ECB Rate Cut is Beyond Last Resort

Markets not reacting to what the ECB said, but instead to what it did not say Euro is pushed across the board as ECB’s Draghi […]

Markets not reacting to what the ECB said, but instead to what it did not say Euro is pushed across the board as ECB’s Draghi […]

Markets not reacting to what the ECB said, but instead to what it did not say

Euro is pushed across the board as ECB’s Draghi said there was no discussion about negative deposit rates or a reduction in the refinancing rate, and gave no hints on the euro being too high as was the case in February. Not even the ECB forecast for a 0.4% contraction in 2013 GDP managed to weigh on the euro.

LTRO is Last Resort, then Comes … ECB Rate cut

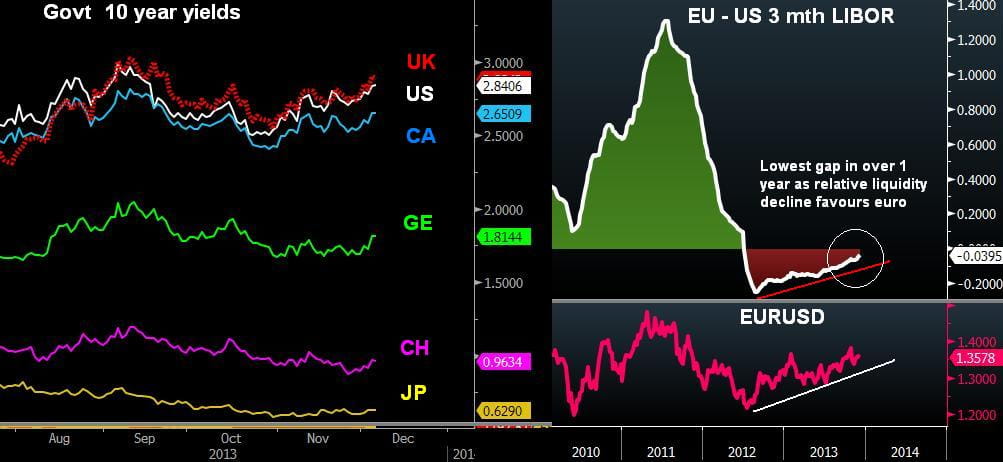

Eurozone dynamics continue to reveal the rare combination of broad-based improvement in business surveys, falling sovereign bond yields and lingering risk of disinflation. And so the contrast between stable market metrics/recovering macro dynamics and slowing prices is likely to eventually put the onus on the LTRO option with a twist (requiring banks to spend proceeds in the economy & not just for buying bonds for carry trade purposes), particularly due to falling liquidity at the ECB. But note that as long as markets are not undergoing the tightness of summer 2012, then an LTRO announcement would be EUR- positive – as was seen after the announcement of late 2012.

Unlike interest rate cuts, which have a floor, there is no ceiling/limit on LTROs. The advantage of LTRO over rate cuts is that they are relatively more efficient in times of disinflationary risks as well as in spiking bond yields as far regenerating capital into capital markets as opposed to triggering a liquidity trap under negative rates. Only when German inflation threatens a decline below 1.0% y/y (currently at 1.3%y/y) and Eurozone CPI slips back towards 0.5% y/y (currently at 0.9% y/y), will the ECB consider implementing the LTRO and verbally threatening a rate cut.

UK Treasury Statement Shrugged, but wait for BoE Minutes

The UK Treasury upgraded its revisions to GDP growth and reduced its view on unemployment (playing catch-up with BoE forecasts), while the Office for Budget Responsibility sees a budget surplus in 2018/19, a year earlier than anticipated and borrowing to be £9bn less than projected in March. Gilt yields (charts below) remain at the top of the G7. Sterling may extend its decline towards $1.6250s ahead of any data surprise from Friday’s NFP, but a rebound is well anticipated back to the $1.65 territory upon release of the BoE minutes later this month.

US GDP Revised Higher, then came the Shutdown

The sharp upward revision in US Q3 GDP to 3.6% from 2.8% remains a manifestation of rising inventories, especially personal consumption was reduced to 1.4% from 1.5%. Given Q3 GDP occurred prior to the government shutdown (estimated to have reduced at least 0.5% from Q4 GDP growth), its relevance in predicting a Fed tapering is shadowed by the time lag taken to fully reinstate furloughed government workers and the possibility of another budget and debt ceiling showdown as early as mid-January—both of which would keep any tapering off the table before Q1.The impact of the shutdown should also be considered into tomorrow’s jobs report. The impact of the government shutdown will continue to distort much of the economic data.