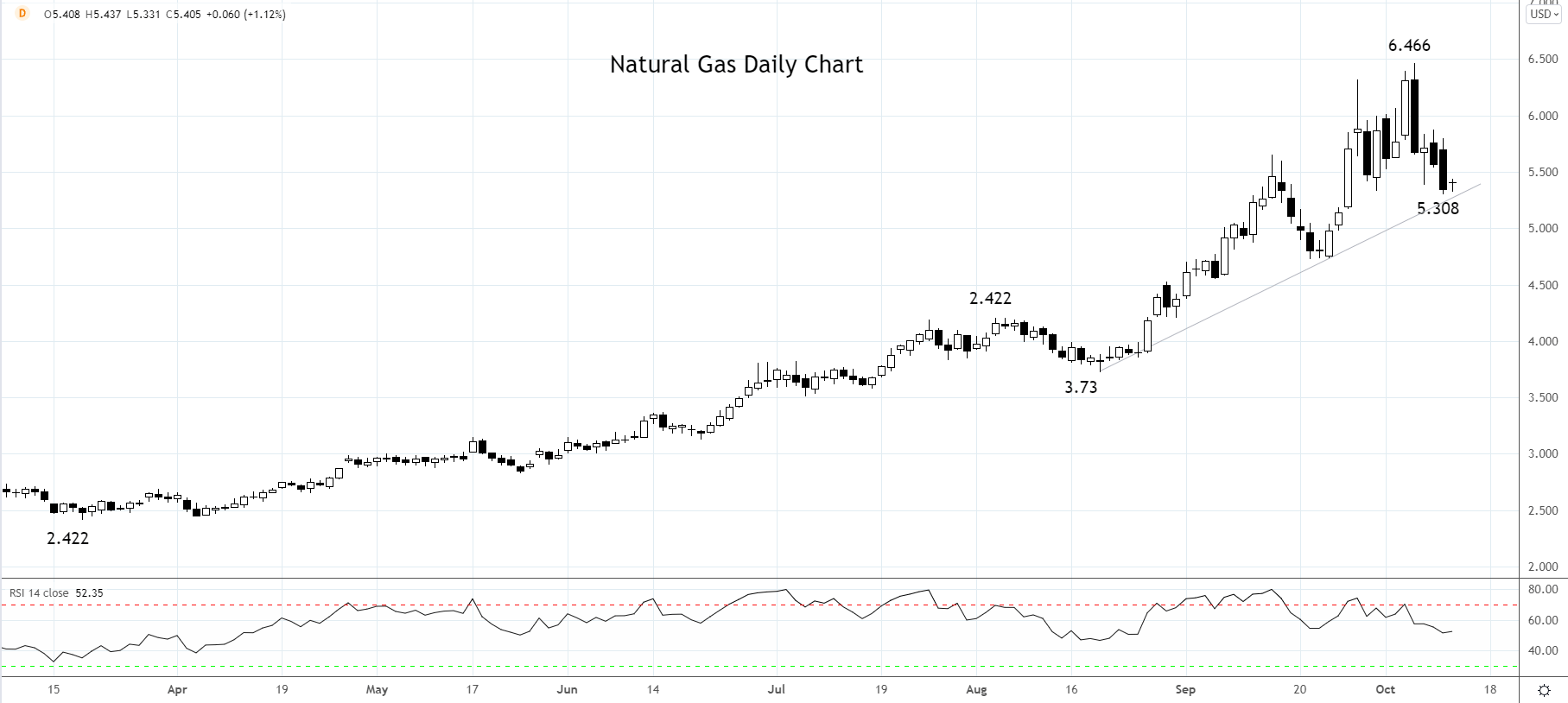

Specifically for natural gas, the driver of its 120% rally since the start of April, a supply shortage on falling domestic output, lower LNG imports, and limited pipeline imports owing to maintenance and a tight gas market in Russia. Playing out against the backdrop of strong demand following a cold winter and spring.

A pledge last week by Russia to increase natural gas supply to the continent, as noted by my colleague Matt Weller has taken the sting out of the market in recent days, and prices have since dropped 15% from a high near $6.50/MMBtu to below $5.50/MMBtu.

Apart from the obvious inflationary implications of higher energy prices, high natural gas prices negatively affect food production. Natural gas is used to produce ammonia and energy from fossil fuels to mine for phosphate. Ammonia and phosphate is a significant component of commercial fertilizer needed to grow food in bulk.

