EM Rundown Fed rate hike fears drive USD ZAR to an all time high

With the market-implied odds of a Federal Reserve rate hike in December skyrocketing from around 30% a few weeks ago up to 68% as of […]

With the market-implied odds of a Federal Reserve rate hike in December skyrocketing from around 30% a few weeks ago up to 68% as of […]

With the market-implied odds of a Federal Reserve rate hike in December skyrocketing from around 30% a few weeks ago up to 68% as of writing, it’s not surprising that the US dollar has been strengthening across the board. EM FX traders will remember during past scares of Federal Reserve tightening (notably the “Taper Tantrum” in 2013 and the “Rate Hike Hissy Fit” – my term that never caught on – in March of this year), emerging market currencies were hit especially hard, but this time around the selling pressure has been less consistent.

Certain EM currencies, including the Singapore dollar, South African rand, and Turkish lira (despite the seemingly lira-positive results from Turkey’s recent election) have been hit relatively hard over the last week. On the other hand, currencies like the Mexican peso and Russian ruble have been holding relatively steady despite the market’s evolving Fed expectations.

The accepted “wisdom” is that a tightening cycle by the Federal Reserve inevitably leads to outflows from emerging markets, hurting their currencies and markets, and certainly throughout the ‘80s and ‘90s, this adage held true. However, during the two most recent examples of Fed rate hike cycles (beginning in 1999 and 2004), emerging market currencies held up relatively well until global equity markets collapsed. This shift is primarily due to more floating exchange rates in the emerging world and (if you can believe) generally lower levels of aggregate debt relative to GDP.

Therefore, bears may want to key in on currencies with fixed exchange rates (especially in the Middle East, given the sustained weakness in oil prices) and the currencies of economies with large current account deficits as the most vulnerable to a potential Fed rate hike. Not surprisingly, currencies in this category include the aforementioned Turkish lira and the South African rand.

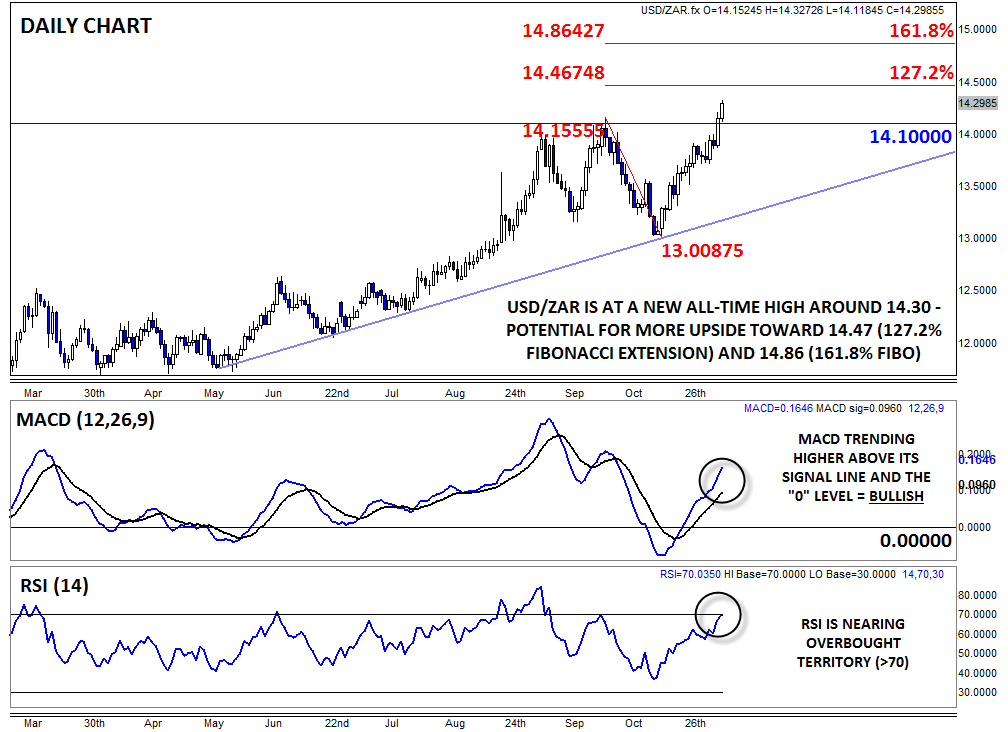

Technical view: USD/ZAR

Speaking of the rand, USD.ZAR has rallied to a new all-time high near 14.30 as of writing. In addition to fears about the Federal Reserve raising rates, South Africa’s currency is also suffering as a result of its correlation with gold prices, which have had a rough couple of weeks.

With the exchange rate at an all-time high, there is nothing but blue skies above for USD/ZAR in our view. The only potential resistance levels to watch will be the 127.2% and 161.8% Fibonacci retracements at 14.47 and 14.86, respectively. Meanwhile, the bias will remain definitively higher as long as USD/ZAR holds above previous-resistance-turned-support at 14.15.