EM Rundown This week s EM central bank bonanza

After last week’s Federal Reserve excitement, traders would probably be happy for a reprieve from the constant “will-they-or-won’t-they” strategizing that inevitably takes place around major […]

After last week’s Federal Reserve excitement, traders would probably be happy for a reprieve from the constant “will-they-or-won’t-they” strategizing that inevitably takes place around major […]

After last week’s Federal Reserve excitement, traders would probably be happy for a reprieve from the constant “will-they-or-won’t-they” strategizing that inevitably takes place around major central bank meetings. Unfortunately (or fortunately, depending on your perspective), this week’s emerging market economic calendar is chock-full of key central bank meetings.

USD/MXN: Banxico still on hold

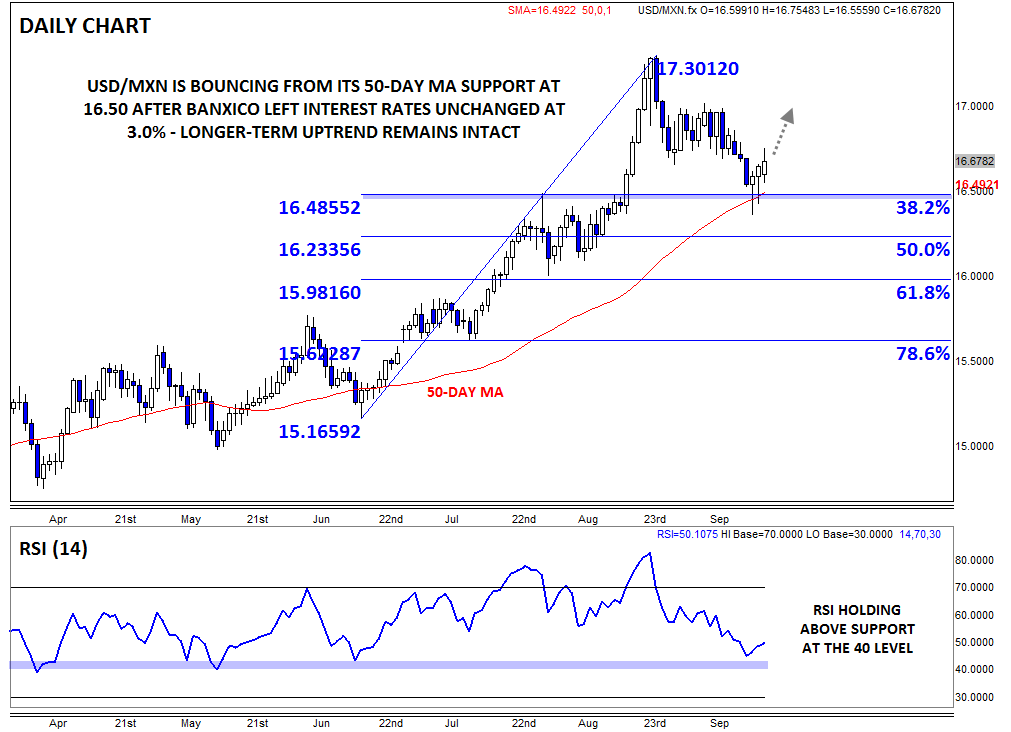

It’s rare for us to have the opportunity to cover a central bank decision “live” in this weekly report, but Mexico’s central bank offered up just that opportunity today. In its regular monetary policy meeting, Banxico left Mexico’s benchmark interest rate (“tasa de fondeo bancario”) unchanged. This decision was widely expected, especially after the US Federal Reserve refrained from raising rates last week. Though inflation remains tame in Mexico, there is pressure for Banxico to match interest rate changes with its much larger neighbor to the North, lest diverging monetary policies cause disruption.

USD/MXN was fairly nonplussed by the decision, generally holding steady around the 16.70 level. From a longer-term perspective, USD/MXN remains within an established uptrend, so traders may continue to favor buying dips toward the 16.00s like we saw last week.

Source: City Index

Source: City Index

European and Middle Eastern Central Banks: No fireworks expected

Looking beyond the North American continent, there are a series of important central bank decisions throughout Europe and the Middle East, though traders don’t expect any tectonic-level shifts in monetary policy.

Tomorrow, the Hungarian National Bank (HNB) is expected to leave interest rates unchanged at 1.35% after recently announcing the end of its current easing cycle. That said, weak GDP growth and low inflation (stemming primarily from falling oil prices) suggest that the bank may take a dovish view in its accompanying statement and press conference. From a trading perspective, EUR/HUF is testing support at its 200-day MA near 309, so a bounce is definitely in play this week.

Also tomorrow, Turkey’s monetary policy committee is widely expected to leave all of its major interest rates unchanged. The central bank is still trying (no pun intended) to normalize monetary policy after the unprecedented currency market volatility earlier this year, but with USD/TRY holding above the 3.00 level, any interest rate cuts would only exacerbate the politically-driven currency weakness. Turkey desperately needs a stable government, but with elections not scheduled until November 1st, the lira will struggle to rally in the coming weeks.

Then, the South African Reserve Bank (SARB) will announce its interest rate decision on Wednesday. The central bank will likely leave interest rates unchanged at 6.00%, but concerns about slowing growth in China and falling commodity prices could lead to a surprise cut. While USD/ZAR has pulled back slightly over the last few weeks, the longer-term uptrend will remain healthy as long as rates hold above the 13.00 level.

Thursday brings two EM central bank decisions. In the Czech Republic, the Czech National Bank (CNB) is anticipated to leave both interest rates and its exchange rate cap against the euro unchanged at 0.05% and EUR/CZK 27.00, respectively.

In Israel, traders are split on whether the central bank will cut interest rates to 0.00% or just leave them unchanged at 0.10%. Frankly, a 10bps shift in interest rates will not have any appreciable impact on the Israeli economy, so the central bank’s accompanying forecasts for inflation and GDP may be more impactful than the headline decision, as they could provide more color for monetary policy in the country moving forward.