The fertilizer price, already high following the rally in the natural gas price, pushed higher earlier this month, following an announcement that China would halt all phosphate exports.

The recent pullback in natural gas has worked off overbought readings, to be holding above uptrend support $5.30 area.

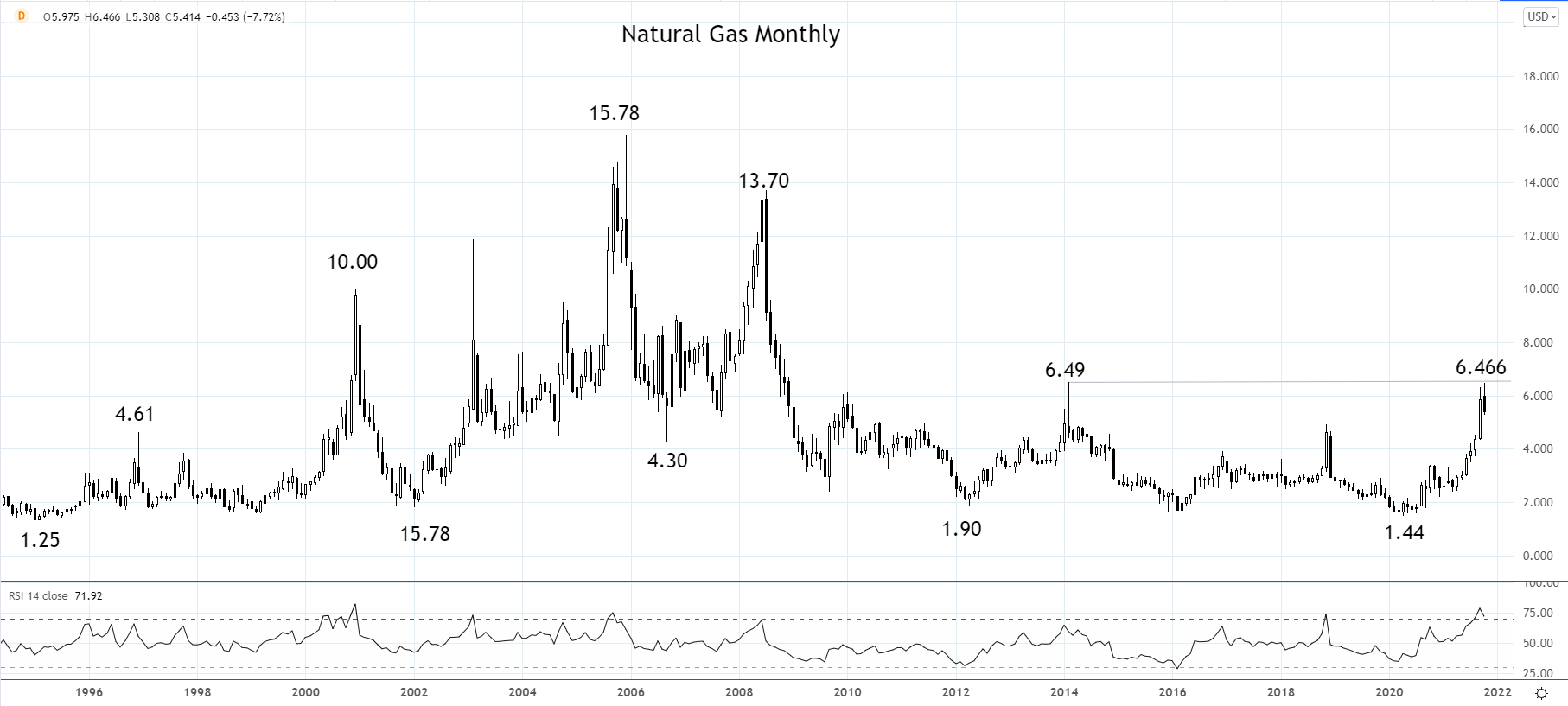

Should this support hold and natural gas see a sustained break above the recent $6.466 high and the 2014 $6.49 high, it could lead to a very messy move towards $10.00 coming from the high of December 2000 viewed on the monthly chart below.

Source Tradingview. The figures stated areas of October 12th, 2021. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Latest market news

Today 07:55 AM

Today 04:47 AM

Yesterday 11:23 PM

Yesterday 10:19 PM

Latest Energy articles

March 27, 2024 12:30 PM

March 18, 2024 04:00 PM

March 14, 2024 11:25 AM

March 6, 2024 05:00 PM