EM Rundown Policymakers set the tone in China Turkey Russia and Poland

As readers of our week ahead report know, it will be a very busy week for monetary policymakers in the developed markets, with potentially high-impact […]

As readers of our week ahead report know, it will be a very busy week for monetary policymakers in the developed markets, with potentially high-impact […]

As readers of our week ahead report know, it will be a very busy week for monetary policymakers in the developed markets, with potentially high-impact central bank decisions in the US, Japan, New Zealand, and Sweden. However, many traders may not be aware that emerging market policymakers will be just as active over the next few days. Below, we highlight several of the most important events for EM FX traders to watch:

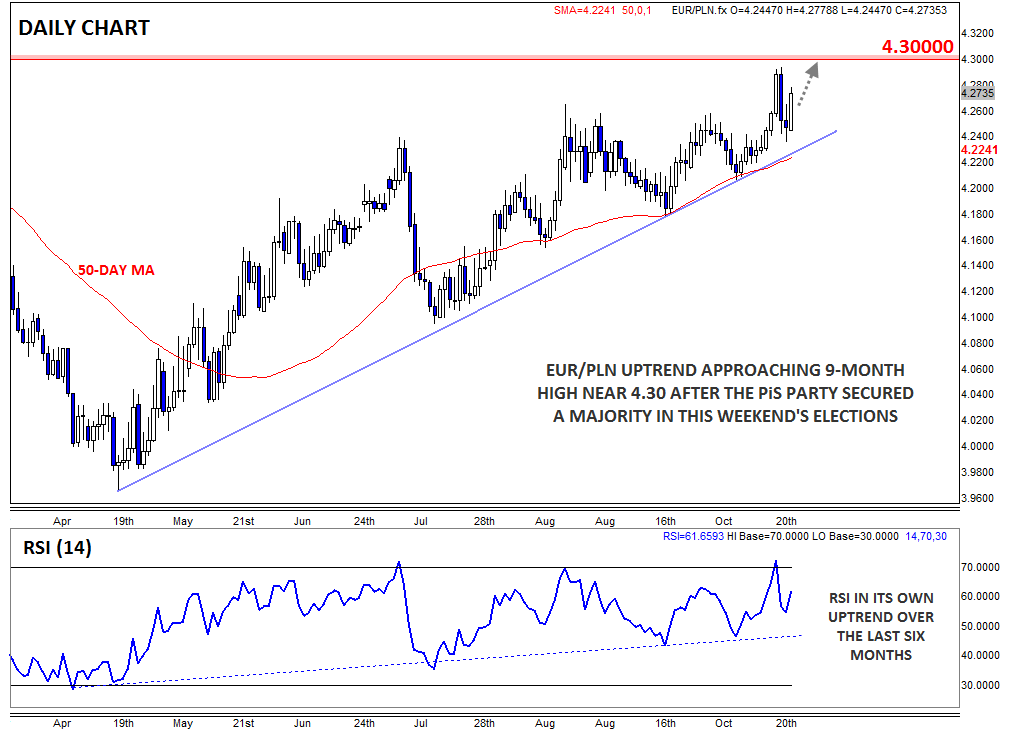

Poland: Election results could keep EUR/PLN trending higher

Over the weekend, Polish citizens went to the polls to elect the conservative Law and Justice party (PiS) into power in the first outright majority in Poland in 26 years. The party ran on a platform of equalizing the country’s recent economic gains, including higher child care benefits and tax breaks for the poor, which has some traders worrying about the government deficit ballooning. On that note, EUR/PLN is rallying back above 4.27 as of writing, and bulls could look to target the pair’s 9-month high up near 4.30 next.

