The EUR/USD outlook is clearly going to change this week with both the Fed and ECB rate decisions to come ahead of US non-farm payrolls report on Friday. The stickiness of Eurozone inflation means there is a greater risk for a hawkish surprise, potentially leading to a bullish breakout above the 1.10 handle on the EUR/USD. At the time of writing though, the EUR/USD bears were exerting some pressure.

Eurozone inflation rises to 7%

For now, the battle around 1.10 continues on the EUR/USD, with rates falling below this handle at the start of this week on the back of a stronger IMP PMI report and a surprise 2.4% drop in German retail sales. However, Eurozone CPI inflation edged up to 7.0% in April from 6.9% previously, while core CPI edged down a tad to 5.6% from the record 5.7% the month before. Both measures were bang in line with the estimates, though.

With key risk events ahead of us, speculators appear unwilling to commit in either direction as there remains some uncertainty in terms how much tightening we will get from the two central banks. Clearly, both the bulls and the bears will want to hear it straight from the horses’ mouths before committing on the long or short side.

What is the ECB expected to do?

The ECB’s benchmark interest rate is at its highest level since 2008, at 3.5%. ECB members have continued to make hawkish noises ahead of the May policy meeting, although the lack of forward guidance in March means it remains uncertain how much tightening we will get this time. After two consecutive 75bp hikes, the ECB dropped to 50bp over the past three meetings and it’s possible we could see them drop to 25bp this time. The market is pricing in around two more rate hikes from the ECB in this cycle.

But it appears as though there’s only been limited impact from the banking turmoil, while the Eurozone economy has avoided a severe recession. Given that inflation remains sticky and well above target, this raises the possibility we will get a hawkish surprise from the ECB on Thursday, especially if the Fed meeting the day before is not too dovish. This could either be in the form of a 50-bps hike or a 25-bps hike plus some hawkish commentary around it – for example, hints of several further rate increases.

Any hawkish surprise could boost the EUR/USD outlook, while a dovish surprise could see it trend lower for a few days at least.

EUR/USD outlook: How will ECB rate decision impact exchange rate?

Assuming that the Fed does not deliver any major surprises on Wednesday, the EUR/USD could go well north of 1.10 in the event of a hawkish surprise from the ECB on Thursday, either in the form of a 50-bps hike or a hawkish forward guidance accompanying a 25-bps hike.

However, a dovish rate hike could see the EUR/USD drop to 1.0800. For example, the ECB could highlight the risk of a sharper or longer-lasting economic slowdown, one that puts any further rate increases in doubt or at best “data-dependent.”

Our EUR/USD outlook remains bullish heading into these ECB rate decision.

Fed decision could have even bigger impact on EUR/USD outlook

The other side of the equation of course is the US dollar, which will come under the spotlight on Wednesday with the Fed’s rate decision and again on Friday with the release of US nonfarm payrolls report. Whilst concerns over weaker US data and mid-tier banks is bubbling away in the background, the odds continue to favour another 25bp Fed hike to 5.25%, which the market pricing implies will be the terminal rate. Yet, comments from Fed official remained hawkish into the blackout period. So, look for clues to decipher whether it is a hawkish hike (+25bp with more to follow), or a dovish one. If it is the latter, then any dovish surprises from the ECB will have less of a negative impact on the EUR/USD than would have otherwise been the case.

