ECB Rate Cut Spares Euro Slow amp Painful Descent

Nearly 2 months after the Fed surprised markets by not tapering its purchases, the ECB responds in kind by unexpectedly reducing both its refinancing and […]

Nearly 2 months after the Fed surprised markets by not tapering its purchases, the ECB responds in kind by unexpectedly reducing both its refinancing and […]

Nearly 2 months after the Fed surprised markets by not tapering its purchases, the ECB responds in kind by unexpectedly reducing both its refinancing and marginal lending rates by 25 bps to 0.25% and 0.75% respectively.

The ECB referred to protracted and broad-based period of low inflation as well as volatility in the Eurozone overnight rate (EONIA) resulting from plunging excess liquidity reaching a 2-year low of € 194,000?

Today’s Eurozone dynamics reveal the combination of broad-based improvement in business surveys, falling sovereign bond yields and surging risk of disinflation. The contrast between stable market metrics/recovering macro dynamics and slowing prices is likely to put the onus on the LTRO option, particularly due to falling liquidity.

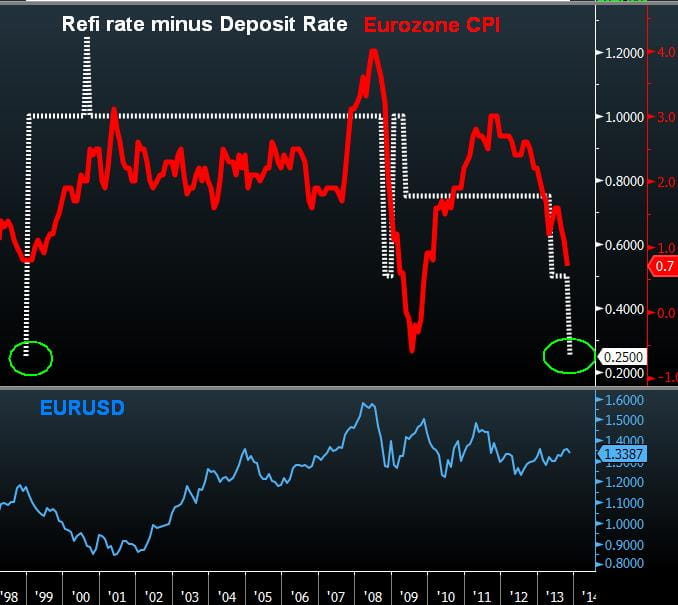

Refi-Deposit Spread at Record Low

The gap between the refinancing rate and the deposit rate has been reduced to 0.25%, the lowest level since the euro began trading in January 1999. Interestingly, the gap is three times as low as in 2009, when inflation was negative during the financial crisis, compared to the current 0.7%.

The above developments are likely to prevent EURUSD from breaking above the $1.37 even if Draghi did not mention euro strength, but it remains premature to expect a euro decline below $1.30 (which coincides with the 100-week moving average) considering the likelihood of downward GDP revisions in the US and prolonged asset purchases from the Fed.

Look Beyond US Q3 GDP

Following the 1st wave of selling from the ECB rate cut, the euro sustained a 2nd wave of selling after the unexpectedly strong release of advanced US Q3 GDP at 2.8% vs expectations of 2.0% and previous 2.5%. The figure was propped by the 0.8% positive impact from business inventories, without which, would have shown final sales at 2.1% due to lower lift from consumers.

As the partial govt shutdown is seen dragging Q4 GDP by 0.5%-0.6%, consumers will have to deliver more than their declining contribution of 1.5% to GDP for growth to present a meaningful differential over overseas rates.