Russia: Central bank faces a tough decision, ruble will be key

The Central Bank of Russia (CBR) will convene on Friday to decide whether to change interest rates from the current 11.00% level. While most analysts do not anticipate a change, some believe that the CBR may cut rates to 10.50% given the subdued consumer demand and recent stability in the ruble. At the end of the day, the central bank needs to see the ruble hold steady or strengthen before feeling comfortable cutting interest rates in order to avoid the risk of another currency collapse back toward the 70.00 level

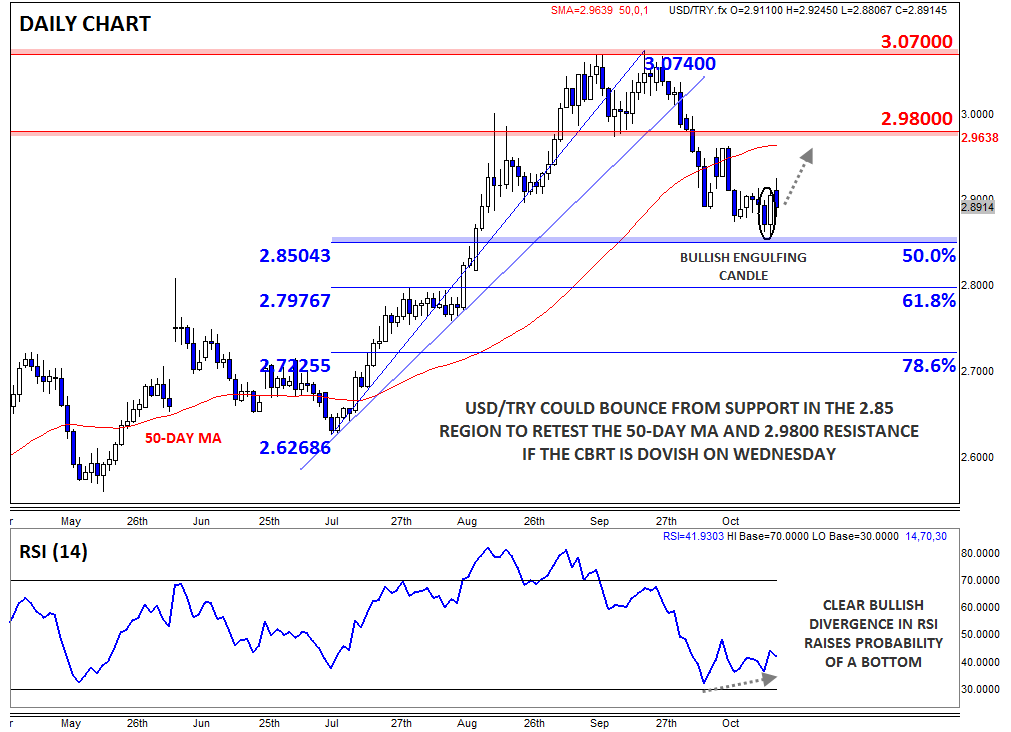

Turkey: Wednesday’s Quarterly Inflation Report will set the tone

Across the Black Sea, the Governor of the Central Bank of the Republic of Turkey (CBRT) will release the bank’s updated Quarterly Inflation Report (QIR). Much like in the UK, this report serves to relay the central bank’s long-term outlook for inflation, growth, and interest rates, and therefore tends to be a very impactful report for traders. It’s also worth noting that Wednesday afternoon and Thursday are public holidays in Turkey, so the thin market conditions could exacerbate the volatility in the pair as we move into midweek.

Looking at the chart, USD/TRY may have put in a near-term bottom on Friday, when rates carved out a clear Bullish Engulfing Candle* .This candlestick pattern shows a shift from selling to buying pressure and often marks a low in the market. Combined with the bullish divergence in the RSI indicator, a dovish economic outlook from the CBRT could take USD/TRY back toward its 50-day MA and previous-support-turned-resistance around 2.98.

*A Bullish Engulfing candle is formed when the candle breaks below the low of the previous time period before buyers step in and push rates up to close above the high of the previous time period. It indicates that the buyers have wrested control of the market from the sellers.