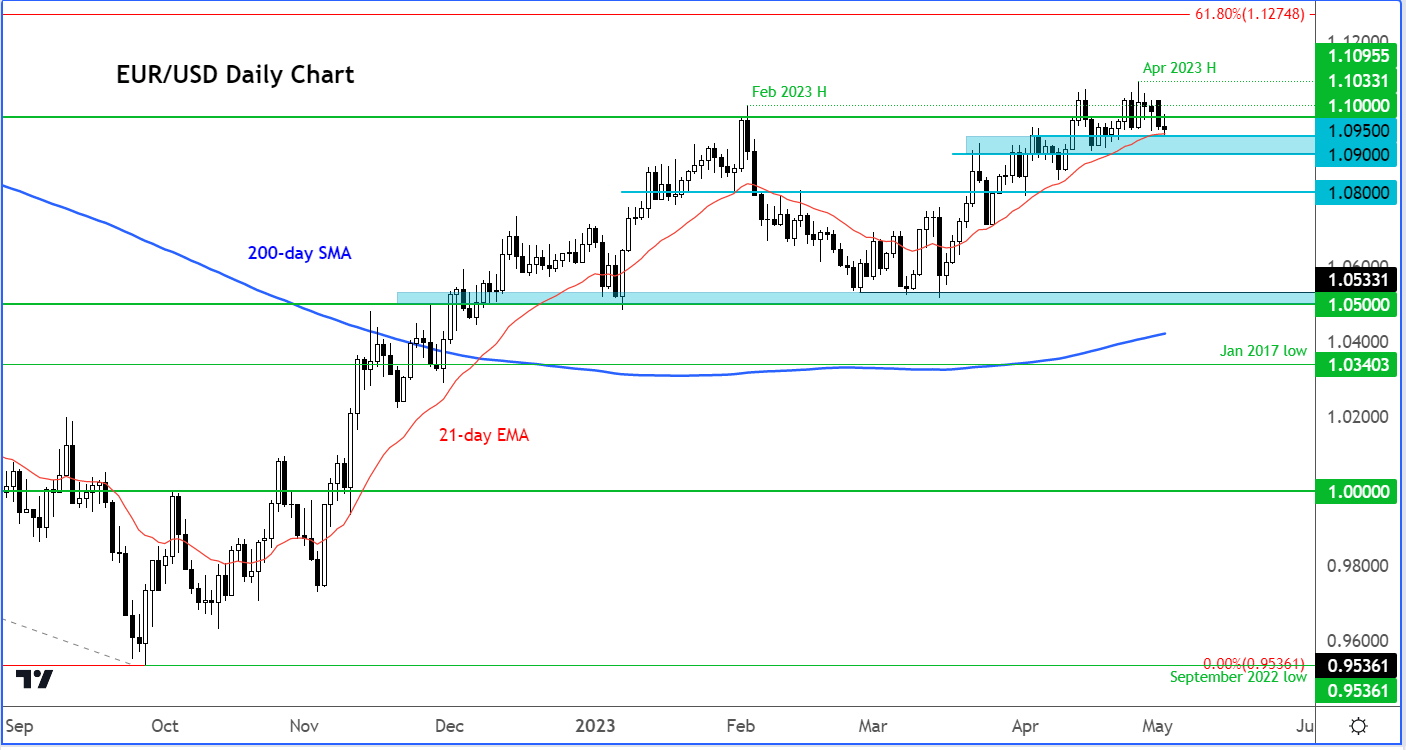

EUR/USD outlook: Technical analysis

Ahead of the ECB and Fed rate decisions, the EUR/USD continues to coil inside a tight range, around 1.1000. For now, the bullish trend is kept alive, although momentum is not there. Still, support is being provided in the dips. So far, the region between 1.0900 to 1.0950 has firm on several occasions. This is also where the 21-day exponential moving average comes into play. For as long as rates hold above this area, the bulls will be happy. Otherwise, the bullish momentum will fade further, discouraging the bulls to stick around.

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

European Central Bank FAQs

What is the ECB rate?

The ECB rate, also known as the key interest rate, determines the conditions for commercial banks borrowing capital from the European Central Bank. There are three rates within the eurozone:

- The main refinancing rate – the rate for commercial banks borrowing from the ECB in the medium term

- The marginal lending rate - the rate for commercial banks borrowing from the ECB in the short term

- The deposit interest rate – the interest earned on capital stored by commercial banks with the ECB overnight

What time is the ECB rate decision?

The ECB rate decisions get announced through a press release at 1.45 pm CET on the day of the meeting, an ECB press conference then follows at 2.30 pm CET.

See our full economic calendarWho is Christine Lagarde?

Christine Lagarde is a French politician and lawyer who has been the President of the European Central Bank (ECB) since 2019. She was the first woman to serve as France’s finance minister and has also served as managing director of the International Monetary Fund (IMF)

See the latest ECB news